How to invest with the Rothschilds?

Old money idea for TheOldEconomy investors

The old economy walks hand in hand with old money. Think about Rothschild and banks, Krupp and steel, Rockefeller and oil.

Old money dynasties are one of my favorite rabbit holes. Besides the household names mentioned above, there are secretive families. Safra, the Syrian-Lebanese banker family, has a fascinating history. However, the Rothschild dynasty remains synonymous with global wealth.

This is TheOldEconomy blog, where we seek Alpha in the old economy. The relevant question is: How can I invest with Rothschilds?

As far as I know, there are only two available options. The first is a self-managed trust, RIT Capital Partners (LSE: RCP), while the second option is a broad category of mutual funds managed by the Edmond de Rothschild Group.

Years ago, we had more options, but two of the enterprises became private: Rothschild & Co and Edmond de Rothschild S.A. I was a happy investor in the first one until the bank announced that it was going private in 2023. Edmond de Rothschild Group went private in 2019.

This is the first chapter of my adventures in the old money world in a quest for Alpha. The company in question is RIT (Rothschild Investment Trust) Capital Partners.

Rothschild Investment Trust

Everything about RIT screams old money. The company’s headquarters occupied Spencer House in London, one of the few remaining townhouses from the 18th century.

The company was founded in 1961 by Jacob Rothschild as "Rothschild Investment Trust." In 1980, there was a conflict between Jacob Rothschild and Evelyn de Rothschild, then the head of N M Rothschild & Sons. Evelyn de Rothschild withdrew the money invested in the Rothschild Investment Trust and forbade the trust from using the name Rothschild.

Jacob left the Board of N M Rothschild & Sons and took complete control of the Rothschild Investment Trust. In 1982, the company bought the "Great Northern Investment Trust" and was renamed "RIT & Northern." Jacob transformed the enterprise into a publicly traded investment trust, RIT Capital Partners, six years later. In 2012, RIT acquired a 37% share of Rockefeller Financial Services. The trust has been a member of the World Gold Council since 2010.

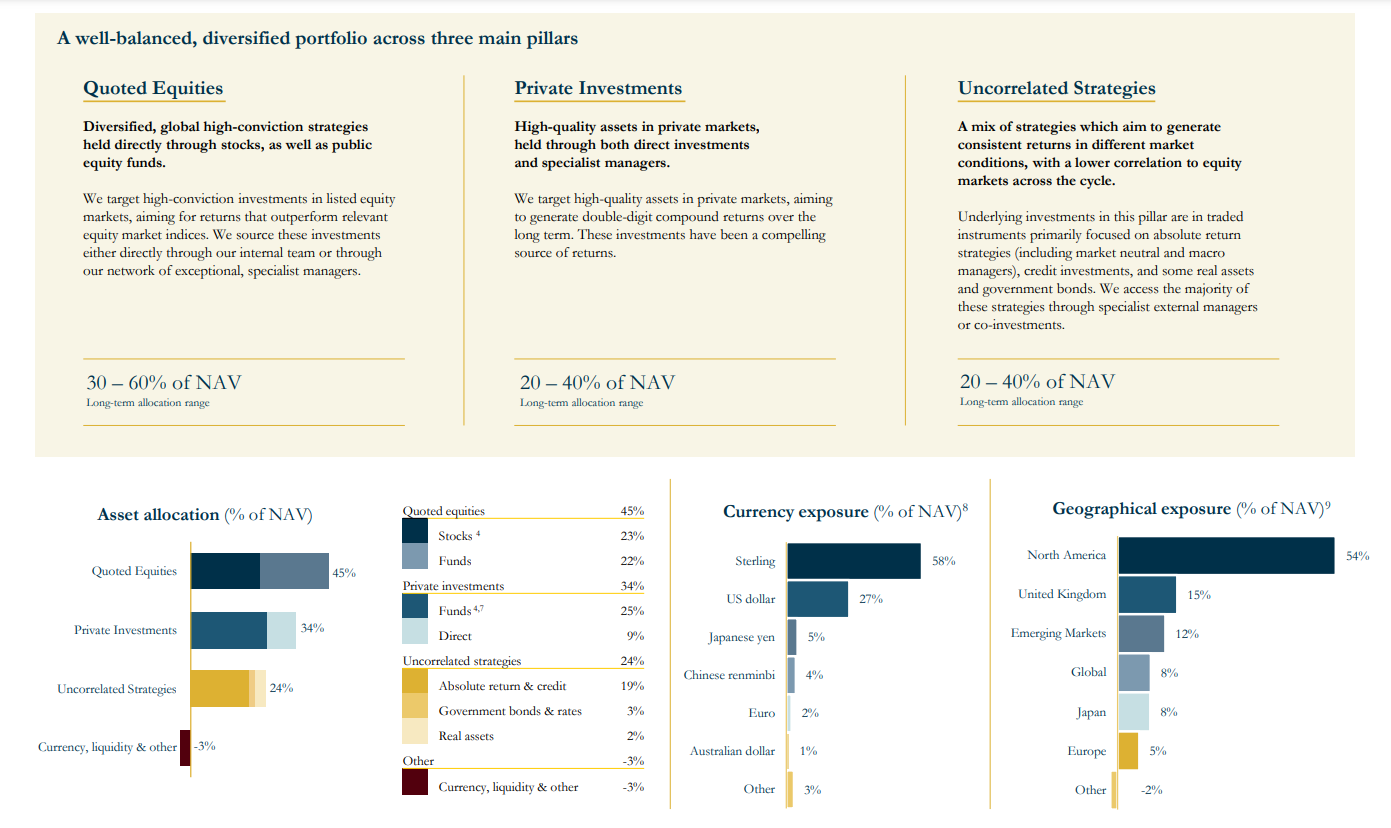

RIT is listed on the London Stock Exchange’s FTSE 250 Index and is one of the UK’s prominent investment trusts. The company’s strategy is broadly diversified by themes, regions, and strategies.

The three portfolio pillars are publicly traded equity, private investments, and uncorrelated strategies. Quoted stocks and private investments account for nearly 80% of the portfolio. The remaining is scattered among tangible assets, absolute return strategies, and government bonds.

Among the publicly traded names in RIT's portfolio are curious findings like Golar LNG and Talen Energy Corporation. However, the more significant positions are blue chips like Mastercard and Amazon.

The largest shareholders of RIT are:

Nathaniel Rothschild: 20.7% stake

The Rothschild Foundation Owns:10.8% stake

J. Rothschild Capital Management Ltd.: 8.6% stake

Evelyn Partners Group Ltd: 5.5% stake

Five Arrows Ltd.: 4.7% stake

Rothschild-related individuals and entities own nearly 50% of RIT’s equity. By owning a share, you become a partner with the Rothschilds.

The good thing about investment vehicles is that estimating value is straightforward. Simply calculate the value of each publicly traded holding. In RIT’s case, however, the portfolio contains private investments and alternative strategies, making NAV estimates challenging. For that reason, I will use the company’s figures.

The most recent data shows that RIT price-to-NAV discount is approximately 27%.

This significant discount means investors can purchase RIT shares for 73% of the underlying asset value. It's worth noting that RIT has historically traded at a premium. The current PNAV discount is attributed to concerns about performance, private investment exposure, and high costs.

RCP's NAV total return has lagged behind broader market indices for the last few years. The trust's private investment positions contributed to the poor performance. The trust's allocation to private investments has increased to about 35.9% of NAV, raising concerns about liquidity, risk metrics, and valuation credibility.

Unlike publicly traded names, private investment valuations are disputable. The information asymmetry is heavily skewed against investors, so we must take those values with a grain of salt. To be fair, this issue is not RIT-specific. All investment vehicles involved in private investments face the same challenges.

To address the issues with private investments, the company’s management plans to reduce their proportion to between 25% and 33% of NAV over the next two years.

On the positive side, private investments are convex by nature. They are call options without expiration on (potentially) profitable enterprises. If selected properly, they can deliver outstanding payoffs. RIT has a long and successful track record of cashing its private investments. In summary, the considerable discount is due to broad negativity toward investment trusts and private investments.

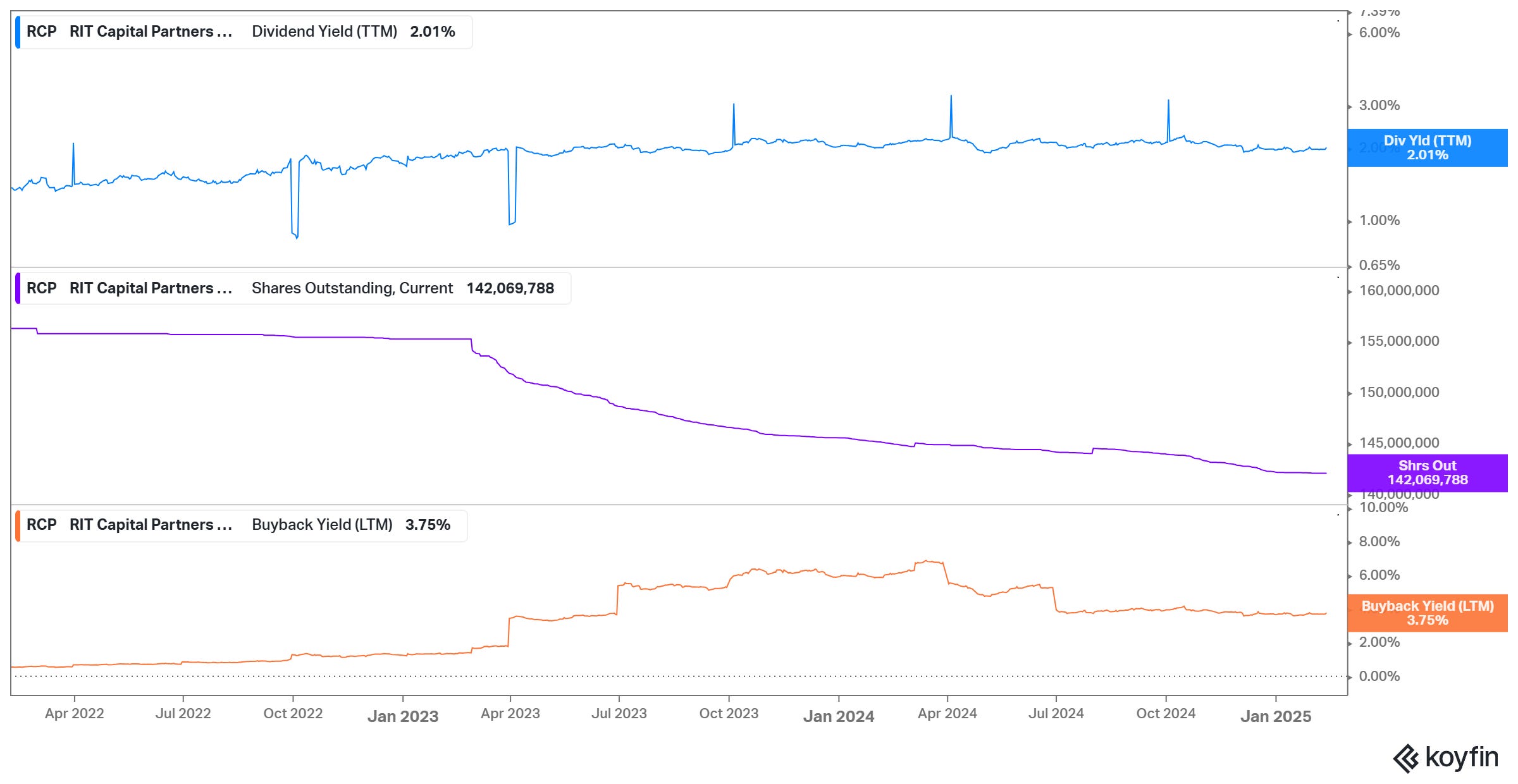

On a positive note, RIT’s management utilizes the discount with active share buybacks. Look at the chart below:

I like buybacks when executed properly, i.e., shares are repurchased at a discount to NAV. Thus, all per-share metrics are growing. At the end of the day, this is what matters the most for investors. In RIT’s case, I would like to see NAV growing per share. Attractive dividends come as a bonus to compensate for the risk taken.

Final Thoughts

Let’s make investing in the Old Economy great again. One of the more unorthodox yet logical approaches is to side with the old money. Unfortunately, Rothschild & Co. is no longer available to us mere mortals. It is a well-run investment bank that has delivered superior results for decades.

The good news is that we have RIT. Frankly, it is not as exciting as Rothschild’s investment banking branch, but it is lucrative enough. At a 27% discount to NAV, we get a diverse portfolio with instruments and strategies not available for the retail crowd. On top of that, we get paid to wait.

This was the first episode of my adventures in the old-money world. Another one is coming soon. Stay tuned.

On the markets, we are wrong until proven otherwise. So, take the above thoughts with a grain of salt.

Everything described in this report has been created for educational purposes only. It does not constitute advice, recommendation, or counsel for investing in securities.

The opinions expressed in such publications are those of the author and are subject to change without notice. You are advised to do your own research and discuss your investments with financial advisers to understand whether any investment suits your needs and goals.