Week 25 26

Distressed Debt Basics and New Fortress Energy Bonds

Today's Sunday email is different. In addition to describing my plans for the week, I will discuss the basics of distressed debt investing, which will provide more context for the situation with New Fortress Energy.

First, let me share a few fundamental principles for investing in distressed debt.

Bankruptcy isn't an event; it's a process.

Every bankruptcy begins with a default, but not every default results in bankruptcy.

For the company's creditors, bankruptcy means debt restructuring or liquidation of the business. Accordingly, if there is a loss on the investment, it will most likely be partial.

For shareholders, however, the situation is different—in the vast majority of cases, when a company goes bankrupt, they realize a total loss on their investment.

Bonds 101

A bond is a loan agreement. As such, each bond comes with predefined parameters:

Face or par value of a bond: A common size is $1,000

Interest rate: In most cases, it is fixed in advance

Bond maturity: Normally, corporate bonds have a maturity of more than 5 years

Interest payment schedule: Usually, twice a year

Principal amortization schedule: The principal is repaid in full at the maturity of the bonds

Covenants: Additional loan terms that fall into three categories – restrictive, affirmative, and financial – that apply to the bond issuer.

Let me give you an example. We have a bond with the following parameters:

Nominal value: $100 (for easy calculation)

Interest: $10 per year

Maturity: after 12 months, on June 21, 2026

Interest payment schedule: payable at maturity of the bond, on June 21, 2026

Principal payment schedule: payable at maturity of the bond, on June 21, 2026

In summary, if we buy that bond today with a face value of $100 and interest of $10 (or 10% interest rate), after 12 months we will receive $110, i.e., $100 principal or $10 interest. The realized return for this period is 10%.

What would happen if we bought the same bond not at face value, but for $90, i.e., paying 90 cents for every dollar?

On the maturity date, June 21, 2026, we would again receive $110 ($100 principal plus $10 interest). However, since we bought it for $90 instead of $100, we will earn a total of $20: $10 in interest and another $10 in realized capital gains (the difference between the $100 face value and the $90 purchase price). Thus, over 12 months, we achieved a total return of 22%.

What is the reason for this?

Bonds are fixed-income securities, and the lower their price, the higher their yield. The bond issuer owes us that $10 in interest (and the principal at par), regardless of how much we paid for the bonds.

Now let's make the situation even more interesting – let's buy the same bond for 50 cents on the dollar, i.e., for $50. What would happen in this case?

On the maturity date, June 21, 2026, we will again receive $110 ($100 principal plus $10 interest). However, since we bought it for $50 instead of $100, we will earn $60: $10 is interest, and the other $50 is the realized capital gain (the difference between the $100 face value and the $50 purchase price). Thus, in 12 months, we earned a total return of 120%.

The last example illustrates the power of investing in distressed debt. However, it is wrong to focus solely on potential gains. Every investment should start with two questions:

What could go wrong?

If it goes wrong, how much will I lose?

As I said in the introduction, bonds are loan agreements. As such, they have a predefined life span. When we have a time frame, we can calculate the probabilities of a given event occurring (or not occurring) with a high degree of credibility. Thus, we can answer both questions.

Now, let's explore the topic in detail.

What can go wrong with my bonds?

For bonds, this is referred to as the default rate. This parameter does NOT measure the probability of the company going bankrupt or the probability of a total loss of the investment.

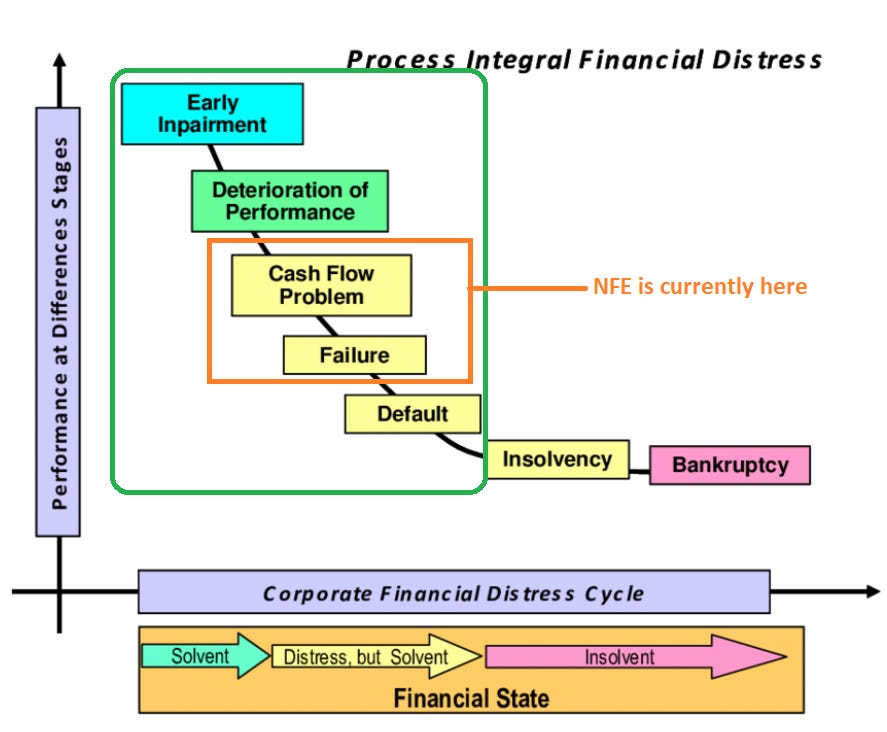

Here is a graphical representation of the financial distress process.

Let's see what the probabilities of default look like according to:

The industry in which the issuer operates

The issuer's credit rating