Banks, along with mining and energy, are my favorite sectors. They are part of the old economy, which the majority loves to hate.

The mining industry is a favorite sparring partner of ecologists, whose Tesla is powered by a battery containing cobalt from the Congo—denial and hypocrisy in one. People who do not understand banks' importance to society are grumbling against them. These same individuals often use banks for one thing—loans to buy stuff they can not afford. Ultimately, it is the bank's fault that they cannot manage their finances. At least, those people think so.

The development of banking and the extraction of raw materials are the foundations of modern civilization. Raw materials are the inputs of every endeavor. Capital must flow; to grow, it must move. Banks are the superconductor through which it flows.

Today, it’s time to examine the banking industry from an investors' perspective. In this article, I argue why banks are attractive investments, explain how to value banking stocks and estimate banks’ solvency and liquidity.

Banks - unexpected opportunities in unexpected places

Without banking, the economy will grind to a halt. Limited movement of capital, goods, and services means stagnation on local and regional levels. Banks' crucial role makes them an attractive investment and a necessary part of the economy.

The banking sector is highly diverse - from traditional commercial banks to boutique wealth and asset management banks to global systematically important banks (GSIBs). I believe that some of these groups will be the big winners from the market paradigm shift and the growing entropy in the world.

Since the beginning of this decade, we have entered a new secular inflationary cycle. The banking system will be one of the agents of this change and one of its primary beneficiaries.

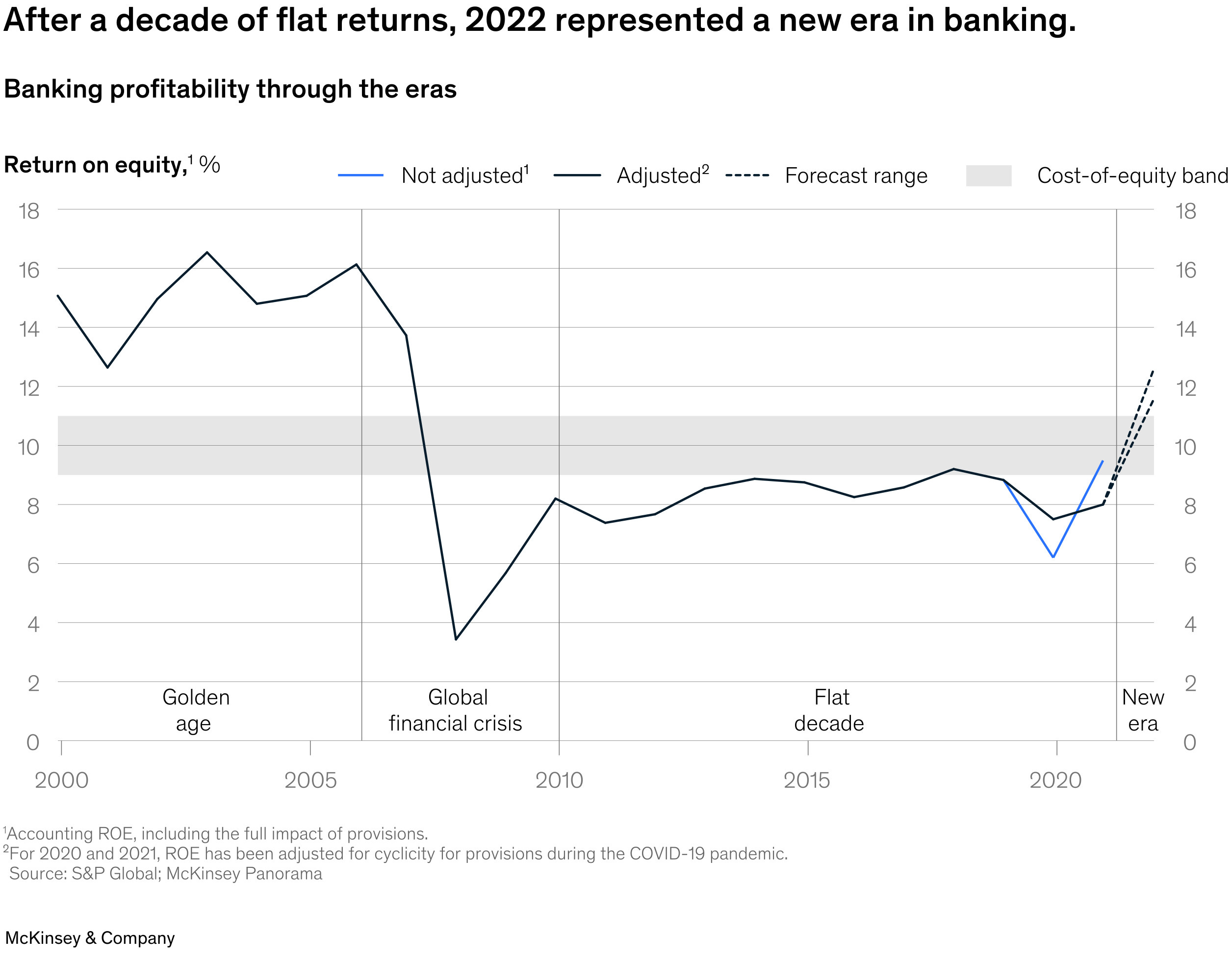

Banks in the previous deflationary regime went through a Lost Decade. After the 2008 crisis, the entire industry stagnated. The chart below shows that ROE merely exceeds the cost of equity.

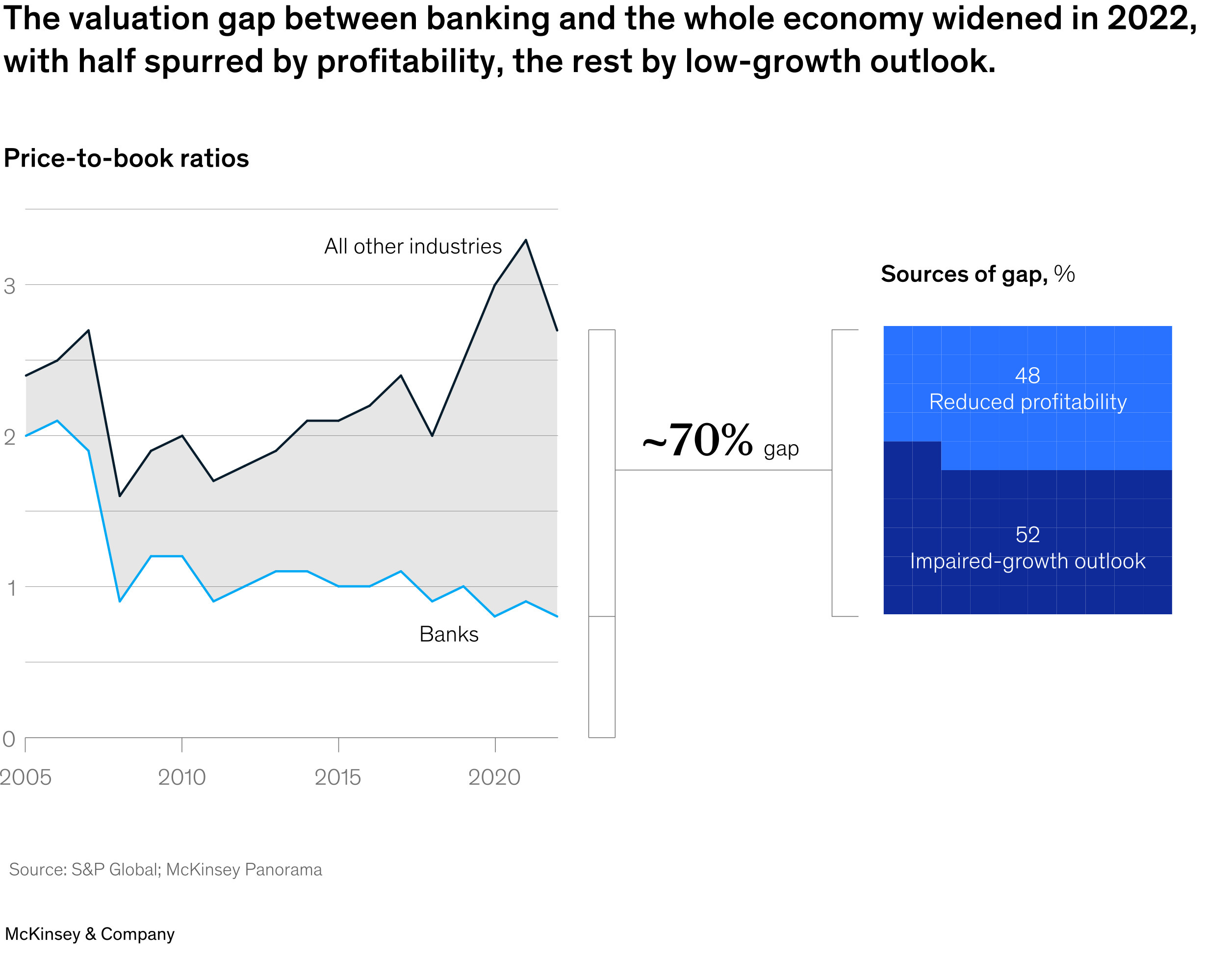

Banking, compared to other sectors of the economy, lags. The Price to Book ratio is not perfect, but it illustrates well enough the gap between banks and the economy over the last 15 years:

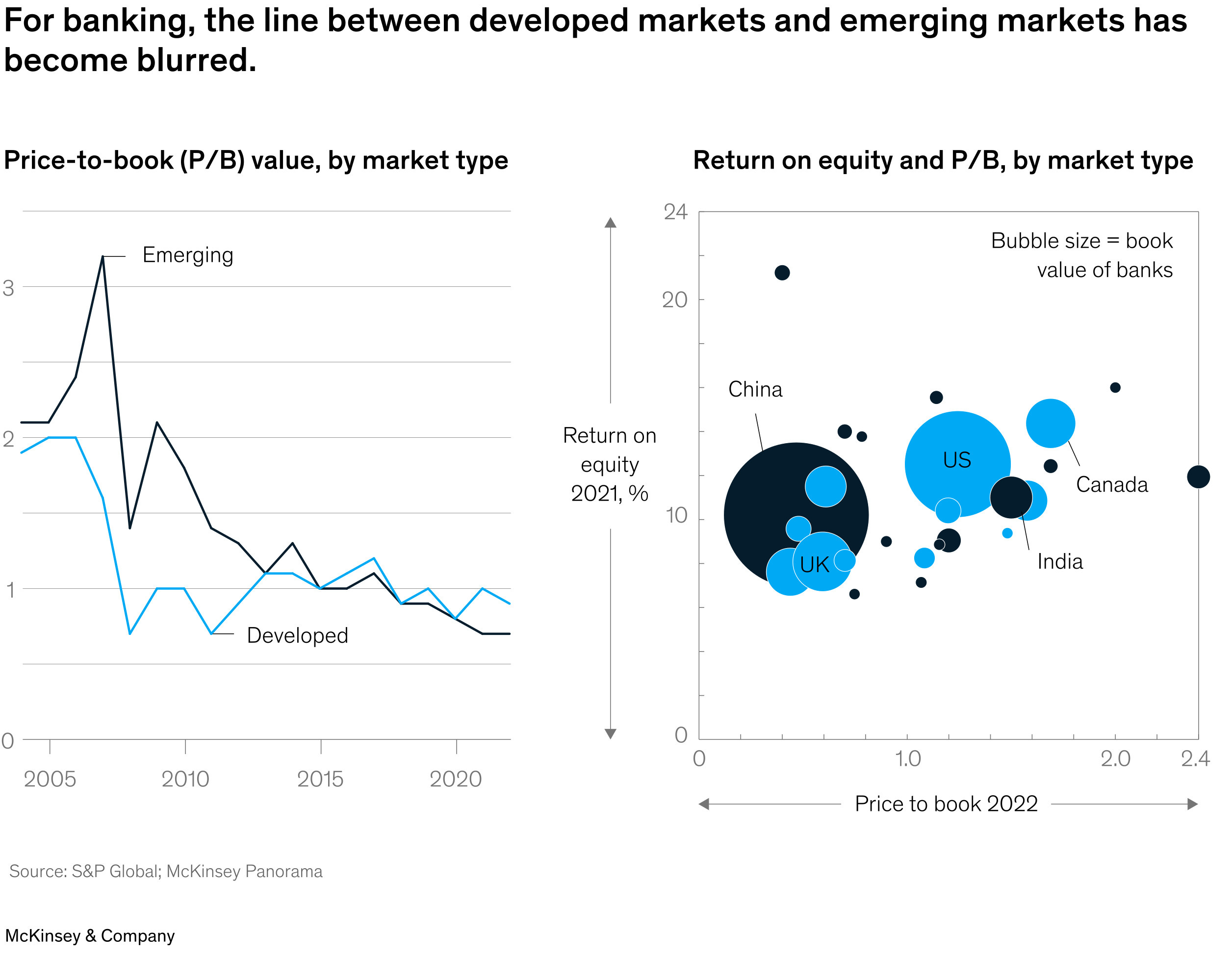

The comparison between the banking sectors of developed and emerging markets is also revealing. Usually, the latter has a higher P/B ratio than the former, but now it is the other way around.

In the present decade, we are moving from a deflationary to an inflationary paradigm. This paradigm shift means that new industries and regions will rise while others will decline. Moreover, the way we play the market will transform once again.

In a deflationary regime, the big winners are the core (the US as the present global hegemon), bonds, technology stocks (Schumpeter creative destruction), and financial assets. In an inflationary regime, the periphery (emerging markets), commodities (Malthusian view on all things commodities deficit), banking stocks, and tangible assets dominate.

Large caps rule over small and medium-sized companies during a deflationary regime and vice versa in an inflationary regime. In parallel, passive investing (Beta) will give way to active investing (Alpha).

The transition from a deflationary to an inflationary paradigm significantly affects the banking system. Those changes create new opportunities for investment in the banking sector.

In the new regime, the banking industry will undergo another transformation:

Growing protectionism: demand for safe capital locations will grow. This will make banks operating in jurisdictions like the Channel Islands, Malta, Switzerland, and other neutral destinations increasingly profitable.

Growing protectionism 2: large economies, still categorized as developing, will seek increasing political and economic autonomy. Their banking systems are no exception to this process. In countries such as Brazil, Mexico, and India, large local banks will assert themselves as regional leaders at the expense of European and US banks.

Rising interest rates: secular inflation means that ZIRP is a thing of the past. Interest rates will remain higher for an extended period, magnifying banks’ profit margins considerably.

Capital will move from the core to the periphery. Commodity-based economies will attract more investment, and banks in countries like Brazil and Mexico will become increasingly attractive.

Return of tangible assets: banks financing projects related to tangible assets such as infrastructure, freight, mining, and energy will be increasingly profitable.

Revenge of Alpha: The last two decades have been dominated by passive investing and Beta harvesting. However, that approach will not work in the new regime. Markets are becoming harder to predict, and active management will strike back. Wealth and asset management banks will benefit from the return on Alpha investment.

Technological progress is not directly related to the transition from a deflationary to an inflationary regime, but it significantly impacts the banking industry. Digital payments are becoming an increasing part of commercial banks' activities. Particularly in regions lacking banking infrastructure, such as sub-Saharan Africa and parts of Latin America, banks that offer convenient and low-cost online payment are already in high demand.

All changes are guideposts on a map, pointing to where to look for Alpha.

The banks I consider investable must have at least two of the following traits:

Operate in neutral jurisdictions and/or emerging markets.

Invest and finance projects related to tangible assets.

Its core business is wealth and asset management.

Offer digital banking services.

Banks, like any industry, have specific parameters that we need to know. As in mining companies, we look at AISC, LOM, and grade, so we analyze RWA, CTE1, and CAR in banks. In the next section, I discuss how to measure a bank’s capital adequacy and how to value a bank’s business.

Solvency and liquidity

Analyzing any business means analyzing the downside risks. Banks are no exception. Risks specific to all banks can be divided into the following groups:

Credit risk

Liquidity risk

Market risk

Operational risk

The BIS chart shows the weight of each risk. Credit risk has the highest total risk weight.

Credit risk is assessed using methods defined and described in the Basel III Accord. In the following lines, I present some of them:

Regulatory capital (RC): it is the minimum equity capital that each bank must maintain. Its purpose is to absorb losses in the event of a solvency crisis. RC consists of two categories: Tier 1 and Tier 2.

Tier 1 or core capital (T1): represents the bank's core equity. It consists of CET1 and AT1, the capital with the lowest risk and the most readily available when needed. Tier 1 is the most liquid capital, so it is the first line of defense in case of solvency and liquidity issues.

Common equity tier 1 (CET1): the bank's equity consisting of common shares, retained earnings, stock surpluses, and accumulated other comprehensive income.

Additional tier 1 capital (AT1) consists of perpetual bonds, preferred shares, and high-contingency convertible securities.

Tier 2 or supplementary capital: unaudited earnings and reserves, subordinated debt, and hybrid debt instruments. This capital is used when Tier 1 is insufficient to provide liquidity to the bank.

Risk-weighted assets (RWA): RWA are all the bank's assets, calculated according to the risk they carry. Each asset—fixed-income investments, loans according to the collateral available, cash—has a different probability of total loss.

Capital adequacy ratio (CAR) is the ratio of RC to RWA. It shows the bank's equity as a percentage of its risk-weighted assets (RWA). The higher the CAR, the safer the bank. This parameter measures the bank's solvency.

Tier 1 capital ratio—the ratio of Tier 1 to RWA. It shows a bank's Tier 1 capital as a percentage of its risk-weighted assets (RWA). The higher it is, the more stable the bank.

CET1 capital ratio is the ratio of CET1 to RWA. The bank's CET1 capital is a percentage of its risk-weighted assets (RWA). The higher it is, the more stable the bank is.

Liquidity coverage ratio (LCR) is the ratio of the high-quality liquid assets (HQLA) to total net cash outflows for 30 days. The bank must have sufficient liquid assets for 30 days of negative cash flows. This parameter estimates the bank's liquidity.

BIS establishes minimum ratios between types of capital and RWAs. These are intended to measure the bank's stability, expressed in terms of its solvency and liquidity.

Capital adequacy ratio > 8 %

Tier 1 ratio > 6 %

CET1 ratio > 4.5 %

LCR > 100%

The described metrics are tools with high diagnostic value. They simply measure a bank’s ability to survive a crisis. Sooner or later, any business is challenged to weather a storm, and banks are no exception. So, maintaining a solid balance sheet and ample liquidity is a must. CAR, RWA, and LRC are essential, as are LOM, AISC, and grade for the mining industry. Investing without knowing what they are and how to use them is like shooting in the dark.

How to value a bank

Each industry has the most appropriate valuation methodology. The particularities of the business determine the choice of approach. Banking is the only business where money has a dual role—funding capital and raw material. It is the capital to finance the enterprise's activities and the raw materials to produce its services.

The following characteristics of banks make the use of cash flow-based valuations inappropriate:

The difference between liabilities, debts, and reinvestments is blurred.

Regulatory requirements for bank capitalization.

Several methods have been adopted to assess banks. I use the Gordon Growth Model or Excess Return Model. The former uses dividends (D), cost of equity (Re), and annual dividend growth (g). The second uses the return on invested capital (ROE), the cost of equity (Re), and the book value of equity (BV). In most cases, I use the Excess Return Model because it captures the essence of the banking business - the bank borrows capital and then lends it at a higher interest rate for extended periods.

The financial markets discount expectations, not facts. So, fixating on the valuation is a dangerous fallacy. At the end of the day, the market determines the price. Our valuation figures are just guidelines, nothing more.

Business valuation is only one step of the investment process, which consists of three stages: security analysis, business valuation, and risk management. The following bullet points sum up how to value a business. The principles are not limited to banks; they apply to any industry.

The valuation of a company is not a qualitative parameter - it is purely quantitative and indicates how much the business is worth. It does not include several qualitative and quantitative parameters that define a company as a good or bad investment.

Business valuation is an exercise in assumptions—we choose the input parameters into the equation, so there is a high probability of error. Our goal when estimating a company’s value is to reduce the margin of error, not to seek precision.

Valuation does not replace risk management—it is insufficient to make an investment decision and does not tell us how much to invest.

As we have seen, banks are no exception and have peculiarities in analysis and valuation. There are no excuses for not knowing them.

I’ve been going through your free posts and have really enjoyed the quality of material mixed with writing style. A great example is the first 100 words of this post which hooked me.