Super-Cycle Setup: Why PGMs Could Deliver Triple-Digit Gains

Deep Dive in PGMs for the Search Engines to Find It

Do you want to know which commodity is poised for a new super-cycle? It is a metal so critical to the United States industry that the Trump administration excluded it from tariffs. China imported record volumes last year, and the metal is indispensable to the green transition. At the same time, chronic supply problems keep the market in deficit, demand remains firm, and analysts continue to predict surpluses that never materialise. With prices now below breakeven for most producers, many mines are closing, all but guaranteeing that any forecast surplus will be pushed even farther into the future. A supply crunch could therefore deliver multibagger returns for the small handful of listed miners while limiting downside risk.

The thesis is straightforward: supply keeps shrinking, demand is steady, and spot prices sit below the cost of production for most companies, several of which have already announced output cuts. Inventories are falling rapidly, yet prices remain muted while informed investors wait for the inevitable supply crunch.

The metals in question are the platinum-group metals—platinum, palladium, and rhodium. Although they serve many industrial uses, the largest single end-market is catalytic converters. That dependence has fueled bearish arguments because electric vehicles do not require catalytic converters, and the global automotive sector has been weak. Even after a strong start to the year—platinum is up 43 percent year to date, rhodium 18.5 percent, and palladium 16.8 percent—prices remain well below recent highs, especially for palladium and platinum, which sold off sharply after their post-pandemic rally.

You might think the opportunity has already passed, but current prices are still far from historic norms.

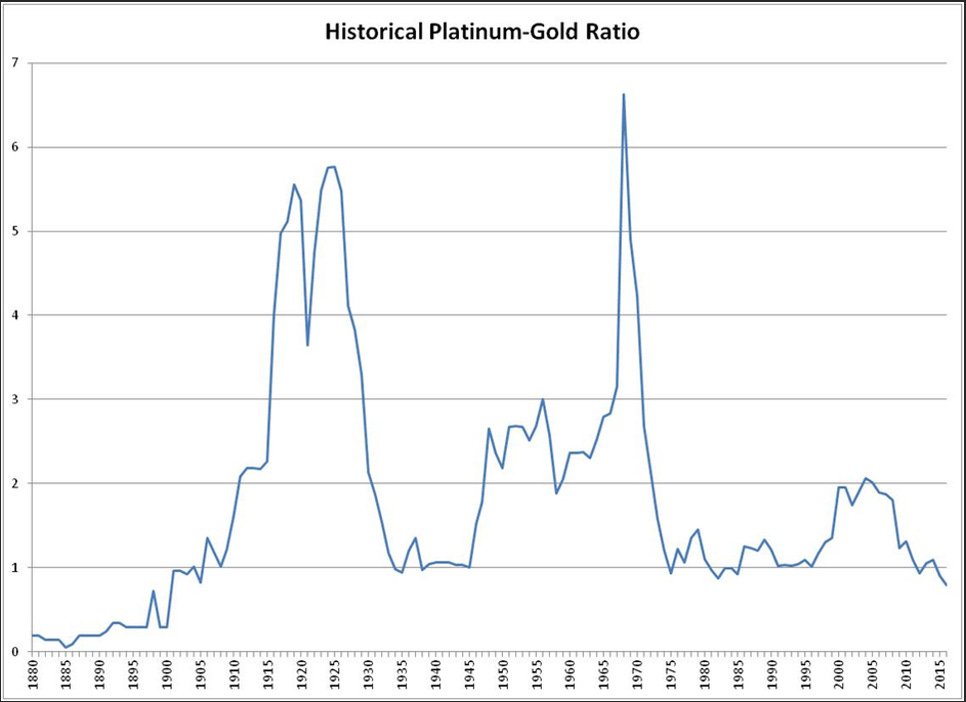

First, consider the platinum-to-gold ratio.

We are at levels never seen before. For more context, look at the longer-term chart.

Today, the ratio stands at 0.37, even though platinum is roughly thirty times rarer than gold.

In this article we will explore every aspect of the PGM thesis in detail: supply-and-demand dynamics, company analysis, small cap opportunities, options, and a step-by-step execution plan to take advantage of the next PGM supercycle.

We will not discuss the potential boost to PGM demand from hydrogen applications; the article is already lengthy, and that market is unlikely to scale before 2030. If it does materialize, it could add demand equivalent to the entire current automotive sector, driving prices even higher.

Index:

1. Platinum Market Overview

2. Palladium Market Overview

3. Rhodium Market Overview

4. Different scenarios and probabilities

5. Analysis of the major miners

6. Execution plan

7. Conclusion

Before we begin, I would like to acknowledge my collaborator, Hugo Navarro of Undervalued and undercovered. Hugo focuses on overlooked small-cap opportunities and has achieved a 56.2 percent IRR across his published ideas. His Substack is currently available at a 50 percent discount on the annual plan for new subscribers; if you find today’s analysis helpful, you may wish to explore his broader research.

1. Platinum Market Overview

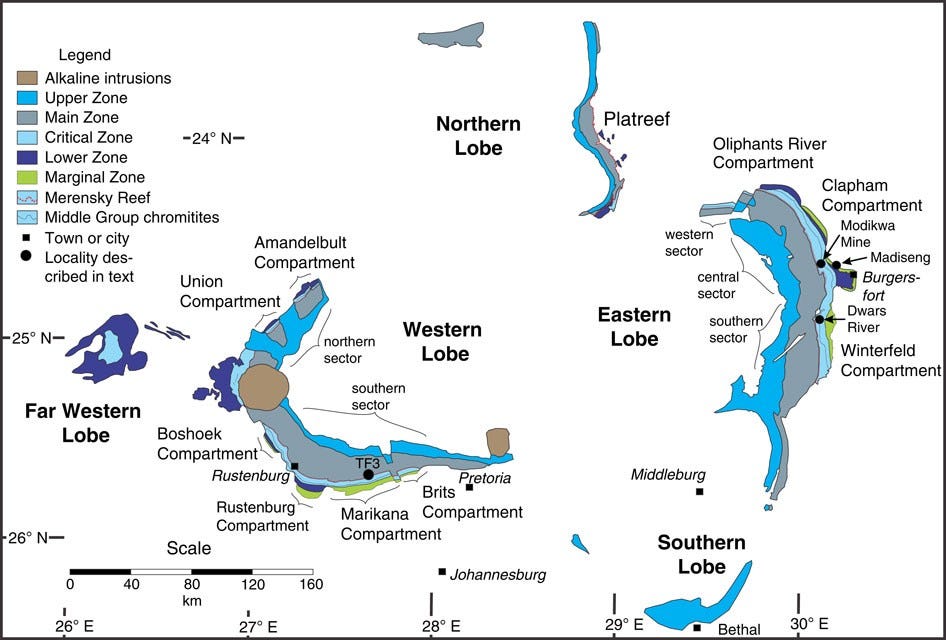

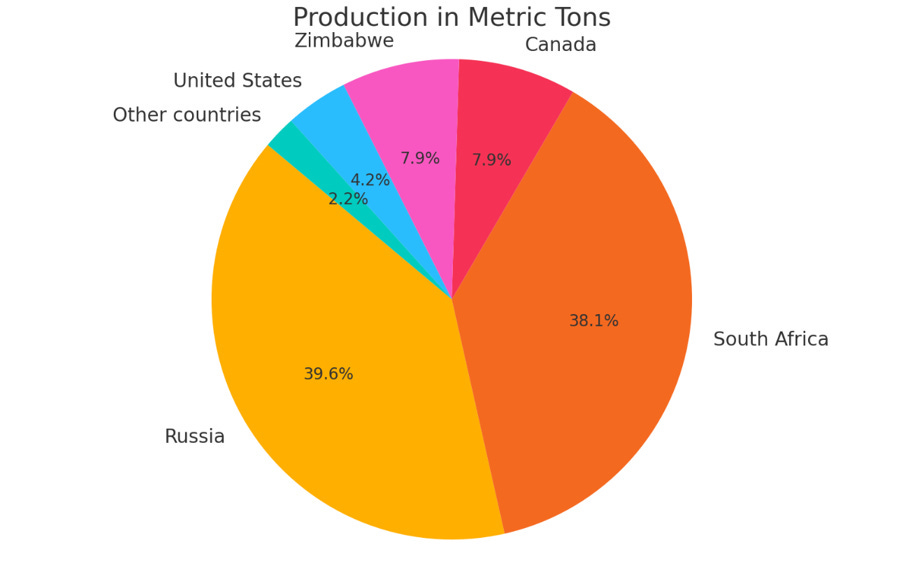

South Africa mines about 75% of the world's platinum, 80% of the world's rhodium, and 45% of the world's palladium. This is all concentrated in the Bushveld Ingenious Complex (BIC) in the Gauteng/Transvaal Provinces.

The map below shows BIC’s limbs (or lobes) and deposits (image via SFA-Oxford):

The largest PGM mines, such as Impala, Marikana, and Rustenburg, are located in BIC, and more particularly in the Western Lobe. To make things even more exciting, more than 70% of South African platinum comes from those mines. Simply, about 50% of the world's platinum is mined in a territory with about 12,500 square kilometers. Surface area comparable to Lebanon or Montenegro.

Considering that, platinum and rhodium are probably two metals with the most concentrated production. A few mines in a tiny plot of land deliver more than half of the global production. It sounds like a recipe for explosive bull runs. The missing ingredient is a catalyst, which will further constrain the supply.

That said, South Africa’s platinum sector faced significant headwinds in the first half of 2025. In February 2025, platinum output fell by nearly 10% year-on-year due to severe rainfall and operational constraints. The 2025 platinum production is progressively declining compared to 2023 and 2024. (Chart via WPIC 1Q25 report)

Major producers have signaled caution regarding production increases, with no significant new mine openings and a reluctance to expand output in the current environment. While no high-profile mine closures were reported in early 2025, companies are actively reviewing their portfolios, with underperforming shafts and higher-cost operations at risk of closure if market conditions do not improve.

Low platinum prices prompted the miners to adapt and reduce production, thereby maintaining their operating margins. AISC remained under pressure, although some relief was noted due to rising rand prices for platinum, palladium, and rhodium. Industry reports indicate that the lowest-cost platinum operations, such as the Platreef project, project cash costs as low as $351 per ounce of 3E+Au, net of by-products and AISC figures between $1,410 and $1,901 per ounce in late 2024 and early 2025.

To some extent, decreased production was offset by robust recycling figures in 1Q25. Global recycling supply increased by 2% year-on-year to 372 koz. Improvements in autocatalyst recycling primarily drove this growth, as higher new vehicle sales in the US and Europe boosted the availability of end-of-life vehicles. At the same time, China’s government incentives encouraged more scrapping of older cars. However, jewellery recycling contracted by 11% over the same period, reflecting subdued consumer trade-ins.

Overall, the recycling sector’s performance was uneven: while autocatalyst scrap recovery stabilized from a low base in Western markets, jewellery recycling lagged. In summary, the recycled platinum supply remains below pre-pandemic levels, and the sector continues to face ongoing challenges from constrained scrap availability and regional disparities in recycling infrastructure.

The platinum market is a notable example of a structural shortage driven by supply issues. Yet the good news for platinum investors does not end here. Platinum demand is projected to surge in the coming years, widening the already acute deficit.

In 1Q25, global platinum demand increased by 10% YoY, reaching 2,274 koz, driven primarily by a sharp increase in investment demand as market participants responded to tariff-related uncertainties in the United States. The anticipation of potential tariffs on platinum imports led to significant flows of metal into the US, with 361 koz entering CME warehouses, temporarily boosting investment demand to record levels.

Automotive platinum demand, traditionally the largest segment, declined by 4% to 753 koz as production of vehicles slowed amid uncertainty over raw material costs and trade policies. Industrial demand also contracted, falling by 22% year-over-year to 527 koz, primarily due to a dramatic 81% decline in glass sector demand, as capacity additions in China slowed and plant closures occurred in Japan. Conversely, platinum jewellery demand rebounded, rising 9% to 533 koz, with notable growth in Europe and China, where high gold prices prompted a switch to platinum. The net effect was a market deficit of 816 koz, the largest quarterly shortfall in six years.

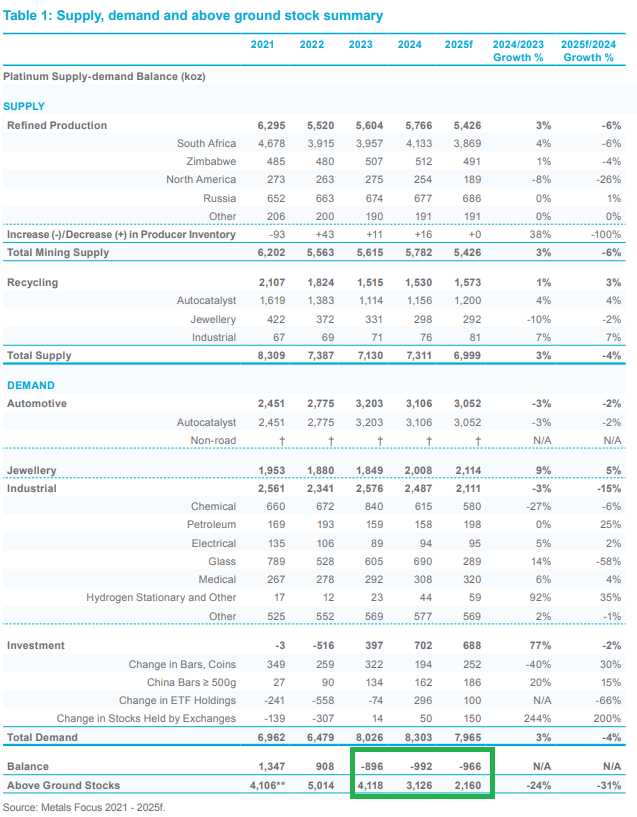

In conclusion, one table tells it all (via WPIC 1Q25 report), we need to know about the platinum market:

The platinum market records its third consecutive year in acute deficit. The shortage accounts for approximately 13% of the total supply. It is only a matter of time before we see higher platinum prices for longer.

2. Palladium Market Overview

Palladium, one of the platinum-group metals (PGMs), is a crucial component in vehicle catalytic converters. These converters reduce harmful emissions, enabling the automotive industry to meet stringent environmental standards. In recent years, however, the palladium market has experienced a significant decline, largely driven by expectations of future surpluses. Since its peak in 2022, palladium prices have plummeted as investors anticipate an oversupplied market.

Palladium is the PGM most exposed to geopolitical risk, with 39.6% of its global supply originating in Russia. Consequently, any Western sanctions on Russia—or a Russian embargo on palladium—could propel prices to new all-time highs.

Year-to-date, palladium prices have severely underperformed those of platinum, mainly because the market continues to expect sizeable near-term surpluses—a scenario not currently forecast for platinum.

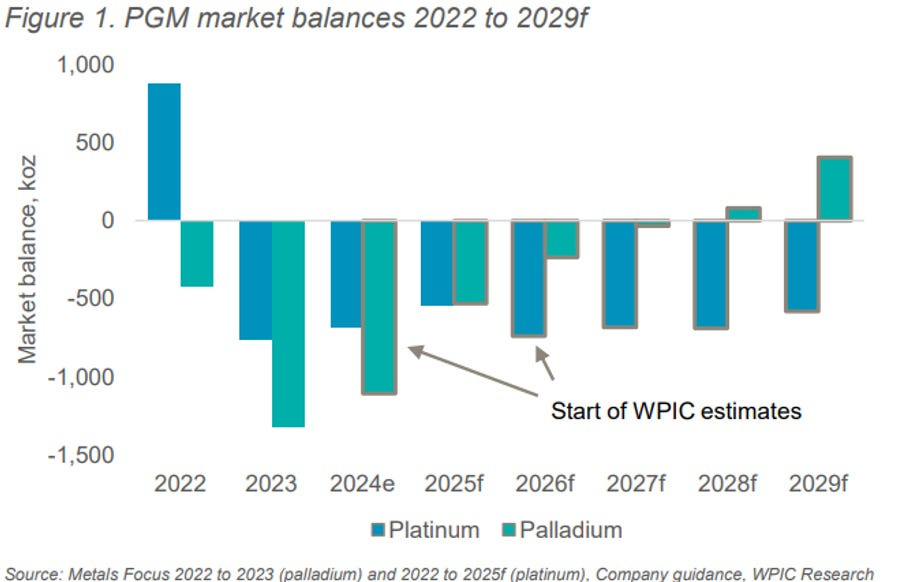

Coming off the strong deficits recorded in 2024—and with shortfalls now expected to persist through 2027—palladium’s fundamentals remain firmer than many analysts predicted. A few years ago, consensus forecasts pointed to a balanced market as early as 2025; clearly, that timeline has slipped. In fact, one new catalyst could push deficits out to 2029: the planned closure of Impala’s Lac des Iles mine, which produces roughly 250 thousand ounces of palladium per year, or about 4 % of global primary supply. Removing this material could keep the market in deficit through 2028, and quite possibly 2029.

Modern catalytic converters can substitute platinum for palladium on a 1:1 basis—one ounce of platinum can replace one ounce of palladium. Historically, the substitution ratio was closer to 2:1, favouring cheaper palladium in place of higher-priced platinum. When palladium prices soared, the economics flipped, and manufacturers began substituting platinum for palladium. Today, with palladium once again the more affordable metal, that substitution incentive is fading. Over the long run, platinum and palladium prices should converge, and periodic substitution cycles between the two metals are likely to continue.

Platinum-for-palladium substitution was estimated at 620 koz in 2023 and is forecast to rise to 700 koz in 2024. Current projections suggest the flow will peak at approximately 877 koz in 2025. While these shifts temporarily suppress palladium demand, any pause—or reversal—in the trend would extend the metal’s supply deficit.

Palladium, therefore, retains significant upside potential. The market is highly sensitive to supply disruptions—such as the Lac des Iles shutdown—and to shifts in substitution economics. With short interest still elevated, any positive catalyst could trigger a sharp price rally as short sellers scramble to cover their positions.

Short positions in palladium

3. Rhodium Market Overview

South Africa dominates global rhodium production, accounting for approximately 80-83% of the world's supply. Like platinum, most of the rhodium production comes from a few mines located in the Western Limb of BIC.

The other two players in the field are Russia and Zimbabwe. Global Rhodium Production by Country is shown below.

")

For reference, the US and Canada account for 1.8% of global rhodium mining.

Rhodium supply comes from two sources: mining operations and recycling. Primary mining accounts for approximately 80% of the global rhodium supply, while recycling contributes the remaining 20%. Recycling has become increasingly important in the rhodium market, with the recycling volume growing at approximately 8% annually. Nevertheless, it is far from sufficient to compensate for the risk that derives from the production concentration.

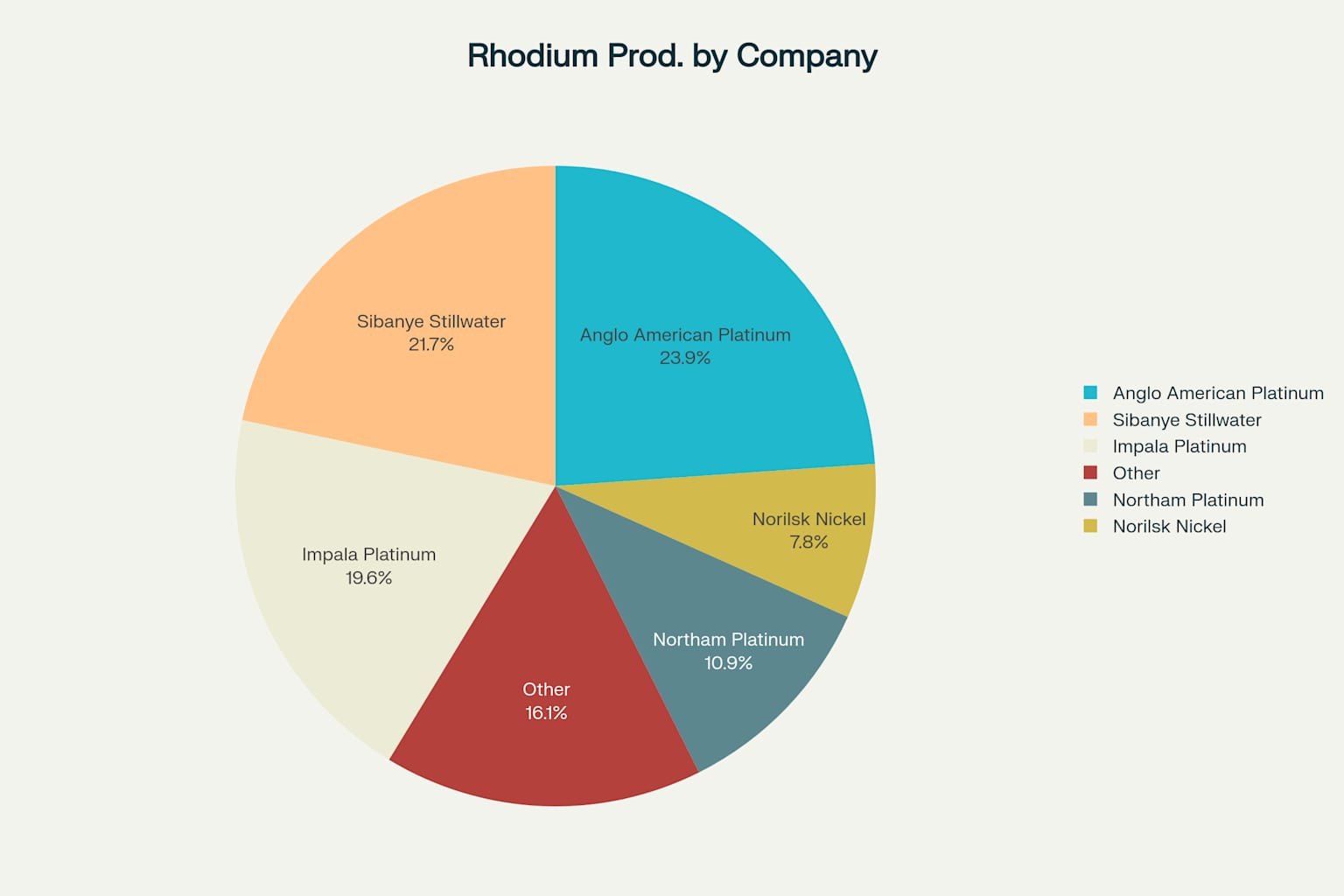

The usual suspects involved in rhodium mining are the South African PGM miners. The only exception is Nornickel.

Sibanye Stillwater and Anglo American Platinum are responsible for nearly 50% of the world's rhodium output.

As you can see, the same story goes here: a few mines with operations in BIC dominate rhodium production. A short-lived perturbation in mining operations can cause an epic spike in rhodium price.

Given the current global state of affairs, I would not be surprised to see some of the precious metals, especially rhodium, being used as a geoeconomic weapon. We have case studies for commodity weaponization: REE, tungsten, and antimony, to name a few. The rhodium market already operates in a regime of deficit. Therefore, a potential export or import restriction would likely cause a substantial surge in its price.

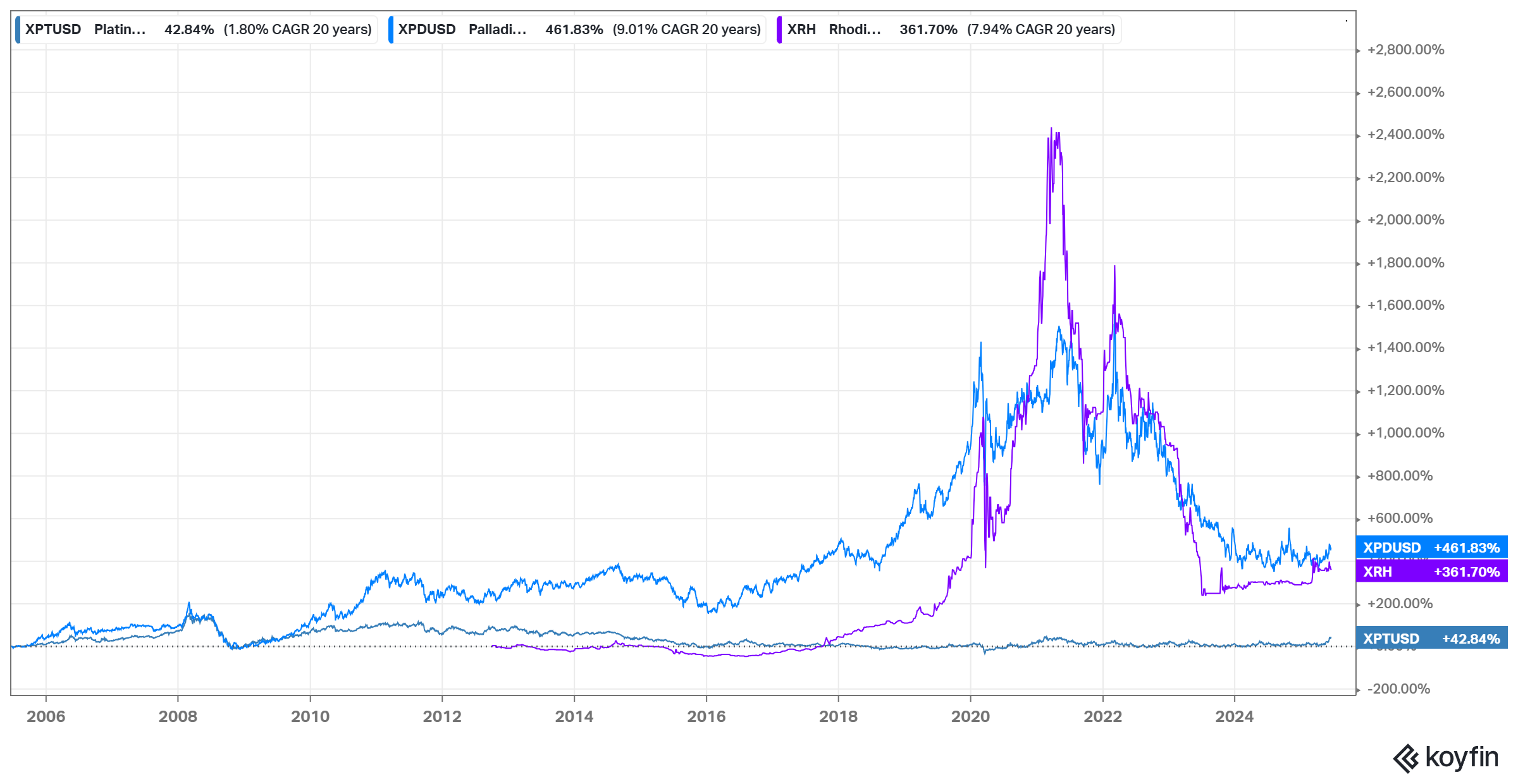

During 1H25, rhodium price surged to a 20-month high, approaching $6,000 per troy ounce by May 2025. Despite the recent bull run, rhodium, like platinum and palladium, is far from its peak levels. For reference, the chart below.

Price surge reflects supply constraints and robust demand. South African production contracted by 4.5% in 1Q25 compared to the previous quarter. Heavy rainfall and widespread flooding severely impacted operations, particularly at the Tumela mine in the Amandelbult complex, contributing significantly to production shortfalls.

Rhodium recycling provided some offset to primary supply issues, with the recycling market growing at an annual rate of approximately 8%. Automotive catalyst recycling remained the dominant source of secondary supply, benefiting from increased vehicle scrapping rates in some regions. However, the overall contribution from recycled sources was insufficient to balance the market, as primary production shortfalls outweighed the gains from recycling.

Automotive demand remained the primary driver for rhodium consumption in 1H25. The metal's critical role in catalytic converters, which reduce nitrogen oxide emissions, continued to support demand. Industrial applications, particularly in the chemical and electronics sectors, provided additional demand support, albeit at lower volumes than those in the automotive industry.

Besides shrinking supply and robust demand, according to Metals Focus, above-ground stocks are declining rapidly. The reduction is 23% to approximately 349,000 troy ounces—the lowest level in four decades and equivalent to just four months of global demand.

Constrained supply, limited demand, and record-low inventories sound like a recipe for asymmetric trade. In March 2021, the rhodium price reached $29,800/oz. Today, the metal is trading at $5,425/oz. These figures imply significant upside potential. Niche metals, such as PGMs, tend to overshoot in both directions. Considering the fundamentals, the stars are aligned for an impulsive bull move. Depending on the catalyst, the rhodium price can reach a new ATH. The same is true for platinum and palladium.

4. PGM Market Scenarios

PGMs are in the late pessimism stage, approaching early skepticism. For reference, the image below:

At this stage, the upside potential is huge, while the downside risk is capped. Only specialist funds invest in the best (in their view) and not always the most liquid companies. It is still early for institutional investors and the mass retail to enter. In other words, the euphoria when the hype peaks and any company with “The New Hot Thing Plc” in its name is bought, no matter its merits, is far away.

So far, so good, knowing our starting point in the cycle provides a base to create our scenario grid. I have three credible scenarios, each with distinct probabilities, for the next 24-36 months:

Bull market: >50% probability; challenging ATH for all PGMs; 24 to 36 months time horizon

Range: 20% to 30% probability; zero upside potential; 24 to 36 months time horizon

Bear market: 10% to 20% probability; >50% loss of the principal; 24 to 36 months time horizon

One thing is common for all scenarios: extreme and unforgiving volatility. Even in the best-case scenario, a roaring bull market, volatility will hit the unprepared investors hard.

Two reminders:

Regardless of the relatively low probability of total loss of the principal, it never reaches zero. Therefore, beware of the importance of position sizing.

Assigned probabilities are not precise. They serve to show the relative credibility of each scenario.

Frankly, the worst case is not a bear market, but a blood-draining range. This is the most challenging regime to trade because of the frequent whipsaws in both directions. The solution in that case is options, but under some consideration. More details on how to bet on PGMs are given in a separate section.

Now, let’s move back to the scenario discussion.

One more reminder about the nature of PGM markets is the pronounced cyclicality. Ruinous bear markets always follow bull markets. So, even if we start with a bull run, we must never forget that as soon as the deficit turns into a glut, the PGM price will crash.

This paragraph emphasizes one more thing: the scenarios should not be considered in isolation. Over the next 24 to 36 months, we can experience all three. Let’s say the PGM price shoots up to a new ATH, then abruptly plunges to the present levels, and eventually sticks to a volatile range. This is only one potential timeline.

That said, despite the favorable probabilities, do not assume a potential PGM bull run will be smooth or that the volatility will not count. Embrace the turbulence.

5. Major PGM Miners

First, we will start with the so-called “big three” — the largest PGM miners in the world: Impala Platinum, Anglo American Platinum (often called Amplats), and Sibanye-Stillwater. We will take a close look at these three to assess their individual risk-reward profiles.

Impala Platinum

Impala Platinum is a major player in the PGM market, with a market capitalisation of around US $7 billion and significant exposure to palladium, platinum, and rhodium. The company operates mines in South Africa, Zimbabwe, and Canada, together supplying roughly 20 % of global PGM output. Its attributable mineral resources total about 316.5 million ounces. One concern, however, is the limited remaining life of several core shafts, which may constrain future production growth.

For FY 2024, the company reported heavy losses. Although its all-in sustaining costs are competitive for a producer of this size, Impala fails to generate free cash flow when platinum or palladium prices fall below roughly US $1 100–1 200 / oz.

The company currently produces 3.38 million ounces of PGMs per year and is guiding for 3.5 – 3.7 million ounces in FY 2025. Management expects output to settle at 3.2 – 3.4 million ounces in the mid-term, chiefly because several shafts are nearing the end of their lives and because of the planned closure of the Impala Canada mine.

The shutdown of Impala Canada could prove significant: the operation contributes about 7 % of group output and is 90 % palladium. As noted earlier, any reduction in palladium supply has the potential to push prices higher.

Over the next decade, mines responsible for approximately 1.745 million ounces of annual production are expected to reach end-of-life, which could ultimately cut group output by more than half.

Impala is still raising production at its newer assets, but costs have risen—reflecting the inflationary pressures faced by most miners. Although cost inflation may moderate, it remains a risk.

Unit costs are therefore projected to stay at, or slightly above, current levels in the mid-term, driven by inflation and the higher operating expenses typical of late-life mines.

CAPEX and Production

Impala’s capital expenditures (CAPEX) have fallen sharply, especially those earmarked for expansion. (The reported –114 % change in expansion CAPEX is likely a data error.) Most of the company’s production growth now stems from a ten-fold increase at Impala Bafokeng, which is offsetting declines at other operations. Even so, revenue has dropped alongside lower PGM prices. Although Impala’s cash balance is at a multi-year low, the group remains cash-positive after netting out debt.

Looking ahead, management guides to refined output of 3.45–3.65 million ounces in FY 2025—a 2–8 % year-on-year increase—while unit costs are expected to rise 0–5 %. CAPEX is slated to fall from about US $800 million this year to US $440–495 million next year, but most of that spending will merely sustain existing production and meet regulatory requirements. With only one genuine growth project in the pipeline, the company may struggle to offset losses at mines nearing end-of-life.

Costs and Profitability

Impala (primary mine): Cash costs are about $1,161 per 6E ounce. Due to large depreciation and amortization (D&A) tied to previous CAPEX, this mine is barely profitable at current PGM prices.

Zimplats (second-largest mine): Cash costs average $829 per ounce, which is relatively low. However, high CAPEX needs (this mine required almost required double the total capex of the rest of mining operations even though it does not represent the same production) mean the operation is not yet free-cash-flow positive.

Other operations: Cash costs hover around $1,000–$1,100 per ounce, and extensive CAPEX has kept them cash-flow negative. Production growth this year has come only from the Impala Bafokeng acquisition; other mines have struggled to maintain output despite sizable investments.

The Two Rivers mine is currently receiving most of the company’s growth CAPEX. Although it has low cash costs for now, it’s set to enter care and maintenance in Q1 of this year, meaning further development depends on higher PGM prices.

Metal Exposure

Impala has notably high exposure to palladium and rhodium—about 20–30% of total production comes from each of these metals, which is much higher than many competitors.

Valuation

At a market capitalisation of roughly US $7 billion, Impala may look inexpensive—particularly if PGM prices rebound to their 2021–2022 levels. Under that scenario, the company could generate US $1.5–2.5 billion in free cash flow, given that palladium and rhodium prices have fallen about 80 % from their peaks. However, the high CAPEX needed merely to sustain production, coupled with sizeable goodwill impairments, raises doubts about Impala’s ability to offset declining output at its core mines. Should PGM prices continue to weaken, the group might have to take on additional debt or shut down further operations.

If you believe PGM prices are set for a sharp rebound, Impala offers intriguing optionality. The company holds around 500 000 ounces of PGMs that could be sold into a rising market, and a price upturn would push most of its mines back above breakeven. Impala’s sizeable exposure to heavily shorted palladium and rhodium also introduces the possibility of a short squeeze—potentially lifting free cash flow above US $2 billion and driving the share price to US $10–15, or roughly a 2× return within a few years.

Overall, the risk-reward profile appears less compelling to me. Management has previously diluted shareholders while still paying dividends—an unfavourable strategy when the stock trades on a low EBITDA multiple. In my view, there are more attractive ways to play the current PGM cycle, although Impala remains one of the miners most leveraged to rhodium and palladium prices.

Anglo American Platinum now Valterra Platinum

Anglo American Platinum—rebranded as Valterra Platinum following its recent demerger—remains the world’s largest PGM producer by market share. The share price has fallen sharply, from more than US $150 in early 2022 to the low-40s today, logging only a 28 % year-to-date gain despite the platinum rally. The key question is whether this pull-back offers an attractive entry point or whether better risk-adjusted opportunities exist elsewhere in the sector.

Anglo American completed the spin-off of 51 % of Anglo American Platinum on 1 June, and Valterra’s shares began trading on the London Stock Exchange the same day. The separation ends a lengthy divestment process that had created uncertainty and consistent selling pressure. Although Anglo American still owns 19.9% of Valterra, any residual overhang should be brief: once the 90-day lock-up expires, some additional sales may occur, but thereafter the company can be judged squarely against its PGM peers.

Valterra’s chief strength lies in its low unit-cost base. All-in sustaining costs averaged US $986 / oz in FY 2024, and management is targeting costs below US $1 050 / oz. Indeed, Valterra was the only pure-play PGM miner to post a profit in FY 2024, underscoring its operational efficiency. The company guides to 3.5 Moz of PGM production in 2024, followed by a 10 % decline in 2025–2026 to roughly 3.2 Moz across managed and consolidated operations. Mine-owned output is expected to hold steady at 2.1–2.3 Moz per year.

The group closed FY 2024 at the upper end of guidance, delivering strong operational results in spite of weak prices.

By metal, about 46 % of Valterra’s production is platinum and 33 % is palladium, with the balance in other PGMs plus a small amount of gold. This blend offers meaningful palladium leverage while maintaining a solid platinum base.

Valterra currently looks inexpensive, though it has historically traded at a modest premium to peers such as Impala. The post-demerger dislocation—and the stock’s muted participation in the recent PGM rally—make today’s valuation compelling, especially given Valterra’s industry-leading margins. A rerating toward its traditional premium seems plausible once the market views the company independently of Anglo American.

With US $888 million of net cash and projected 2024 operating cash flow of US $300–400 million—even while many rivals are loss-making—Valterra is well placed to navigate the current down-cycle. At the top of the cycle, free cash flow has historically hovered between US $3–5 billion. Against a US $10 billion market capitalisation, that upside suggests Valterra may offer the most attractive risk-reward profile among the “big three” PGM miners.

Silbanye Stillwater

Sibanye Stillwater, often highlighted on Substack, trades on the NYSE and is therefore more accessible to U.S. investors and far more liquid than its miner peers, which mean that most speculation regarding PGM prices is done through options on Silbanye making it far more volatile delivering a 2x return YTD thanks to the increase in PGM prices and their gold operations. Over the past decade, the company has outperformed many of its peers. However, it’s also quite complex to value due to its diverse operations:

Gold Mining: Producing around half a million ounces, which at current prices and even with their high AISC amounts to 500 million in EBITDA just from gold.

PGM Mining: Active in both South Africa and the U.S., with a significant portion of PGM production coming from recycling.

Lithium Assets: Owns what is claimed to be the largest lithium mine in Europe, plus a battery recycling plant.

Byproducts and Other Minerals:

Chrome byproduct from PGM mining.

Around 60 million pounds of uranium in tailings; recently entered a joint venture for the Beisa uranium project. Sibanye will receive a cash payment, 40% equity in Neo Energy, and royalties of up to $5/lb of uranium—potentially significant if prices rise.

DRD Gold Stake: Holds 50% of DRD Gold, which has a market cap of $1.2 billion, valuing Sibanye’s stake at around $600 million.

Streaming Deal: Raised $500 million from Franco-Nevada by pre-selling gold and PGMs from South African operations, while this decreases a little bit of the upside from the PGM sector, the company still maintains a good upside potential and this deal was smart at the time.

At current PGM prices, even after the recent rally, Sibanye’s PGM operations remain under pressure. In the United States, production costs are about 1,400 dollars per ounce; South African costs are somewhat lower but still well above those of competitors such as Impala and Anglo American. To contain losses, the company has placed the Stillwater West mine on care and maintenance and has reduced its workforce until prices recover.

Although Sibanye carries some debt, it should have little difficulty servicing it: the adjusted leverage ratio for 2024 is below 1 and is likely to decline further if PGM prices rise. The group’s complexity is noteworthy. Its gold-mining division alone could justify much of its market capitalisation, while the uranium joint venture, the DRD stake, lithium and battery-recycling businesses, and PGM assets provide multiple avenues for growth. The market’s chief concern is the weak PGM segment, which had weighed on the share price until the recent increase in platinum.

In the short term, Sibanye could be hit hardest if PGM prices fall again and a sustained bull market fails to materialise. Over the longer term, however, the company’s diversified asset base may offer a more attractive story, creating an asymmetric opportunity for investors willing to accept the risk. For a detailed analysis of Sibanye’s structure and prospects, please refer to the linked deep-dive report.

Small producers, golden opportunities

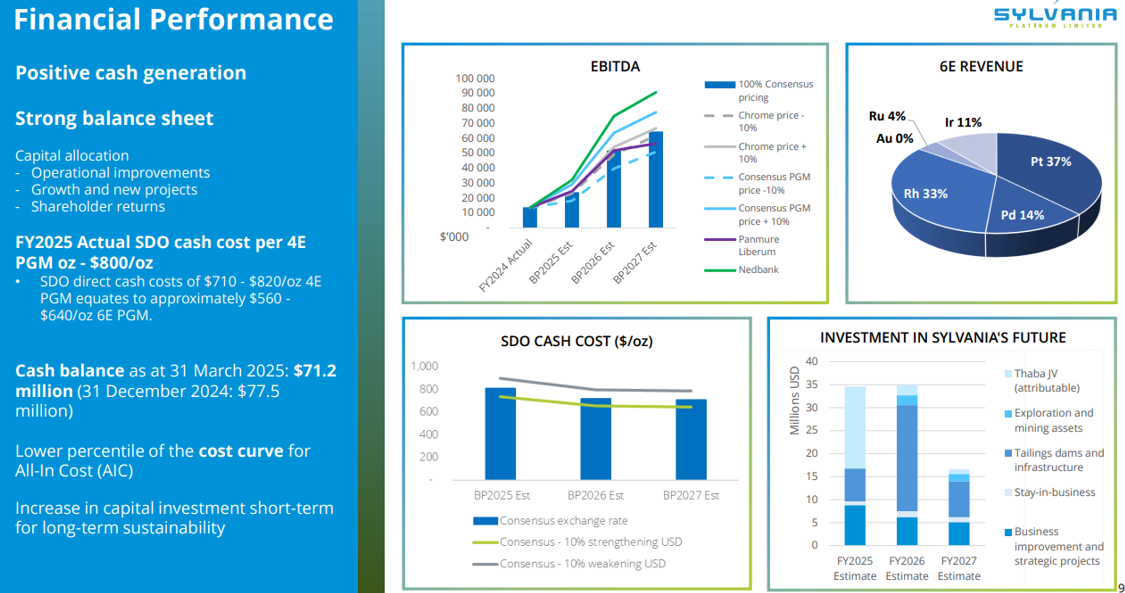

Sylvania Platinum, with a market capitalisation of 182 million pounds, stands out for its low-cost tailings-reprocessing model, which keeps the business profitable even when PGM prices soften. The balance sheet is robust: the company holds more than 60 million pounds in cash and carries no debt, giving it the flexibility to pay dividends, repurchase shares, and continue reinvesting.

Management has pledged to return at least 40 per cent of adjusted free cash flow to shareholders. Any future upswing in PGM prices would likely feed straight into EBITDA and, by extension, the share price. Growth programmes are structured to lift output as prices rise, yet the operating model remains firmly at the low end of the cost curve. Consistent with this strategy, Sylvania is already conducting buy-backs and distributing an attractive dividend.

In the most recent investor presentation, management projected EBITDA of more than 60 million dollars based on consensus price assumptions. Since then, spot prices have moved well above those forecasts. If the market strengthens a little further, EBITDA of 80–90 million dollars in 2027 looks achievable—implying a remarkably low valuation multiple even before considering a more bullish PGM scenario.

With cash equal to more than one-third of its current market capitalisation, Sylvania can remain profitable even if prices stall. Its SDO costs already absorb some growth expenditure that AISC metrics exclude, reinforcing the company’s margin resilience. For a deeper look at this thesis, see my detailed write-up; it uses deliberately conservative assumptions that can be updated easily for the recent price moves.

Tharisa is the lowest-cost PGM producer I have identified, yet it trades at what can only be described as a bargain valuation: roughly one-times EV/EBITDA and three-times earnings based on FY 2024 figures, not peak-cycle numbers.

Several factors have undermined investor confidence, keeping the share price depressed since the PGM downturn. Management is directing virtually all operating cash flow into the Karo mining project—an undertaking that is not viable at current prices and is assigned a negative present value by most analysts. I take a different view. Although material risks exist—especially regarding management’s alignment with shareholder interests—a sustained rebound in PGM prices could transform Karo into a high-value asset and spark a rapid rerating of the shares.

With the stock up only 15 percent year-to-date, Tharisa still trails its peers. The Karo project effectively functions as a free option on stronger PGM prices, obtained alongside an existing low-cost mine. The position is certainly speculative, but it may appeal to investors who are bullish on the PGM sector. For further detail, please see my full write-up.

6. Execution Plan

I love the PGM market because of its extreme concentration. The paradox of abundance does not exist here. As Hugo showed, only a handful of names are available to trade.

Thus, to get exposure to the PGM theme, we have three alternatives, each with its pros and cons:

Equally weighted basket: the goal here is to squeeze as much as possible the PGM’s Beta.

Value investing approach: pick small-cap PGM miners with the ultimate goal to gain Alpha on top of the PGM’s Beta

LEAPS calls strategy: pick call options of the most liquid names, in that case Sibanye Stillwater, with the purpose of gaining Alpha on top of the PGM’s Beta

The third strategy is my favorite because it provides the upside of small-cap miners, but the downside risk of large-cap names. Yet, depending on market goals, risk tolerance, and skills, the other two alternatives might be better.

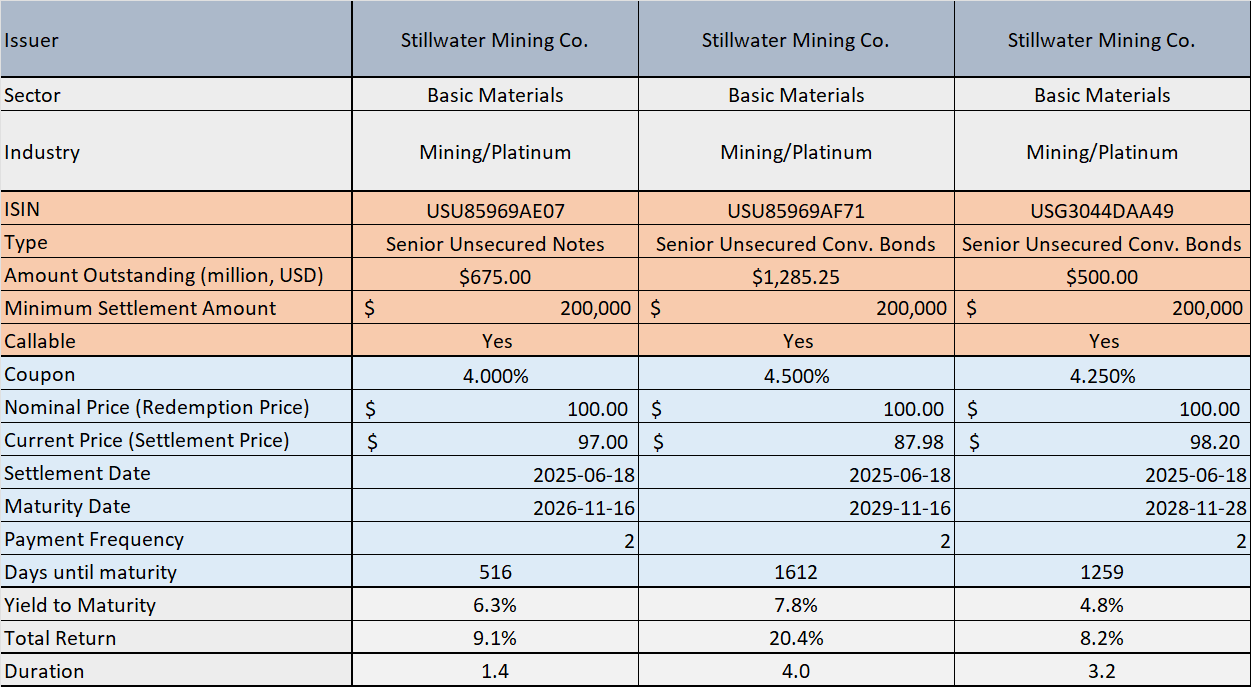

A side note: for income seekers, the PGM market offers limited opportunities. The only viable instruments are Stillwater Mining Co. bonds. The table below shows bond specs.

For curious investors, Sibanye bonds are not the only fixed-income instruments. Northam Platinum and Anglo American Platinum are also listed on the bond market.

Given the upside potential of PGM equities and mediocre (for the risk taken) PGM bond yields, fixed income is not the best place to be, except as part of a HY credit portfolio. That said, let’s move on to equity and option ideas.

As discussed, we are in the first inning of the game, when the volatility is still low. The following image (chart via Macro Ops ) illustrates perfectly the importance of position sizing during the cycle.

In short, in the first phase, we can bet bigger while keeping the risk size constant. During the trend emergence, going long LEAPS calls offers excellent risk-reward. At that stage, the volatility is low (even by PGM market standards), so we can buy cheap calls, as measured by implied volatility. Once the price surges, we profit not only from the price change but from the implied volatility increase, too. To recap, if we like to wager on the PGM bull run, we have options (pun intended).

Look at the chart below. It resembles the graph above.

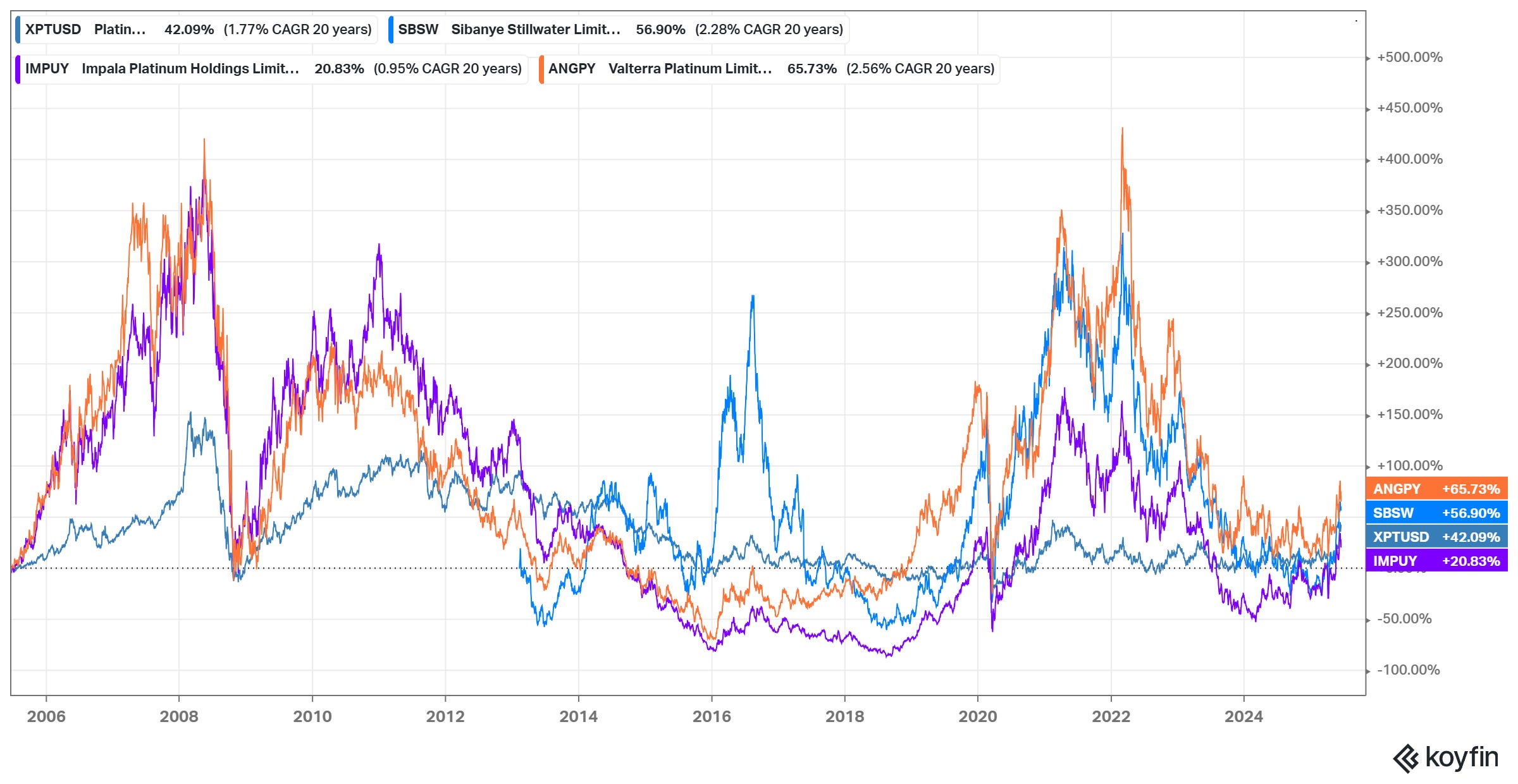

The odds of being right, or at least not wrong, are skewed in our favor. The Big Three, Sibanye Sillwater, Valterra Platinum (then Anglo-American Platinum), and Impala Platinum, are positioned for a missile launch.

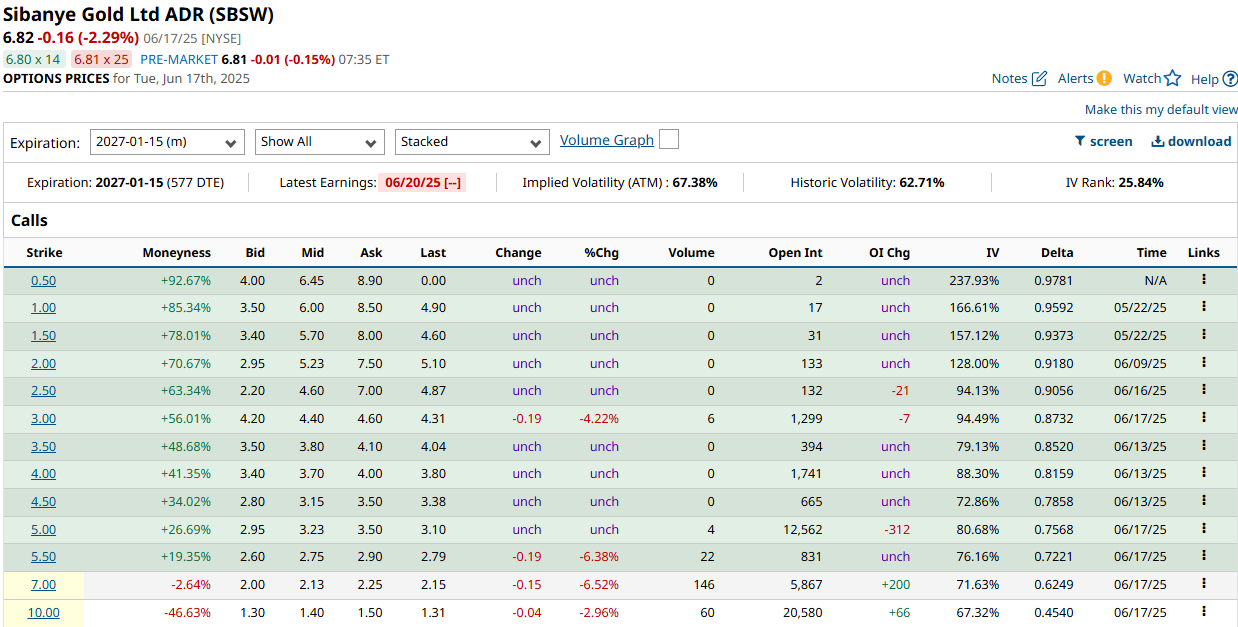

To ride the wave, we have equity and options at our disposal. If we prefer to play using LEAPS calls, Sibanye is the only practical alternative. It offers multiple tenors and strike prices. The table below shows SBSW calls with expiration in January 2027.

At first glance, implied volatility (IV) is too high. Usually, I shop for calls with an IV below 40%. But the context matters.

PGMs, such as REE and uranium stocks, are inherently volatile, and searching for contracts with IV < 50% is a daunting task. To offset the high price as measured by IV, I purchased DOTM calls. For SBSW, this means a strike price beyond $7.0. My base case for Sibanye is that its shares will reach $18 to $20 within the next 12 to 24 months, resulting in a risk-reward ratio greater than 5.

Of course, position sizing matters. Despite the odds being favorable and RR being > 5, we should never bet on the option more than a few hundred bps. Another thing to remember is to enter gradually. Let’s say we decided to allocate 200 bps to Sibanye calls. Do not shoot all at once, but split the position into three individual trades.

Last but not least, I will give an example of an equity position. The chart below shows the Impala Platinum (OTC: IMPUY) weekly chart.

The price has just pierced a multi-month range and is hovering above the 12-week moving average. A buy limit order with a stop just below $5.8/share. The first profit would be $13.0, at which point I would close at least half of the position.

This was just an example of how to bet on PGMs via equities. If the small caps are the preferred option, the role of price action takes the back seat. In that case, a fixed stop loss could cause more harm than good. This does not mean you should not use a stop loss. The idea is to shift from a price-dependent to a time- or event-dependent stop loss. Essentially, exit the position not based on a predetermined price, but on weakening conviction or on a time cap, even if the price is not moving down.

Positioning for each scenario

Here we present two main positioning strategies. Both are bullish on PGM prices: the first is more conservative, aiming for steadier, safer returns if the thesis takes time to play out; the second is more aggressive, offering potentially explosive gains should the current price move prove to be a true breakout.

Conservative scenario:

This is my preferred approach to PGMs. It focuses on low-cost producers with strong cash balances and combines them with spot exposure—through ETFs or physical metal—in palladium and platinum, so timing a rebound precisely is less critical. This mix should deliver better risk-adjusted returns than a fully aggressive allocation.

For investors with more than one million dollars to deploy, I recommend buying Valterra Platinum, which looks attractive after the completion of its demerger, and pairing it with palladium and platinum exposure via ETFs or physical holdings. A balanced 50/50 split between the stock and the metal makes sense here.

Investors with smaller amounts should look at the small caps—Sylvania Platinum (my favourite) and Tharisa—because they offer strong leverage to PGM prices over the next four to five years. The same 50/50 allocation rule applies.

Bullish scenario:

Investors who believe the breakout is already under way and want maximum upside should consider options and higher-cost miners, as these have greater operational leverage to rising PGM prices.

Large investors could combine equity and options in Sibanye Stillwater; Valterra Platinum is also compelling, as it still has room to catch up to peers once the short-term demerger overhang clears.

Smaller investors might focus on Sibanye Stillwater options and explore junior miners; my top pick in this space is Generation Mining.

You can blend these approaches to suit your style and assessment of where we are in the PGM cycle—starting aggressively, then shifting to a more conservative stance later to protect capital.

7. Conclusion

Hugo’s take

My focus is always on unloved and overlooked sectors and companies where the market is being unfair, and the PGM space has all the hallmarks of such mispricing. Supply is constrained, demand is steady—or even growing—and renewed investor interest is emerging while the sector remains largely unknown, leaving plenty of room for a rerating.

Although I am extremely bullish—and have been since platinum hovered near 900 dollars—I prefer a cautious approach. My PGM portfolio, therefore, holds three equally sized positions: a spot palladium ETF, a spot platinum ETF, and Sylvania Platinum. The last position has almost doubled since I purchased it for the Undervalued and Undercovered model portfolio. I am now considering reducing my platinum ETF exposure and adding a more aggressive position in higher-risk miners such as Sibanye Stillwater, or initiating a stake in Valterra Platinum, which still appears to have room to catch up with its major-miner peers after the demerger.

Overall, while I remain measured about the present price breakout, I believe PGM miners still offer significant upside at current levels. Metals such as palladium and rhodium should ultimately follow platinum once the market recognises that the fundamentals for all three are closely aligned.

Mihail’s take

I love hated markets. PGMs are the epitome of the loathed industry. When the Green Cult reached its peak and PGM mining CAPEX hit bottom, no one wanted to hear about platinum, palladium, etc. Recent price action indicates a shifting narrative. The market is moving from late pessimism to early skepticism.

To get exposure to the PGM industry, there are multiple ways. My favorite is using LEAPS calls on Sibanye Stillwater. In that way, I get junior miners upside potential coupled with a large miner's downside risk. That said, depending on investors’ goals, skill set, and risk tolerance, they can choose an alternative approach, such as investing in PGM juniors, an equally weighted book, or even high-yield bonds.

In summary, PGMs are one of the most asymmetric bets for the next 24-36 months. Of course, a gut-wrenching volatility on the way up is guaranteed. So, embrace a turbulent ride.

PS: For more actionable and asymmetric ideas on critical minerals and beyond, consider TheOldEconomy premium plans: Researcher and Strategist.

Thank you for being part of TheOldEconomy. Here’s to your continued growth and success, one wise decision at a time.

Invest wisely,

Mihail Stoyanov

Founder, TheOldEconomy

Everything described in this site, TheOldEconomy.substack.com, has been created for educational purposes only. It does not constitute advice, recommendation, or counsel for investing in securities.

The opinions expressed in such publications are those of the author and are subject to change without notice. You are advised to do your own research and discuss your investments with financial advisers to understand whether any investment suits your needs and goals.

| A guest post by

|

You might consider replacing that first image with an accurate periodic table.

Great article! I think pltm is the metal for a pragmatic time!