Market Overview Week 24

Market Overview Week 24

Bull market, LPG/LNG carriers, South Africa

The market tends to move in a direction causing the most pain to most market participants. 1H24 reminded us of the validity of that maxim.

The US indices have performed excellently, while the prophets of doom keep predicting the market crash. One day, their forecasts will be correct. However, until then, they stay on the fence, just talking smart.

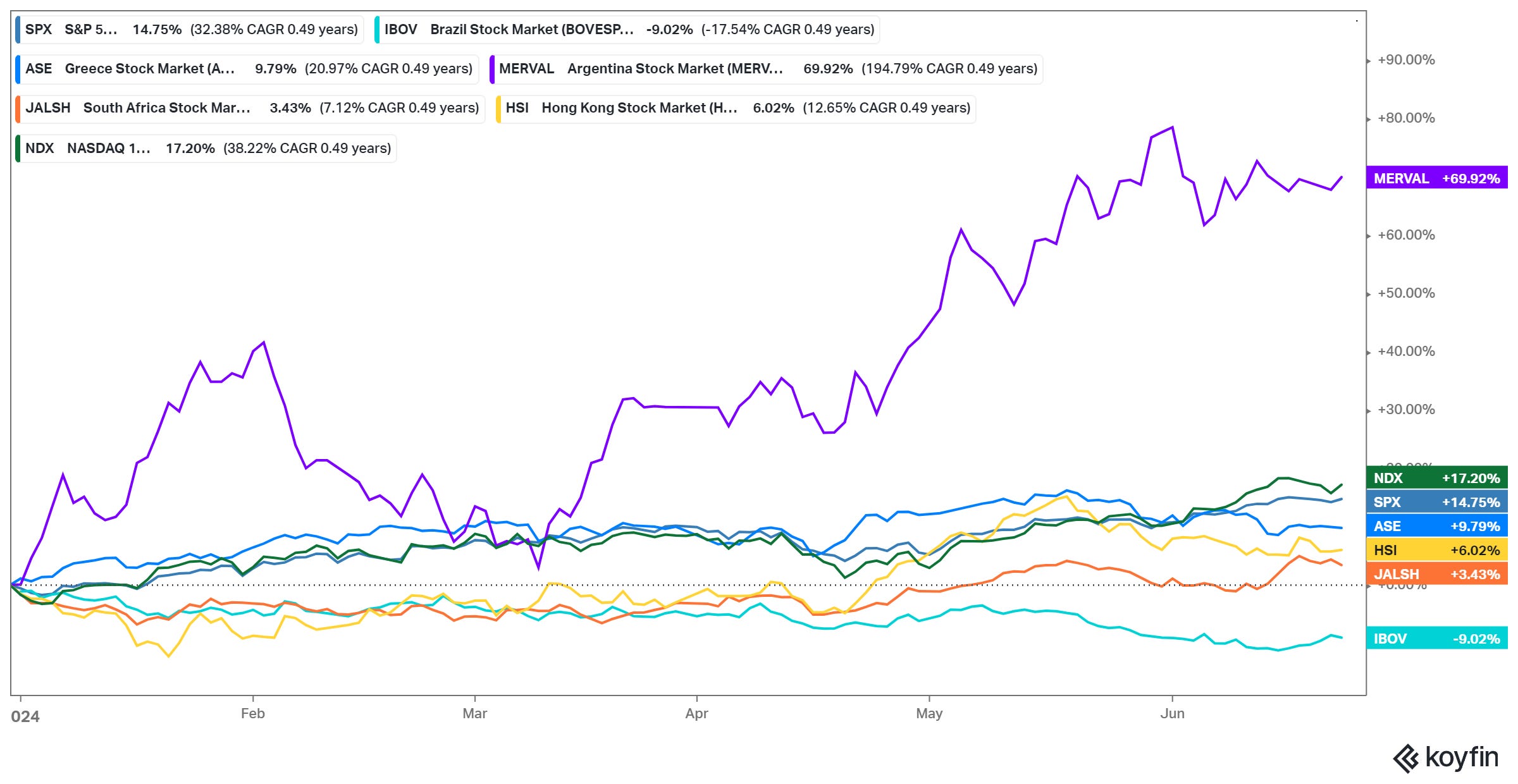

Argentina is the big winner, with a 69% YTD return. Neighboring Brazil is performing quite mediocrely due to the weak real against the US dollar. The Greek market also surprised investors for another year. Last but not least, the Hang Seng index has started to wake up.

The elections in South Africa brought an expected surprise—the African National Congress, ANC, for the first time, did not win with an outright majority. The ANC formed a coalition with the Democratic Alliance, DA, the party governing the Western Cape Province. The DA is expected to introduce pro-business measures without populism. Accordingly, investors’ interest in South Africa is anticipated to return.

Liquidity is a mandatory prerequisite of a bull trend. So far, the fiscal extravaganza is working. The governments of China and the United States - the two largest economies - have successfully injected funds through fiscal stimulus.

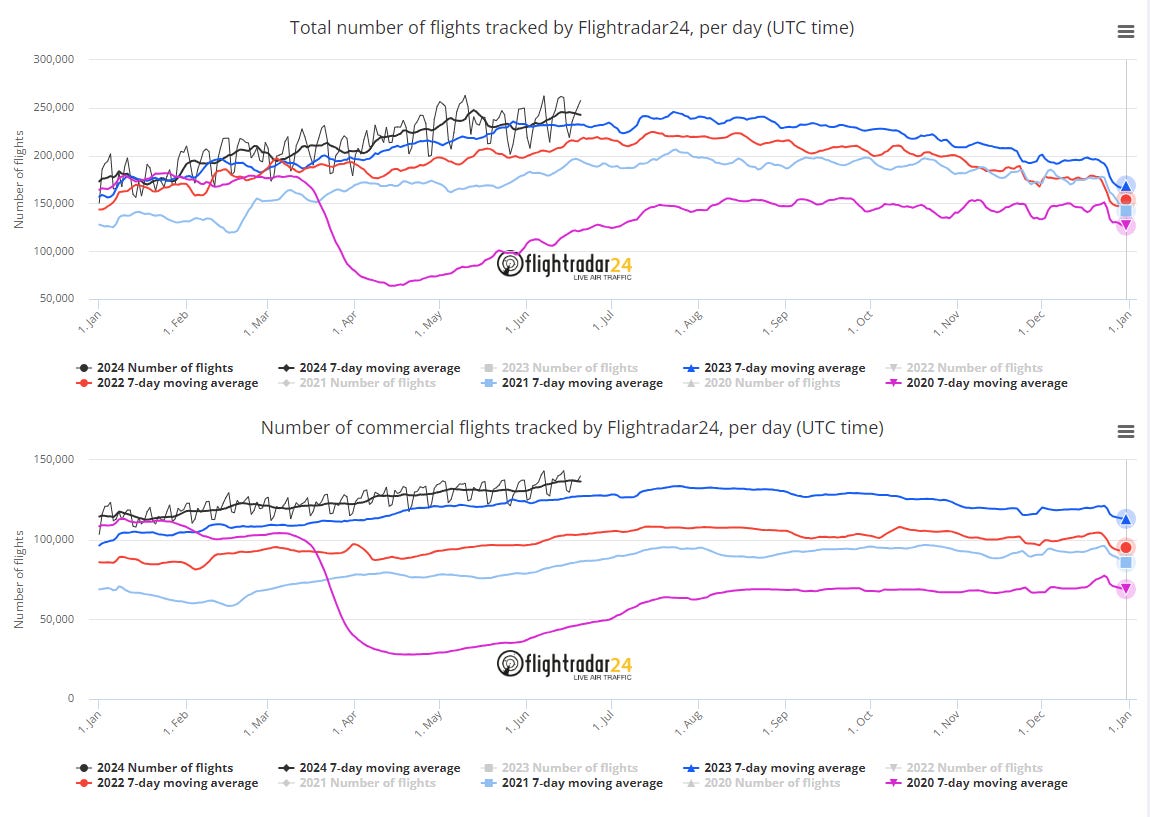

The number of commercial flights is a good enough (not perfect) indicator of the strength of the global economy.

In 2024, flights passed the record levels of 2023.

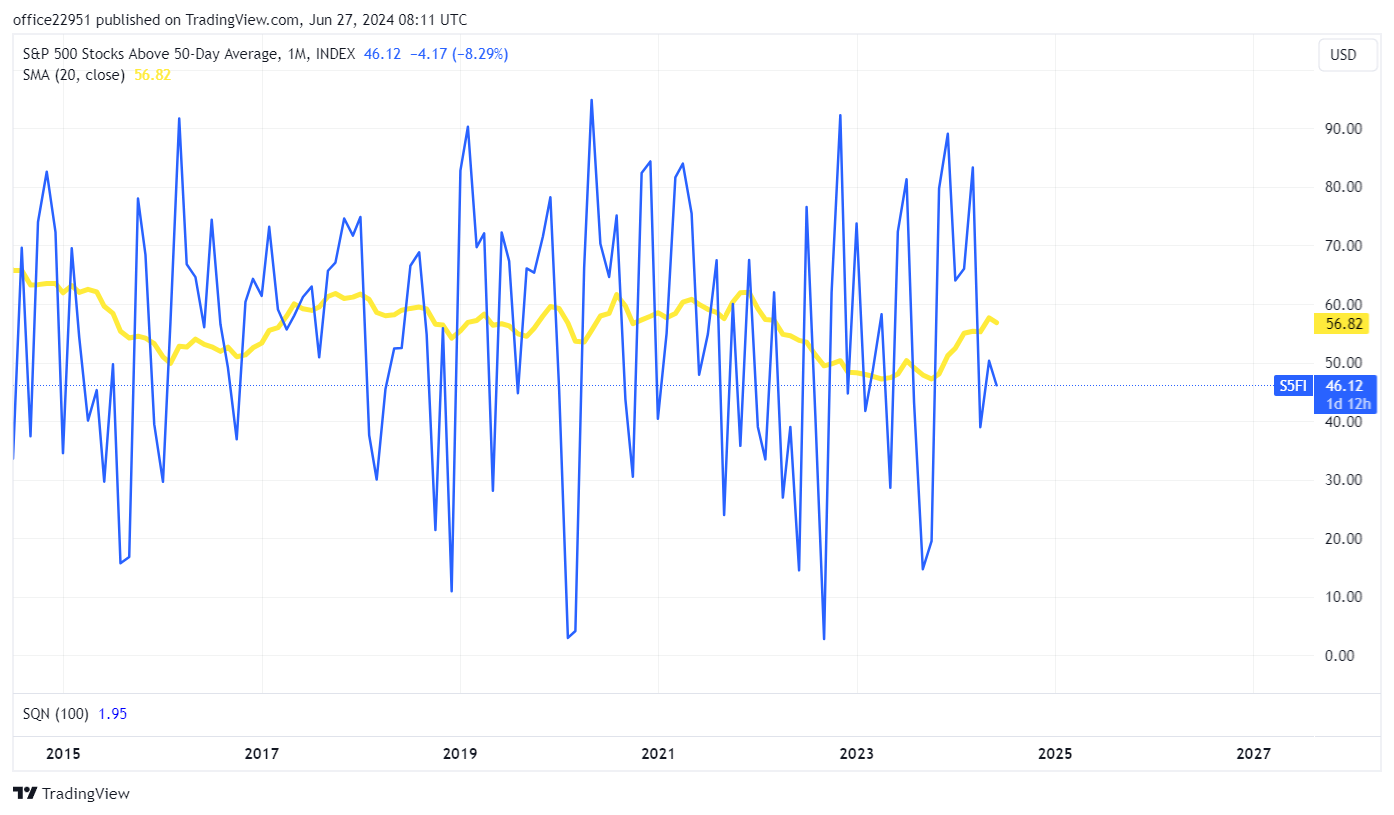

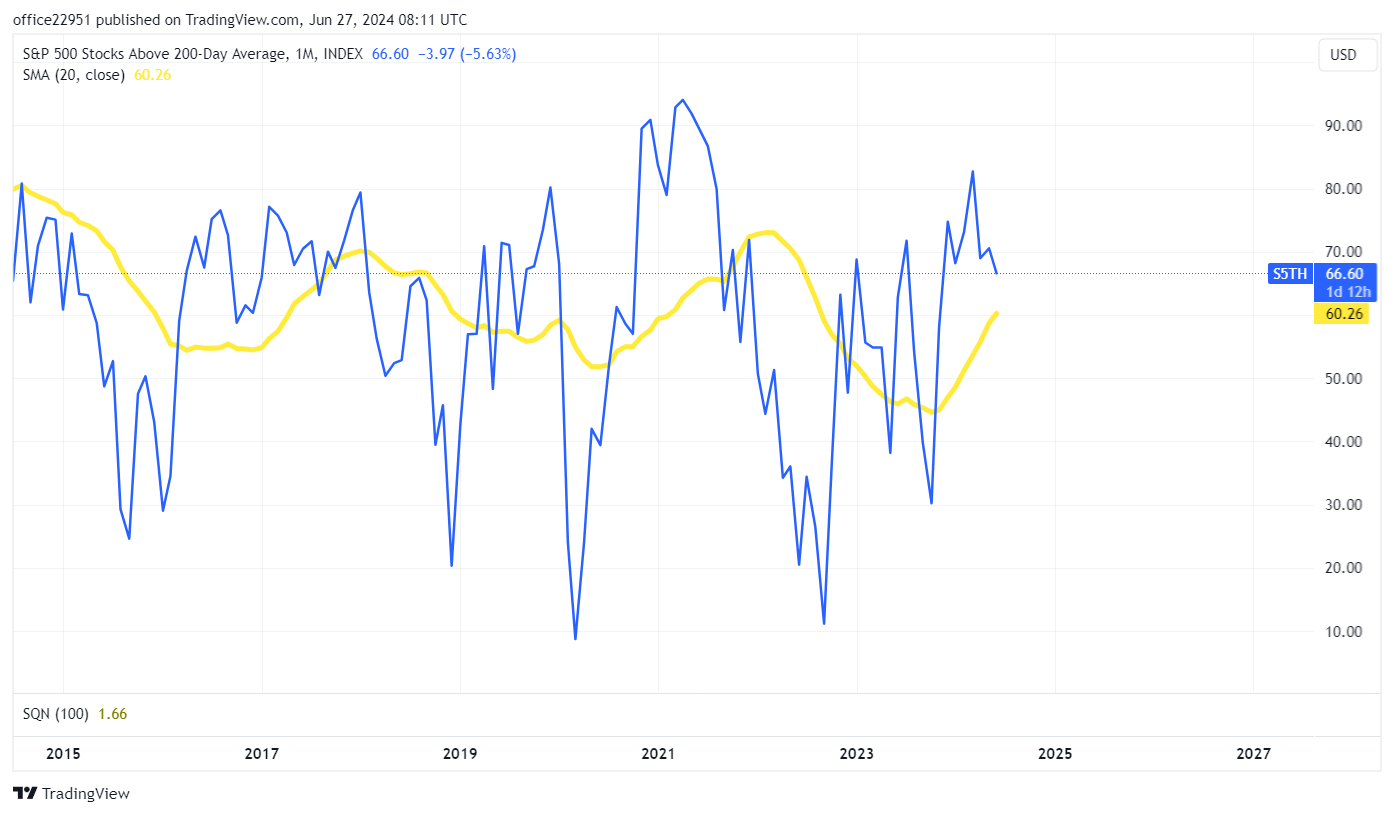

The new highs in the markets are not expected to be the last. The number of companies above the 50 and 200-day moving averages has not reached limits, suggesting extreme positioning.

Stocks above 50/200 MA (moving average) are around their averages over the last 20 months. In summary, the generals (MAG7) are leading, and the soldiers are still following.

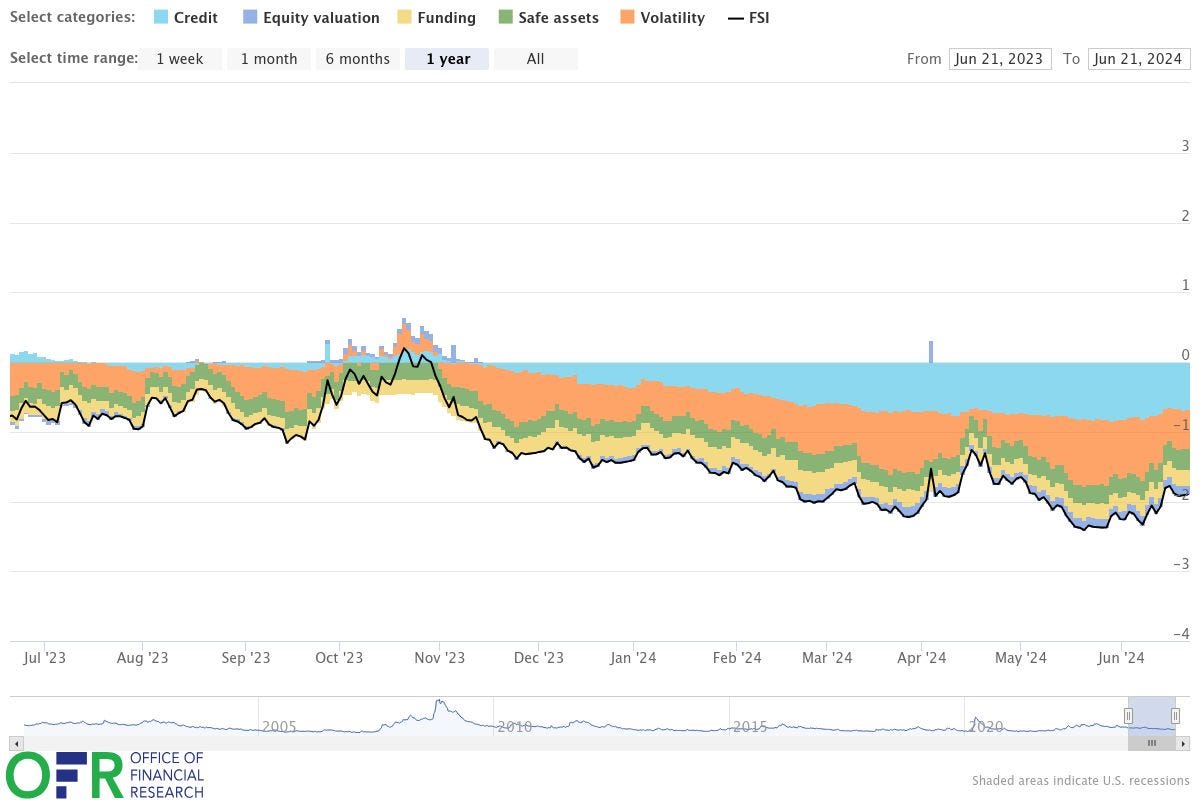

Let's take a look at the OFR indicator.

Far from indications of a trend reversal. Of course, this does not cancel a healthy correction in the coming weeks. However, there are no indicators of an imminent bear market. Bears are more likely to stay on summer vacation next.

So, it's time for some esoteric investing ideas.

What do shipping companies and Russian natural gas have in common?

Ice Class LNG carriers.

Ice-class LNG carriers’ demand is poised to grow. The supply, on the other hand, is getting more constrained, driven by the following factors:

Gas carriers with the last generation propulsion have an advantage over ships with steam turbines.

LNG terminals Yamal and Artic 2 require ice-class ships. And most of those have steam turbines.

No matter the propulsion system, ice-class ships are becoming increasingly in demand.

Sanctions imposed on Russia prevent the construction of new such ships at the Zvezda shipyard.

So, a limited supply and growing demand for ice-class gas carriers exist

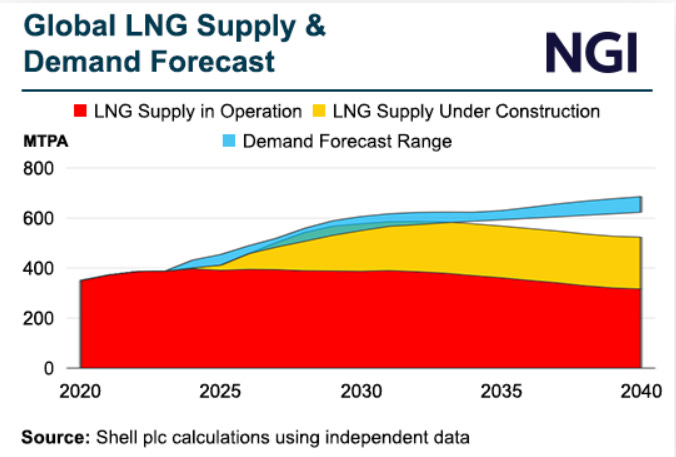

The factors driving natural gas demand can be summarized in three lines and one graph:

Green energy – together, nuclear power plants and LNG power plants are the most environmentally friendly

The Global South - a growing population that wants to live better

Geopolitical entropy - disruption of supply lines, creation of new political and economic alliances, and collapse of old ones

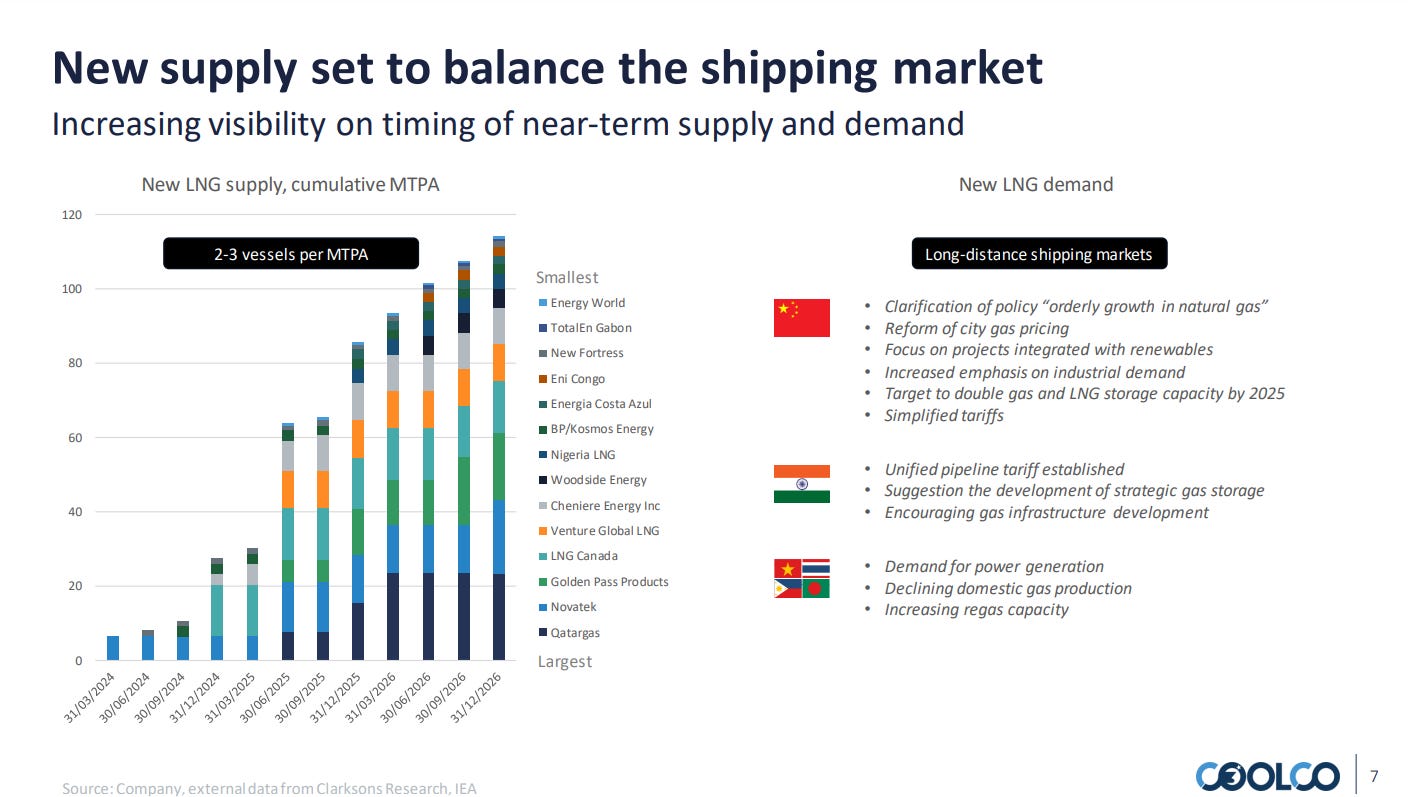

Liquefaction capacity will grow by 300 MTPA, or 60%, over the next six years. Cool Company's last presentation provided an excellent preview of future LNG demand and its impact on LNG carriers.

From 2024 until 2026, the LNG supply will grow by 110 mtpa. Every mtpa requires 2-3 new LNG vessels. Simply put, the LNG demand growth rate exceeds the LNG supply growth rate.

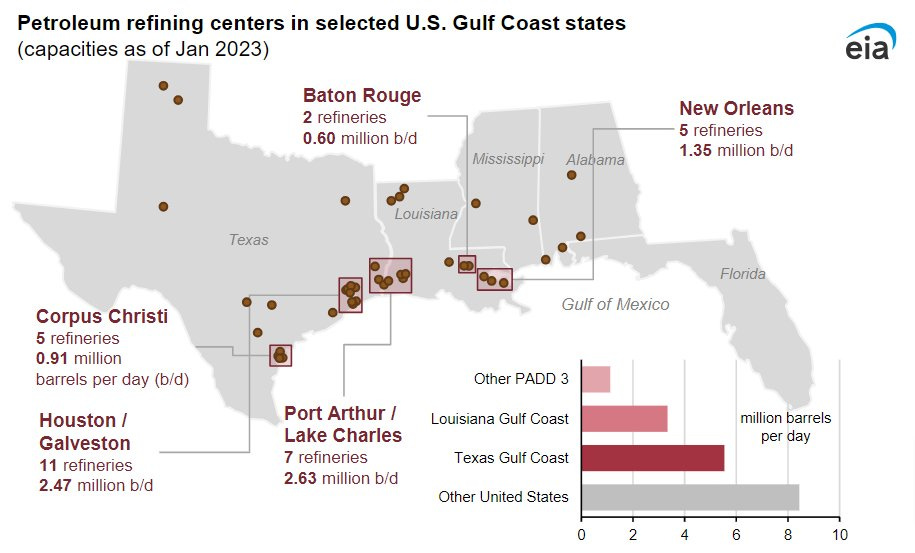

The US is the largest exporter of natural gas, followed by Qatar, Australia, and Russia. The US leads not only in this category; in recent years, it has established itself as a significant exporter of LPG.

China, Japan, and South Korea are the primary consumers of US propane/ethylene/ammonia. More than 90% of US LPG/LNG export terminals are in the Gulf of Mexico and East Coast.

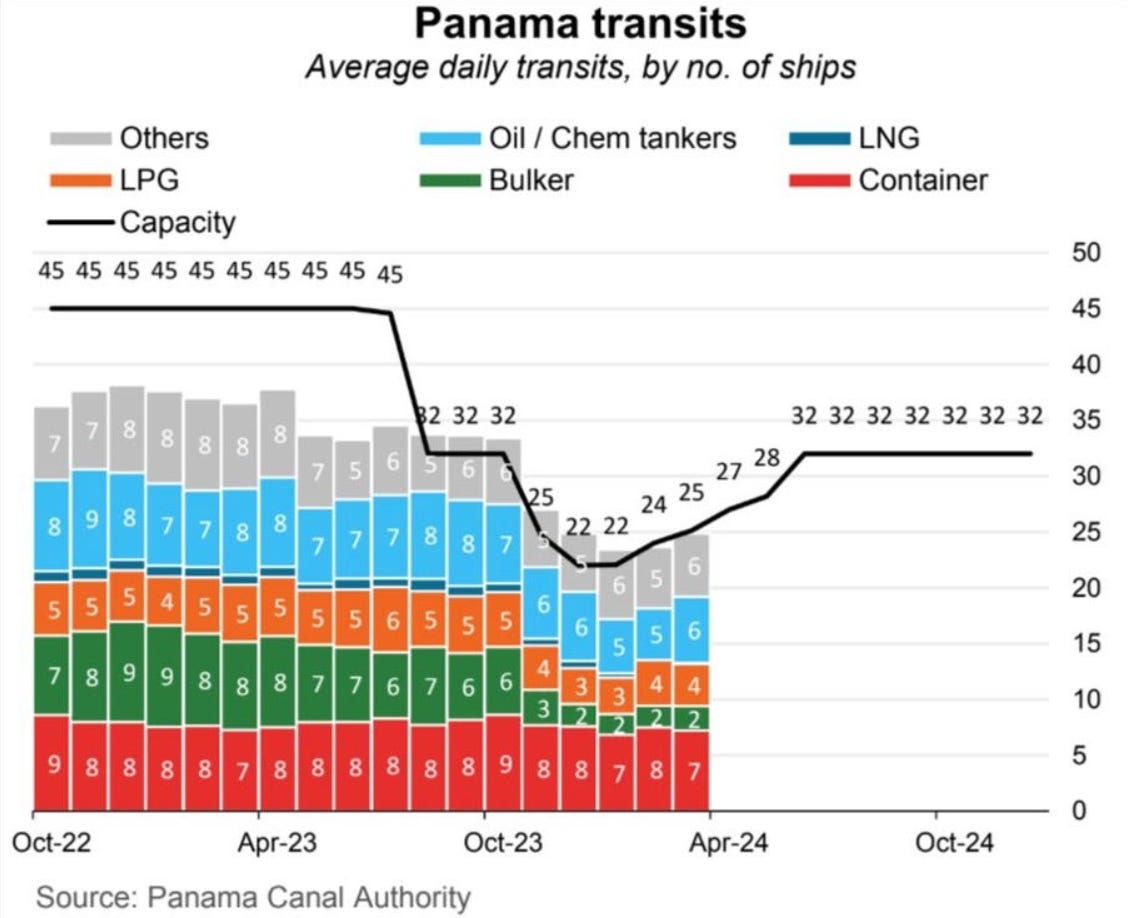

And here comes the role of the Panama Canal. The record drought in Lake Gatun has mostly affected gas carriers and medium and small tankers/bulkers.

Since the beginning of June, the water level has been gradually rising.

Traffic is expected to recover to 2022 levels in the next 12 months. However, this will not happen overnight. In other words, the Panama Canal will remain among the factors affecting LNG carriers in the coming months.

A final reminder: no matter how well-argued our analysis is, we will sooner rather than later find ourselves on the wrong side of the game without risk management.

Knowing when to strike is at least as important as knowing where to strike. This makes prudent risk management a foundation of my investing process.

The second one is to seek asymmetric ideas in obscure places. Simply, there is more Alpha to extract per market participant.

If you don’t want to miss such opportunities, look at TheOldEconomy paid subscriptions. If I got your attention, peek into the ”Test Drive” Section.

Yamal LNG has 15 Arctic icebreaking LNG tankers and several “normal” ice class ships built and operational. The prospects of Arctic 2 LNG project are uncertain due to sanctions and nobody knows when it may start production and need icebreaking LNG carriers for production offtake. It’s not “the world needs ice class LNG tankers - it’s Novatek who needs them”.