How (not) to make dumb investing decisions?

The advantage of boring and "emotionless" markets

Kevin Kelly says, "Don't be the best; be the only." How can we apply this maxim to the markets?

I look for markets, instruments, and strategies most people are indifferent to. The word indifference is the key.

Hated and adored markets are sources of informational and emotional noise. Thus, our emotional capital, which is no less important than financial capital, is quickly exhausted. At that stage, we are reactive, awaiting the next emotionally charged bytes, hoping it will tell us what to do.

Take, for example, the AI hype. The emotions surrounding this market blind most investors because of the never-ending flow of information.

This is not a tirade against AI stocks but against our inability to think independently. The next hot market could be uranium, gold, banks, or whatever. It is not the market that matters but market participants' irrational behavior.

Why do the crowded markets so easily delude investors?

Emotions

The infinite flow of information surrounding popular markets triggers an emotional response. Every byte is a prompt that pushes you to react. Accordingly, the more popular a market is, the more information is blasted around hence, more emotions are triggered.

Emotions are energy. Energy infatuate. Infatuated away, we lost ourselves. Independent thinking is thrown away. We don’t act but react.

Now, we are at the mercy of the collective. We seek confirmation for our (in)actions in others. Accordingly, the solace and comfort of the group when things get tough, as they inevitably will, are everything we crave.

Emotions amplify the herding effect. Therefore, popular markets, where the crowd is, are increasingly efficient. Hence, Apha extraction is getting harder. There is less Alpha per market participant, resulting in fierce competition for a few pips of advantage.

Reminder: markets are never absolutely efficient or inefficient. They oscillate between efficient-inefficiency and inefficient-efficiency.

At the other end of the (in)efficiency scale are markets that no one looks at except a handful of specialized funds and retail enthusiasts. Information flow is kept to a minimum in these places, hence the emotions. Thus, our emotional capital remains intact. When we are not in the center of an emotional storm, it is much easier to avoid inadequate decisions. Therefore, we are a step closer to the adequate ones.

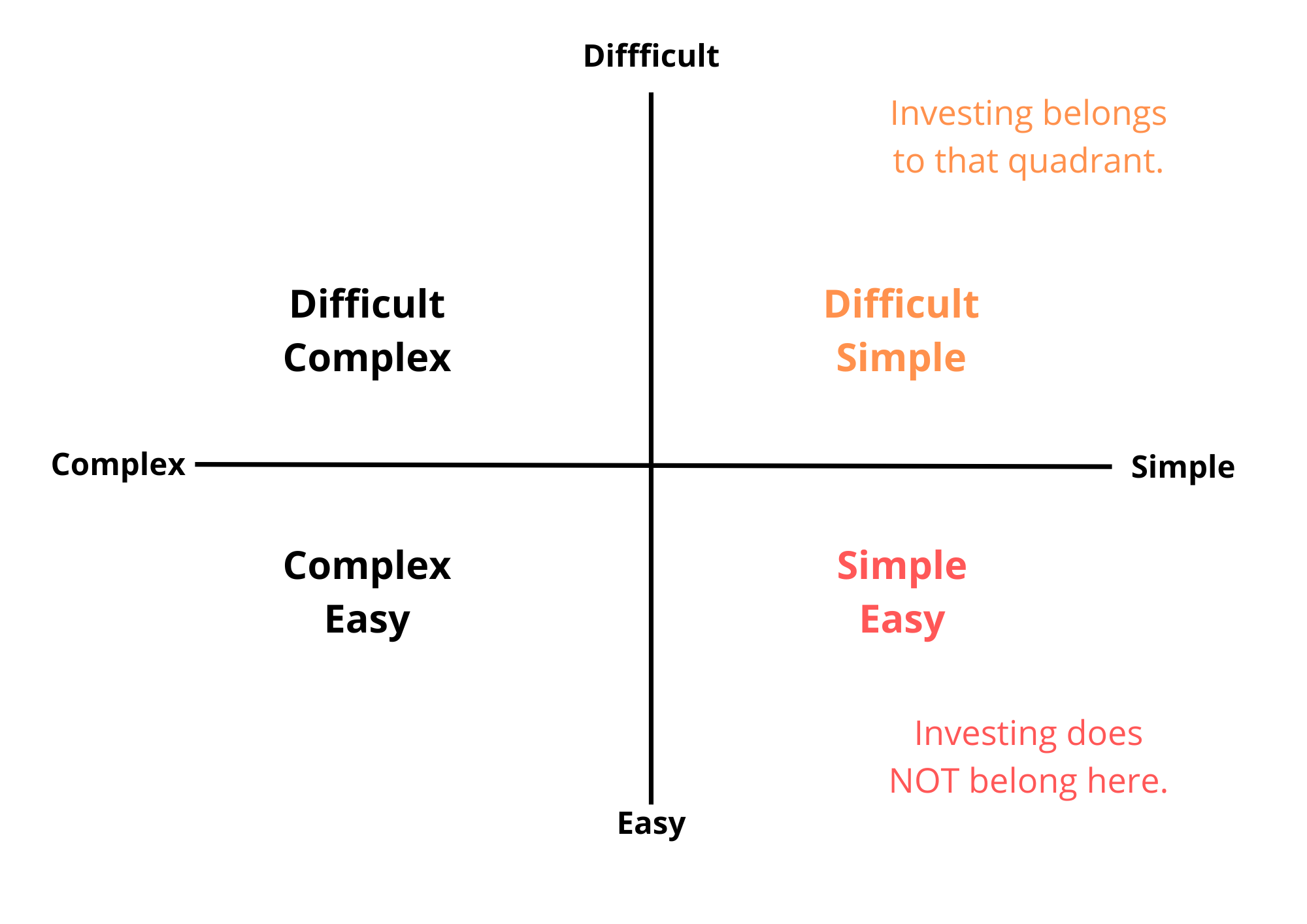

Investing in boring and “emotionless” markets is a feasible approach to protecting our emotional capital. Then, the game goes from complex and difficult to simple and difficult. Yes, it never becomes simple and easy. Investing belongs to the first quadrant.

If we are unable to control the flow of information, our ability to make adequate decisions declines. The quality of decisions determines the quality of outcomes.

Decisions

When we pick a street, we choose not to go down every other street. This means that everything that happened on the alternative routes is unavailable.

It is the same in the markets. By choosing to invest in Apple (for example), we decide not to invest in Cameco, Barrick, Bitcoin, etc. This means we will miss everything in these markets—the ruinous declines and epic ascents.

But the interesting part doesn't end there. Buying is only one of three actions we take in the markets. The other two are selling and waiting.

Accordingly, they also have consequences - profit or loss. Yes, even the decision to wait may be good or not so good. In summary, we face six options, depending on what action we take and its outcome. :

Purchase leading to profit

Purchase leading to loss

Sell leading to profit

Sell resulting in loss

Waiting leading to missed profits

Waiting leading to missed losses

We constantly make decisions in the markets, and their quality depends on our emotional capital. Popular markets are charged with emotions, which inevitably exhaust our emotional reserves. To protect our emotional capital, we must stay indifferent to collective emotions.

Then, how to achieve it?

The solution

My solution is simple: I avoid popular markets and do not let the crowd get me carried away. There is another option—to be immune to the collective's influence. It's easier said than done. While there are people capable of that, I am not one of them. That's why the best solution for me is to stay away from the emotional markets.

I operate in markets that do not arouse any interest in 99% of market participants. Regular readers know that the more esoteric a market is, the more interesting it is to me. Over time, I've realized that this has several advantages; one is that it insulates me from the emotionally filled information flow inherent in hot markets.

Final Thoughts

We do not understand reality. We are only aware of its simulation, i.e., hyperreality. The information flow of news, podcasts, posts, and articles represents tiny fragments of the simulation—I stress, not of reality.

And yet we have the courage, or the arrogance, to claim that we understand reality. We know nothing. Life is a mystery.

Being successful in markets, business, and life is not proof that we know something.

Deciding we've decoded the game is even easier in popular markets. Inexperienced investors get intoxicated by their quick and easy wins. The last two years are an illustrious example. Purchase an equity with AI attached to its name and ride the wave.

However, two things are growing in proportion to the new market tops: the emotional charge and our inability to think critically. This is an explosive combination.

If we want to play the game long-term, we have no excuse not to think critically. Then, we face two options. Either we develop emotional immunity or play “emotionless” markets. There is no middle option.

I prefer to be alone with my thoughts in a room rather than in a crowded stadium where everyone screams. I want to be the only one where I am, not another one where everyone is.

Regardless of our path, the final destination is independence in thoughts, decisions, and actions—independence from the drama of the crowd.

On the markets, we are wrong until proven otherwise. So, take the above thoughts with a grain of salt.

Everything described in this report has been created for educational purposes only. It does not constitute advice, recommendation, or counsel for investing in securities.

The opinions expressed in such publications are those of the author and are subject to change without notice. You are advised to do your own research and discuss your investments with financial advisers to understand whether any investment suits your needs and goals.

Very insightful, thanks a lot