My doomsday shopping list

Bonds and equity ideas in shipping, energy, and more

The market continues to do what it does best: move in the direction that causes the most pain to the greatest number of market participants.

Furthermore, this week, we witnessed the power of viral information combined with trading algorithms. With just one tweet, this account provoked several trillion dollars to change hands in half an hour.

In addition, yields on US Treasuries have risen significantly despite the target rate of below 4.0%.

Yields are a strong predictor of equity behavior. I love the following quote from James Carville:

"I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a 400 baseball hitter. But now, I would like to come back to the bond market. You can intimidate everybody."

Treasury yields are telling that the turbulence is far from over, and the recent rip might be a correction in the bear trend.

Then, what should we do? Panic and sell everything? Definitely not. Another alternative, staying paralyzed in fear, is not viable, either. What we have to do is follow our execution plan. This is the only way to remain in the game.

As investors, our top priority is survival, and after that comes growth. In today’s article, I share my view on markets and some investing ideas. You will read about correlation, gravity, and fixed income. But before we move on to the interesting stuff, let’s look at the scenarios.

Reminder: treat today’s article as a map, nothing else, because the map is not the territory.

The scenarios

The first scenario is that the market continues downward, and the S&P500 reaches 4,000 - 4,500 in the next few weeks. The weight of this scenario remains at 35-45%.

In deep market crashes, bonds and preferred stocks are more attractive than common stocks. They have intrinsic value, and their issuers are obligated to distribute dividends/interest and eventually redeem the security. In summary, we generate income from dividends or interest plus capital gains.

For example, in March 2020, at the C19 crash, Tsakos Energy's preferred stock traded for $12.00 ($25.00 is par value) and a yield of 9.00% (relative to par). As a result of the decline, these shares carried a 19% annualized yield, plus over 100% potential capital gain upon sale. The key word here is gravity. More on that later. We get all the perks at a low risk of total loss of principal.

The second scenario is more boring—the market enters a volatile range. The weight of this option is also unchanged, 35%-40%. In this case, I would use any downturn to add to current positions in critical minerals and litigation cases. Meanwhile, I will look for lucrative fixed-income plays.

I'm not entirely ruling out a surprise bulls comeback, either. Recent days remind us of two things: to expect the unexpected and the power of a changing narrative. In this view, a positive catalyst event like a trade agreement between China and the US could put the ball back in the bulls' court. Nevertheless, this is the scenario with the lowest probability. I assign 10% to 20% chances of happening.

To emphasize, these values are not absolute, much less precise. They show the relative weight of each scenario.

The prevalence of no-bull market scenarios reminds me of the importance of two often overlooked characteristics of any investing idea: low correlation and a center of gravity.

Correlation and gravity

Prolonged bear markets are an elevator to hell. However, there are exceptions. Such are unpopular and obscure industries and companies. A prime example is litigation cases.

These types of positions are not dependent on the performance of the indices. They do what they do without getting excited about the markets. Of course, it's a double-edged sword; these same ideas during a bull market also do what they know. If we don't have a catalyst event on the horizon, let's say a court decision, we can still incur losses even though the markets are performing well. In simple terms, the impact of the catalyst event outweighs that of the broader indices for such ideas.

TheOldEconomy portfolio has two litigation cases. Yet they are not the only even driven picks. Add critical minerals and distressed debt to the list.

Fixed income and litigation cases share another advantage. They possess a center of gravity. What does it mean?

Think about the bond’s nominal value as the center of gravity. It does not matter what the bond price is before the maturity date. To clarify, this is true for bond investors who hold to maturity or redemption. On that day, the issuer must repay the bond at its par value. As maturity approaches, the bond price will move closer to its par value, i.e., the law of gravity in action.

Litigation cases have a predefined size. The claim is the center of gravity here. Depending on the progress of the case, the claimant's share price will fluctuate accordingly.

If the company's market capitalization is $50 million and the claim is valued at $500 million, the center of gravity is $500 million. So, if the court decision favors our company, its equity value will increase, chasing that $500 million.

Low-correlated ideas with a center of gravity are highly lucrative, particularly during times of increasing uncertainty. Thus, they are an integral part of my shopping list.

A doomsday shopping list

Here is the doomsday list. In such a scenario, the assets that offer the best payoffs and probabilities are fixed-income instruments. The list includes preferred stocks, bonds, and a few common equity plays. And here it is:

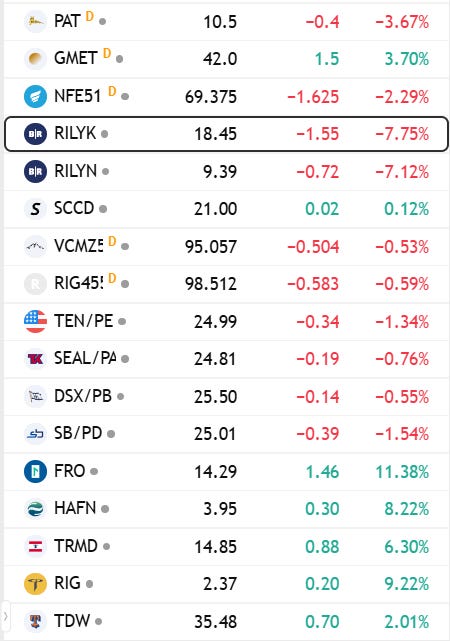

Shipping and energy dominate the list. All shipping names listed above have fortress balance sheets, which significantly reduces credit risk and affirms dividend safety for preferred equity investors.

New Fortress (NFE) and B. Riley (RILY) are another story. Both enterprises have apparent issues and fall into the category of distressed debt. Yet, credit risk is not as high as the market implies. Most importantly, the Yield to Maturity is adequate to compensate for the risks taken.

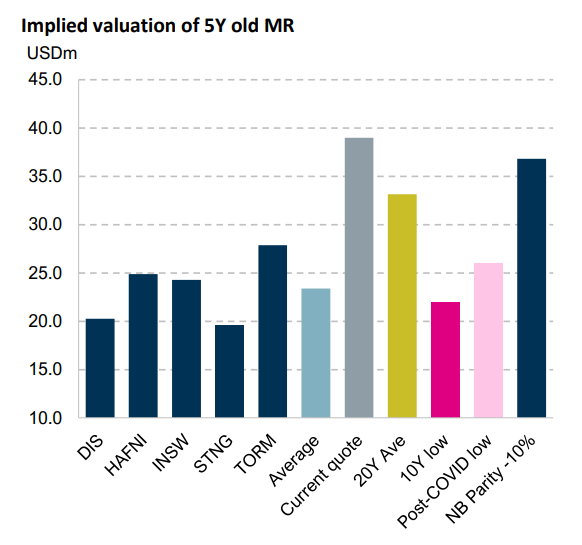

The next theme is shipping. Product tankers are getting really interesting at those share prices. Look at the image below:

The reference is the value of MR product tankers. Product tanker owners trade at massive discounts to PNAV. Basically, we can buy quality floating steel for less than 60 cents on a dollar.

Two junior miners top the list. Panthera Resources (PAT) is a classic litigation play. Shout out to

for his exceptional article covering cases as an emerging asset class. Guardian Metal Resources (GMET) is a bet on the US mining revival. It owns a large tungsten project in the US.The list includes Tidewater (TDW) and Transocean (RIG). Both companies trade well below their 12-month moving average. For now, it is too early to consider equity positions. On the other hand, RIG offers attractive bonds. Depending on how extensive the decline is, RIG credit may get a priority boarding pass for my portfolio.

This was my doomsday shopping list. Do not treat it as a recommendation. Use it as an idea generator.

Final Thoughts

Bear markets are fun. Thanks to the crash, epic memes were born. Look at that meme.

Once I see it, I can not unsee it. Now, back on the serious stuff.

To recap. First, do not panic. Focus on financial and mental capital preservation and then on growth. Survival is the prerequisite for growth, not the other way around.

Then, find the right instruments to express your view. Low correlation/high gravity assets are invaluable alpha generators in turbulent times. Shipping and energy are good places to start your research.

PS: TheOldEconomy is changing once again. News is coming soon. Stay tuned.

On the markets, we are wrong until proven otherwise. So, take the above thoughts with a grain of salt.

Everything described in this report has been created for educational purposes only. It does not constitute advice, recommendation, or counsel for investing in securities.

The opinions expressed in such publications are those of the author and are subject to change without notice. You are advised to do your own research and discuss your investments with financial advisers to understand whether any investment suits your needs and goals.