Kazakh Oil and Gas Distressed Debt Play

The "Stans" as One of The Most Arcane Corners of Oil and Gas Game

I have a new rabbit hole to explore: oil fields in overlooked places like “Stans” in Central Asia and Kurdistan in the Middle East. Both regions face a range of risks, like corrupt politicians and geopolitical uncertainties.

Furthermore, many of the companies there are registered in the UK. Windfall tax, anyone?

Formally called the Energy Profits Levy (EPL), it was introduced in May 2022 in response to soaring energy prices and record industry profits. Initially set at 25%, the levy was raised to 35% in January 2023 and then to 38% in November 2024. The windfall tax is applied on top of the sector’s existing 40% tax rate, bringing the total tax burden to 78%—one of the highest globally.

Windfall taxes are one of the most parasitic ways to squeeze businesses. The goal is short-term political gains, while the price is long-term economic and energy issues.

Originally planned to end in 2025, the levy has been extended several times and is now set to expire in March 2030. The policy has raised billions for the Treasury but has drawn criticism from industry for reducing investment and increasing uncertainty.

Look at the terrible performance the UK Oil and Gas companies delivered over the last 36 months. The windfall tax has taken its toll on the industry.

An extraordinary tax burden and high political risks define the existence of the companies listed above.

Are those companies investable?

The short answer is yes.

The long one is the topic of today’s report. We are heading to Kazakhstan to search for asymmetric opportunities in the oil and gas fixed-income universe. Yep, today’s report is as esoteric as it gets.

Kazakhstan Oil and Gas Industry

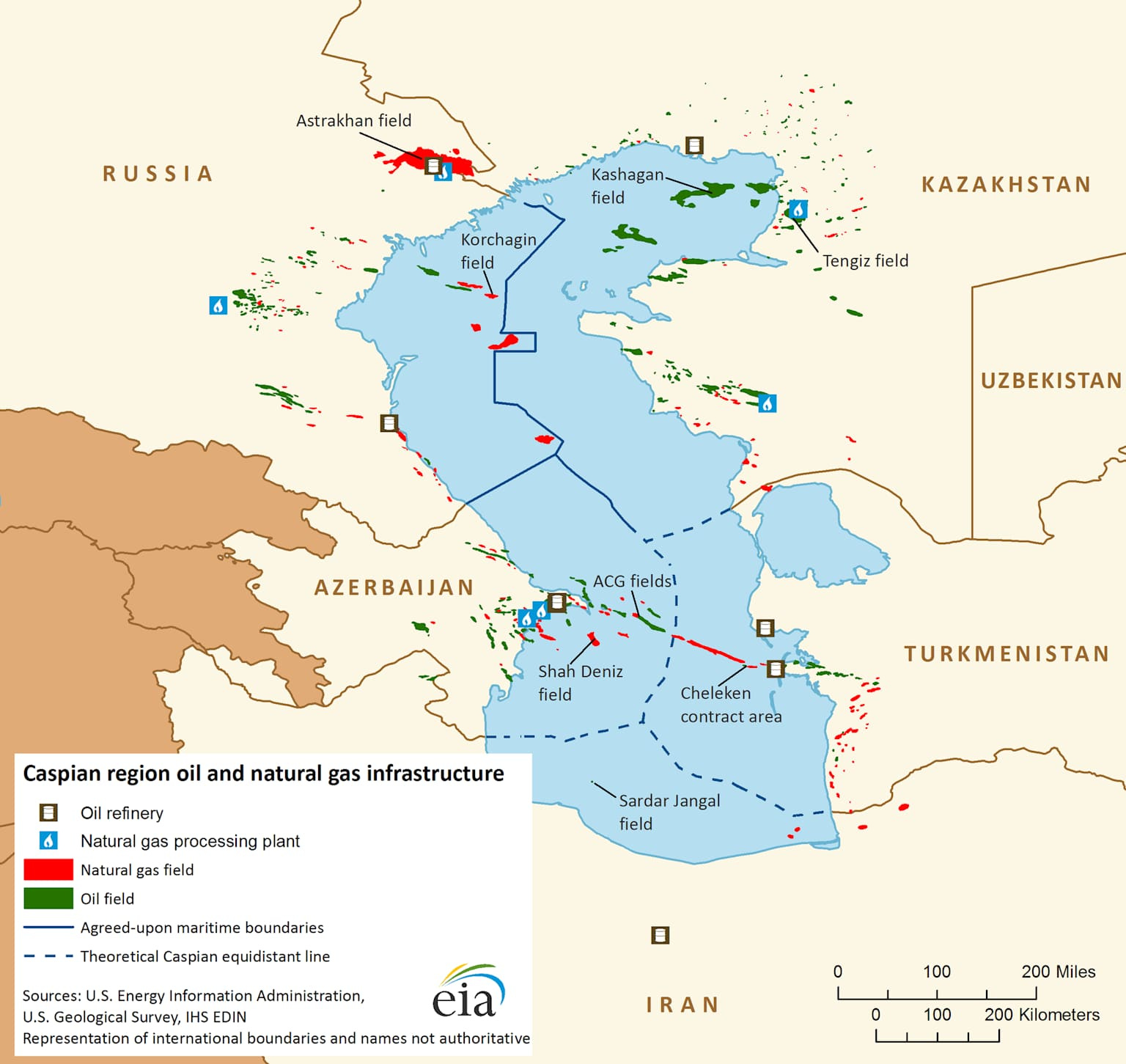

Kazakhstan, the world's largest landlocked country, is a significant oil exporter. Its location and resources are preconditions for elevated geopolitical risk. The country is locked between two of the Great Powers, Russia and China.

Additionally, the logistics of exporting oil from Central Asia are a factor to consider. No access to global ports with VLCC terminals. The only viable way is pipelines. They have their pros and cons.

One drawback is higher transport costs per mile compared to VLCCs. Furthermore, relying solely on pipelines located in foreign countries entails significant geopolitical risk. A case in point is the Ceyhan pipeline, involving the parties of Iraq, Kurdistan, and Turkey. The Kurdistan oil industry is a story for another time; today, we head to the vast Kazakh steppes.

Kazakhstan’s oil and gas fields have a history spanning over 125 years. The industry began in 1899 with the drilling of the Karashungul well in Atyrau, and by 1911, the Dossor field, developed by British entrepreneurs, brought international recognition. Soviet-era discoveries in the 1930s and post-war expansion laid the groundwork for industrial-scale production. After independence in 1991, Kazakhstan prioritized foreign investment, leading to landmark partnerships: the Caspian Pipeline Consortium (CPC) with Russia and Oman in 1992, and the 1993 “contract of the century” with Chevron for the Tengiz field.

Today, Kazakhstan holds 30 billion barrels of proven oil reserves, the largest in Central Asia. Its annual oil production is targeted at 104 million tons (approximately 2.1 million barrels per day) by 2025, driven by three major projects: Tengiz, Kashagan, and Karachaganak (image via Wikipedia).

Tengizchevroil (Chevron, ExxonMobil, KazMunayGas, Lukoil) operates Tengiz; North Caspian Operating Company (NCOC) manages Kashagan; and Karachaganak Petroleum Operating (Shell, Eni, Chevron, Lukoil, KazMunayGas) runs Karachaganak. These three fields now account for over 66% of national output.

Karachaganak was discovered in 1979, with significant production milestones in the 2000s, including integration into the CPC pipeline and multiple expansion projects. Kashagan, discovered in 2000, is among the world’s largest offshore oil fields and required advanced technology for development. Kazakhstan’s strategic partnerships, vast reserves, and steady production growth have established it as a vital player in global energy markets.

Today's accent is not on the large offshore fields in the Caspian Sea, but on smaller onshore projects located in the Northwest of the country.

A case in point is the Stepnoy Leopard field. It is a newcomer in the game. It is reflecting the region’s ongoing resource development beyond legacy giants like Tengiz and Karachaganak. The Leopard project is the essence of today’s distressed debt thesis. Its development is the line between life and death for the company behind it.