History despises order. Humans despise disorder. In that dissonance, human history was born. Basically, our civilizational narrative is a timeline of wars.

Our age is no exception, though present-day conflicts have more dimensions. Kinetic wars are complemented by cyber, informational, and trade warfare. Every aspect hides lucrative opportunities for adventurous investors.

Today, I present you with such an idea. The topic is the intersection between critical minerals and geopolitics.

China + trade wars + critical minerals = Asymmetric opportunity

Mandatory ingredients for an asymmetric idea in commodity complex: a few major suppliers and capital starvation. If state actors are authoritarian, even better. Another bonus is if the country has systematic political and economic issues.

That paragraph summarizes one of the decade's major themes: geopolitical fragmentation and critical minerals. Let’s give a couple of examples. The chart below (via Bloomberg) shows the origin of critical metals by country of production.

The list is not exhaustive, yet it clearly illustrates how one country can dominate the market of a particular critical mineral.

However, not all critical minerals producers are equal. Some are more equal than others, as the old communist saying goes. I mean the acute dependence on China for the supply of several critical metals. The latter become a geopolitical lever in the trade wars between the Great Powers.

How dependent are the US and China? The pie chart below represents the US's reliance on Chinese critical metals (via Visual Capitalist).

In some instances, China processes more than 50% of the minerals and is responsible for 100% of the supply.

As I repeatedly said, the EU is the patsy on the poker table between the Great Powers. The following map confirms my observation.

The Old Continent imports the majority of critical minerals from around the globe. However, China is the leader in REE and more specialized minerals.

Since China controls more than 30% of the supply, a plausible scenario is that the CPP restricts or bans exports. This means cutting supply for the EU and the US, which have relied heavily on China for the last two decades. The result is almost non-existent infrastructure for extracting and processing critical metals.

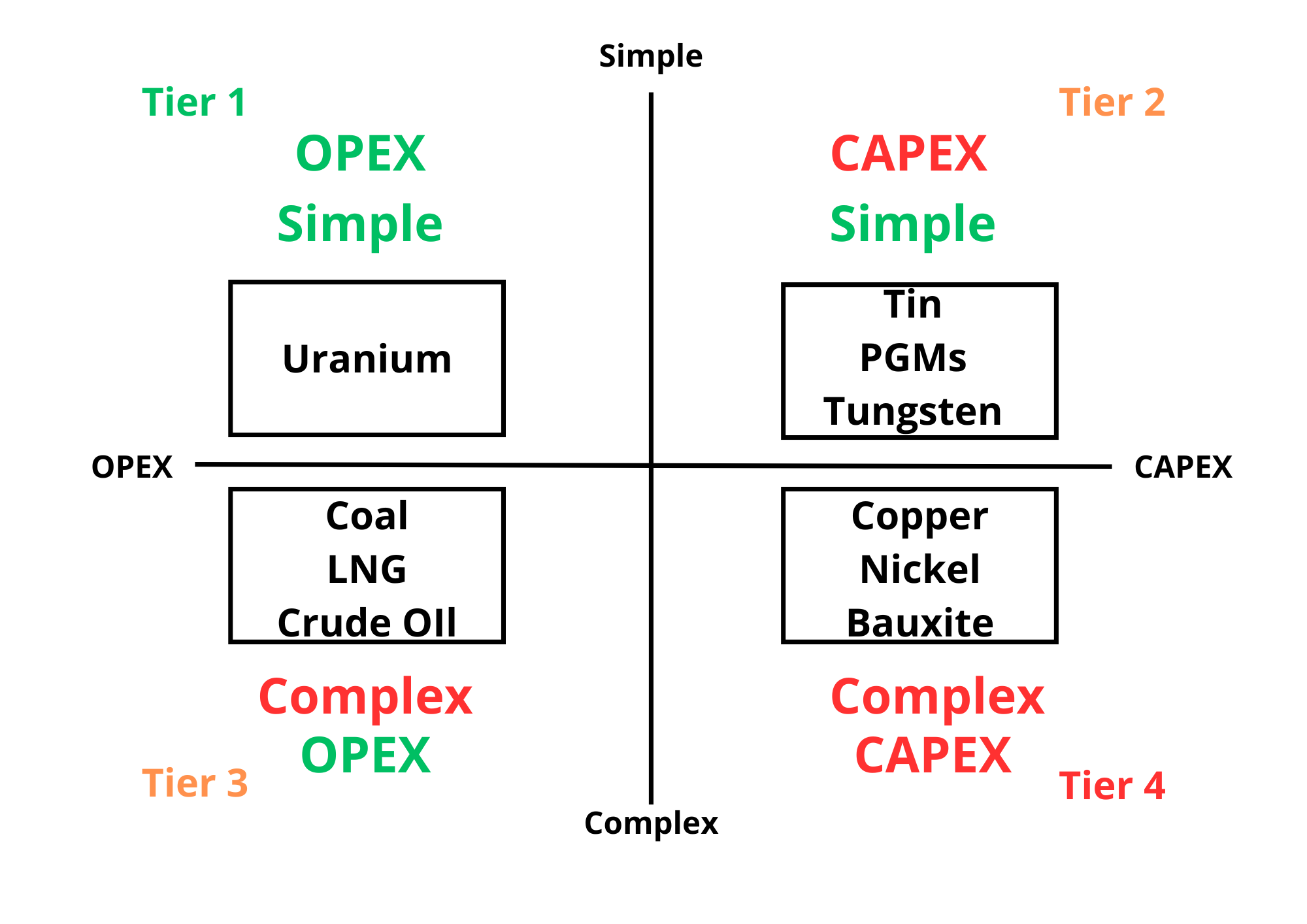

One of the best things about those metals is that they belong to the “Simple” category.

In other words, their markets have a few moving parts. China is the driving gear. So, a minuscule change in CPP's restrictive export policy may cause epic shortages of critical metals.

A bonus tip: the more authoritarian the dominant players, the more plausible future supply cuts. China ticks that box, too.

To sum up, having well-known supply variables makes creating plausible scenarios less challenging. On one side of the scale, we have complex industries like fossil fuels with many variables, while on the other side, we have markets like uranium with a few well-known parameters.

Critical metals dynamics are reminiscent of the uranium market. One state actor, China, controls most of the extracting and processing of critical minerals, making supply forecasting less difficult than the crude oil market.

China’s ability to restrict supply gives investors another edge. Knowing that the CCP can block critical metals exports anytime gives us an advantage. It improves our timing by telling us when the least wrong time to buy is.

Let’s give a fresh example. On August 14, 2024, China announced its decision to curb antinomy exports. China is the number one antimony producer, accounting for 48 percent of global production and 63 percent of U.S. antimony imports. Antimony is critical for the defense industry, particularly for armor-piercing ammunition, precision optics, and electronics, including semiconductors.

Commencing September 15, export restrictions will go into effect for six antimony-related products. The scope of the limits is unclear for now. However, in a press release, China's Commerce Ministry says that the government opposes any country from using exports from China “to engage in activities that undermine China’s national sovereignty, security, and development interests.”

That being said, it's worth discussing the China-US trade war. A conflict timeline is a map showing potential scenarios. Of course, the map is not the territory. So, do not take the sequence of events for granted. Treat every scenario with a different level of credibility.

China and US trade wars history 101

Trade wars are not new. Restricting critical supplies for your enemies boosts the probability of winning the battle (and the war). It is a tip-for-tat game. The US sanctions Chinese chip manufacturers, and the CCP restricts critical mineral exports.

Trade wars between China and the US started in 2018. One of the most impactful restrictions was export controls imposed by the US in October 2022. These controls aim to constrain China’s access to and ability to manufacture advanced semiconductors.

These actions are part of the Biden Administration’s “small yard, high fence” strategy. Its goal is to ensure “strategic competitors cannot exploit American and allied technologies to undermine American and allied security.” This includes microchips.

China has a few options for striking back. One of them is imposing restrictions on critical minerals exports. The country remains dominant in extracting and processing myriad critical minerals, giving CCP enormous geopolitical leverage.

Since 2022, China has decisively followed the US's adverse actions, implementing sanctions on various materials. It started with gallium and germanium in August 2023 and then graphite in September 2023.

It's worth mentioning that, for now, China has not instituted direct export restrictions to specific countries. Beijing uses a soft yet decisive approach to impact its strategic competitors. Nevertheless, the prices of affected minerals increased because of the rising fear of further restrictions. Western customers had to seek alternative suppliers as a backup in case of trade war escalation.

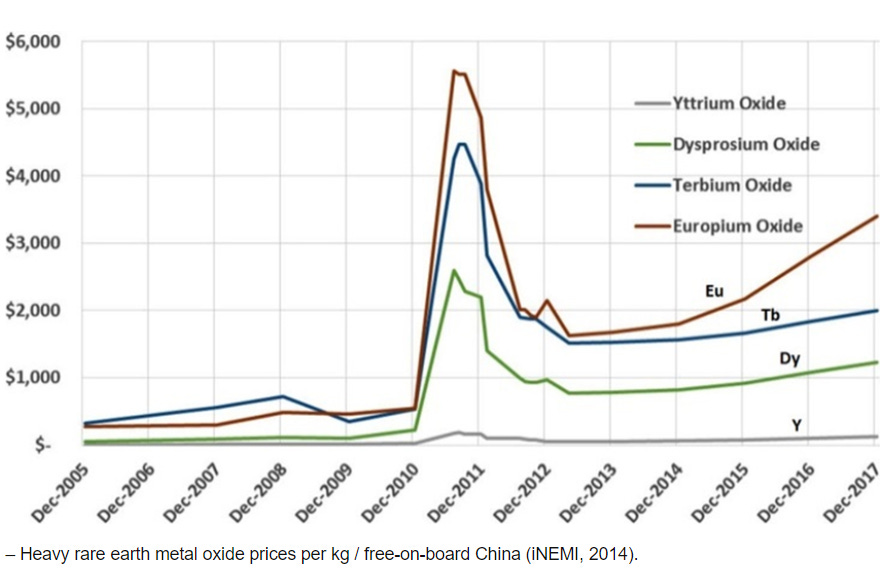

This is not to say that China never used mineral exports as a tool of retaliation. In 2010, after a Japanese ship collided with a Chinese fishing vessel, China stopped REE exports to Japan for two months. As a result, the price of REE skyrocketed.

The chart above illustrates the powerful consequences. Given that the decade is dominated by rising global chaos, I expect more retaliatory measures between Great Powers.

The trade war is a tip-for-tat game. So, its intensity depends not only on China but also on the US. Both state actors’ actions form a reflexive cycle of cause-effect. Therefore, to create scenarios for the future, we must consider China and the US equally important. That being said, a drastic measure by the US toward China can indicate another round of critical mineral restrictions from the Chinese side.

The next election is a few weeks away. Hence, as analysts, we must focus on the odds of who will be the next inhabitant of the White House.

The trade war between China and the US has just started. However, the direction and intensity of the restriction exchange are not predetermined. Democrats and Republicans will keep the present status quo, adding tariffs and export restrictions for China. Nonetheless, there are nuances regarding intensity and magnitude.

According to various political analysts, Trump is expected to go “nuclear” on tariffs, while Harris is projected to take a softer approach. The more intense the US tariffs/restrictions, the more decisive the Chinese response. Depending on the severity of US action, I would not be surprised to see retaliatory actions aimed at the US.

To recap, critical minerals have become a powerful tool to exert power over strategic adversaries. China is best positioned to exploit that advantage. On the other hand, the intensity of the measures depends on the other actors, primarily the US.

This makes investing in critical minerals an event-driven bet on a macro scale. Simply put, we wager on CCP causing global disproportional imbalances because of further export restrictions. The best thing is we have multiple options, from copper through antimony to rare earth elements.

Final Thoughts

Trade wars represent event-driven investing at a macro scale. Punitive measures have the potential to spark a sudden deficit in an already capital-starving industry. Critical minerals mining matches perfectly the description.

China is not the only country in that game. Russia has a lot to offer. Think about uranium, nickel, and palladium, just to name a few. Russian President Putin proposed restrictions on uranium exports a few weeks ago. Let’s not forget that sanctions work both ways.

Yesterday, the news came out that the US asked G7 to consider limiting imports of Russian palladium and titanium. The palladium price spiked by 8% in a few hours. The game of sanctions has just started and the best is yet to come.

Position accordingly.

Everything described in this report has been created for educational purposes only. It does not constitute advice, recommendation, or counsel for investing in securities.

The opinions expressed in such publications are those of the author and are subject to change without notice. You are advised to do your own research and discuss your investments with financial advisers to understand whether any investment suits your needs and goals.