Market Overview Week 24

Market Overview Week 24

Oil, tankers, rigs, and banks

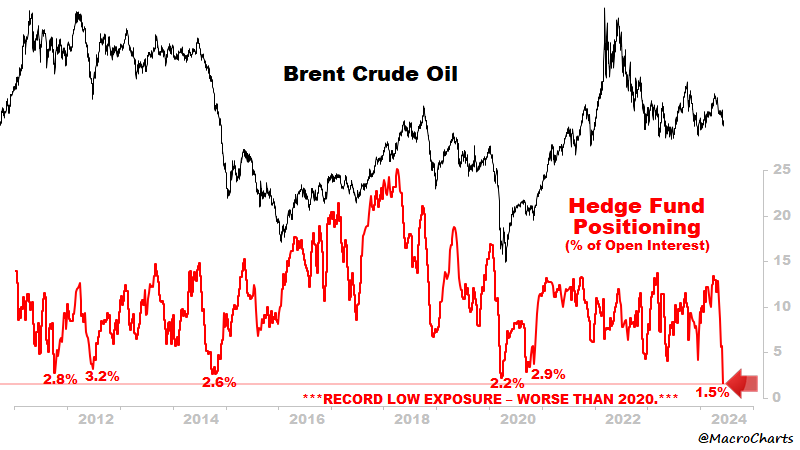

Oil has been moving in a relatively narrow range in recent months. The question is where it will continue.

The positioning of the big players is too bearish.

The lack of interest from hedge funds is record low. It even surpasses the March/April 2020 bottom.

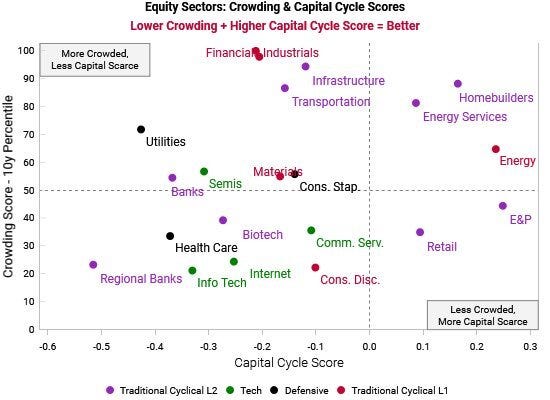

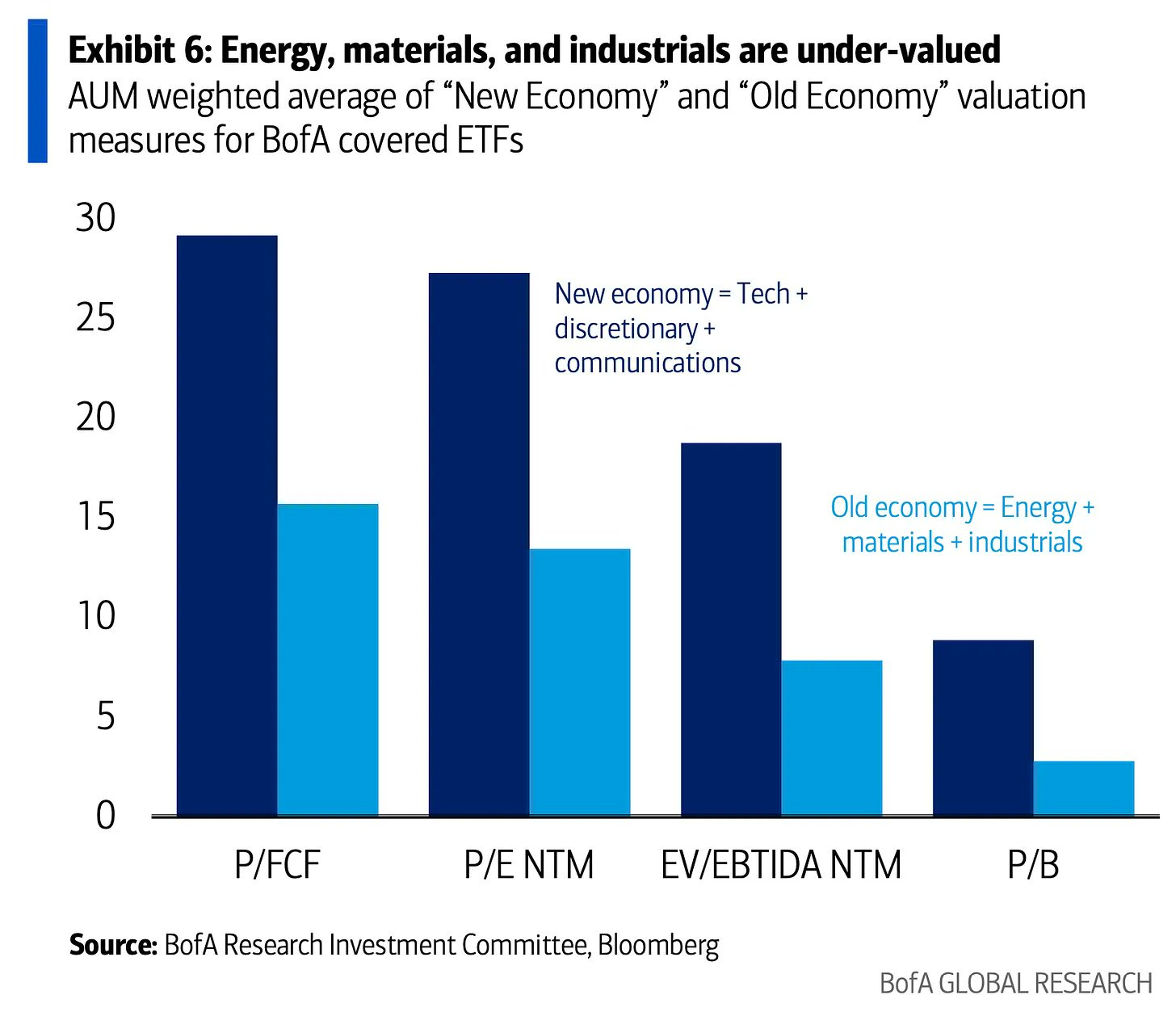

Overall, energy continues to be among the themes attracting less capital and market participants.

The result is low valuations. Old economy companies are trading at a significant discount compared to Tech, discretionary, and comms.

That doesn't mean shorting tech stocks. It is a reminder that there are many ways to generate Alpha.

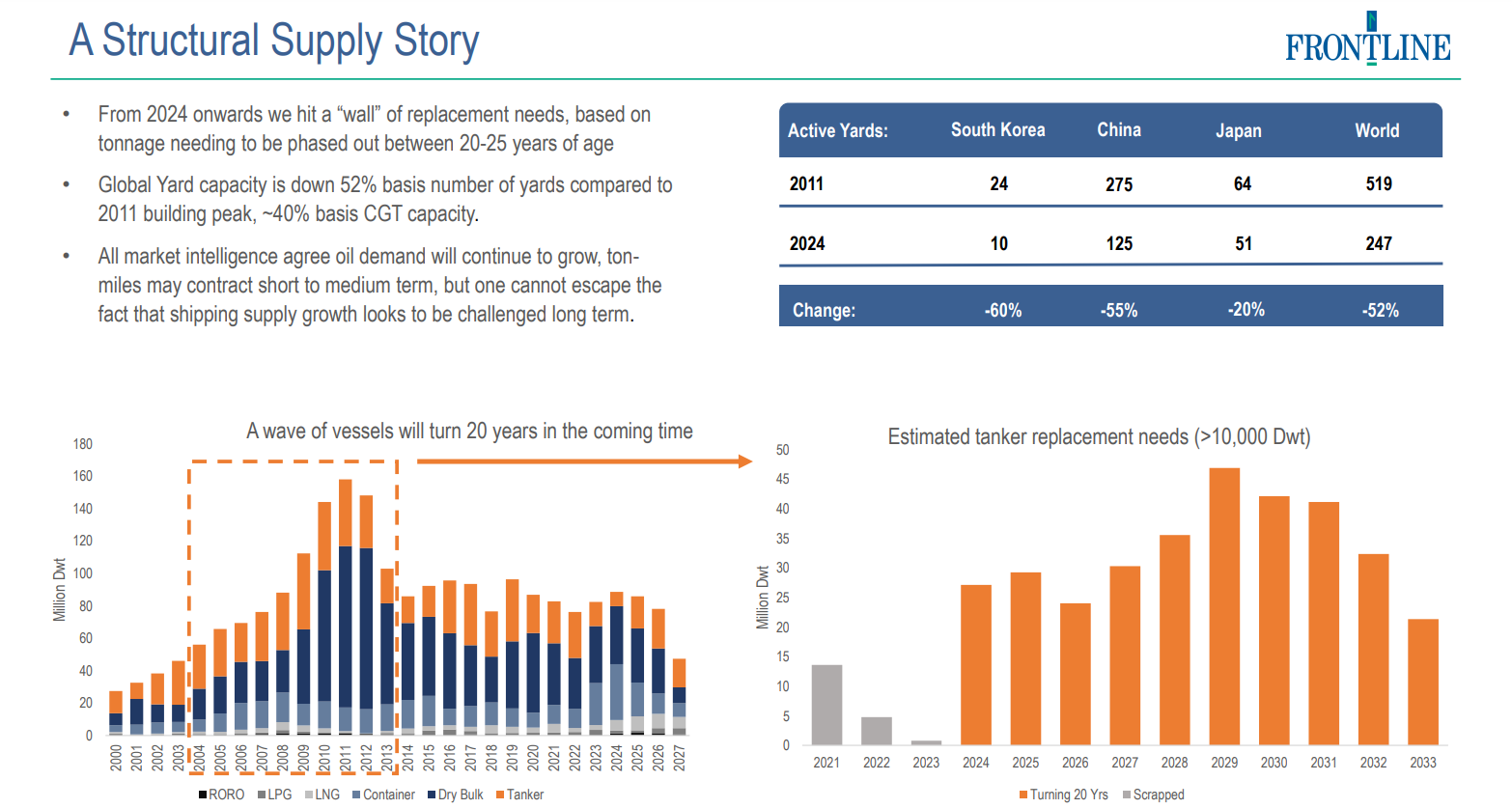

Two of the most promising industries in the old economy are tankers and oil rigs. They are extremely cyclical, which makes them relatively predictable.

The trick is where to look. With all asset-heavy companies, the supply-side rules. It shifts slowly due to the time it takes to build a ship, a mine, or a platform, while demand is more erratic.

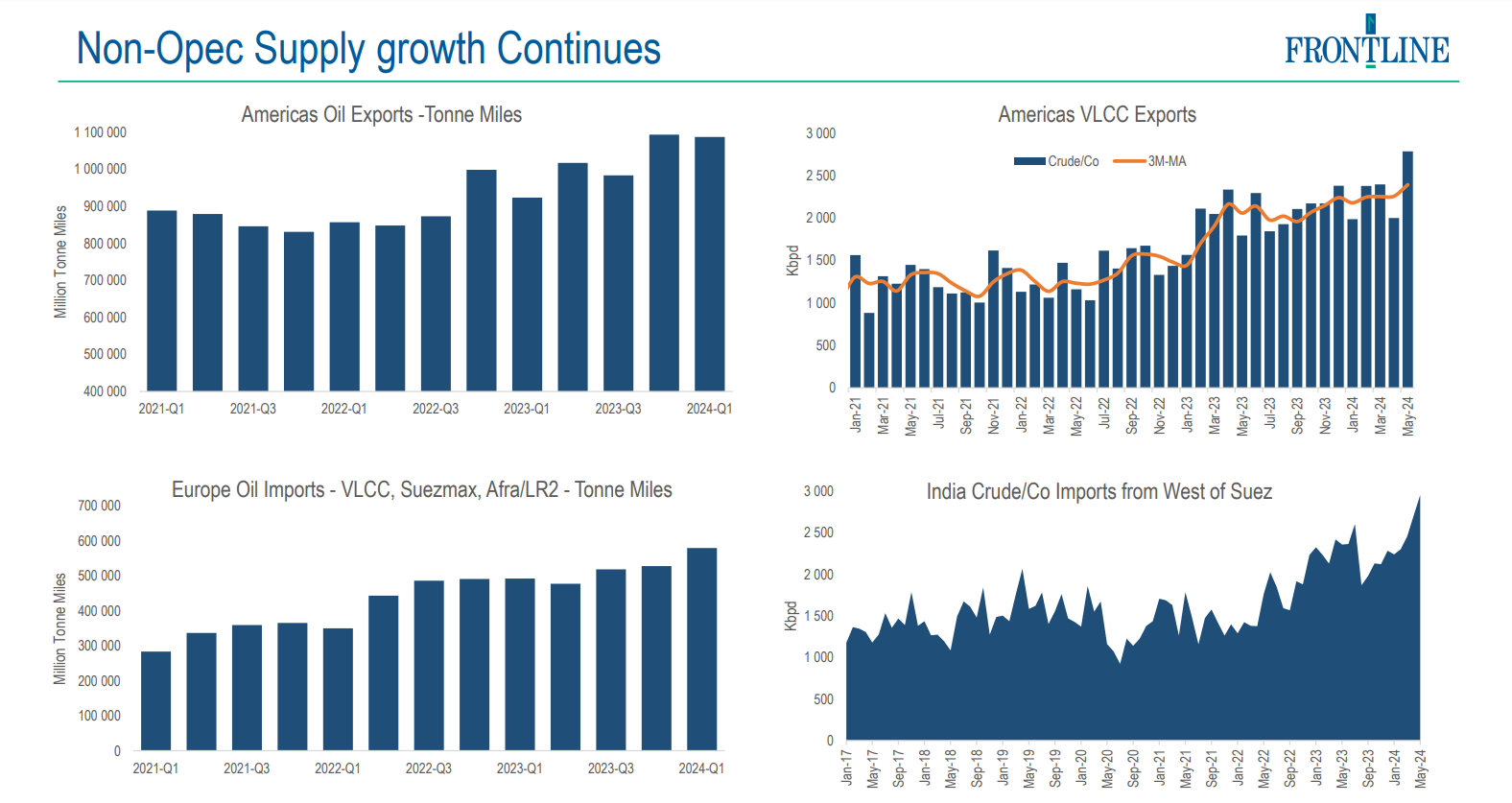

Not all tankers are equal. VLCCs bring the best fundamentals: low order book, aging fleet, and growing tonne-mile demand.

The global oil demand is robust, resulting in a growing need for VLCCs.

US crude oil exports are also increasing. The Middle East crisis remains a decisive factor in the VLCC demand equation.

Tanker transit through Suez is down 50%. The longer the resolution is delayed, the more the tanker demand will grow. At least for now, I do not see successful peace talks between Israel and Gaza. So, the supply chain constraints will persist.

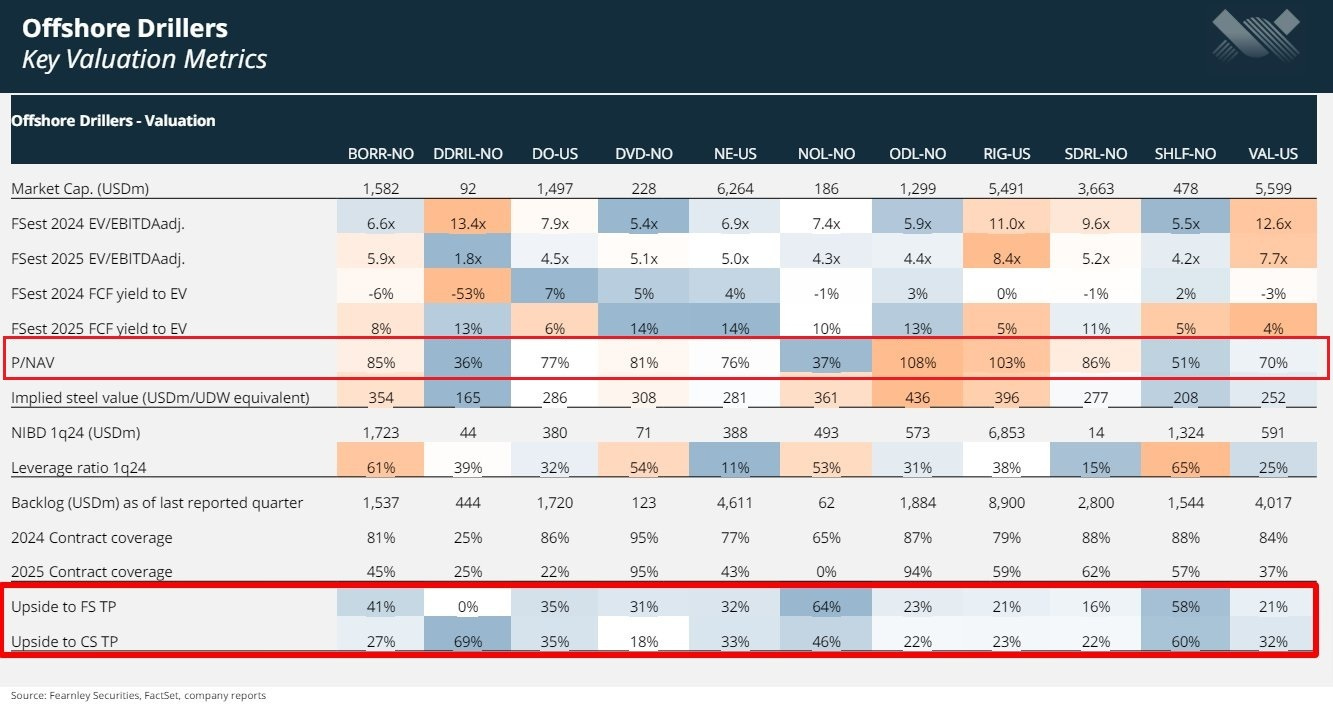

Oil rigs are another excellent way to bet on fossil fuel demand. Tankers sit between the oil well and the end user while oil rigs begin the oil extraction and processing process.

Currently, most companies in the industry are trading below their NAV.

Metals made delivered returns in April and May. However, in recent weeks, they entered into a deep correction. I expect the present commodities super-cycle to be highly volatile (even by commodity standards). And this is not a bug. Volatility makes investing in commodities great (if you know how to harness it).

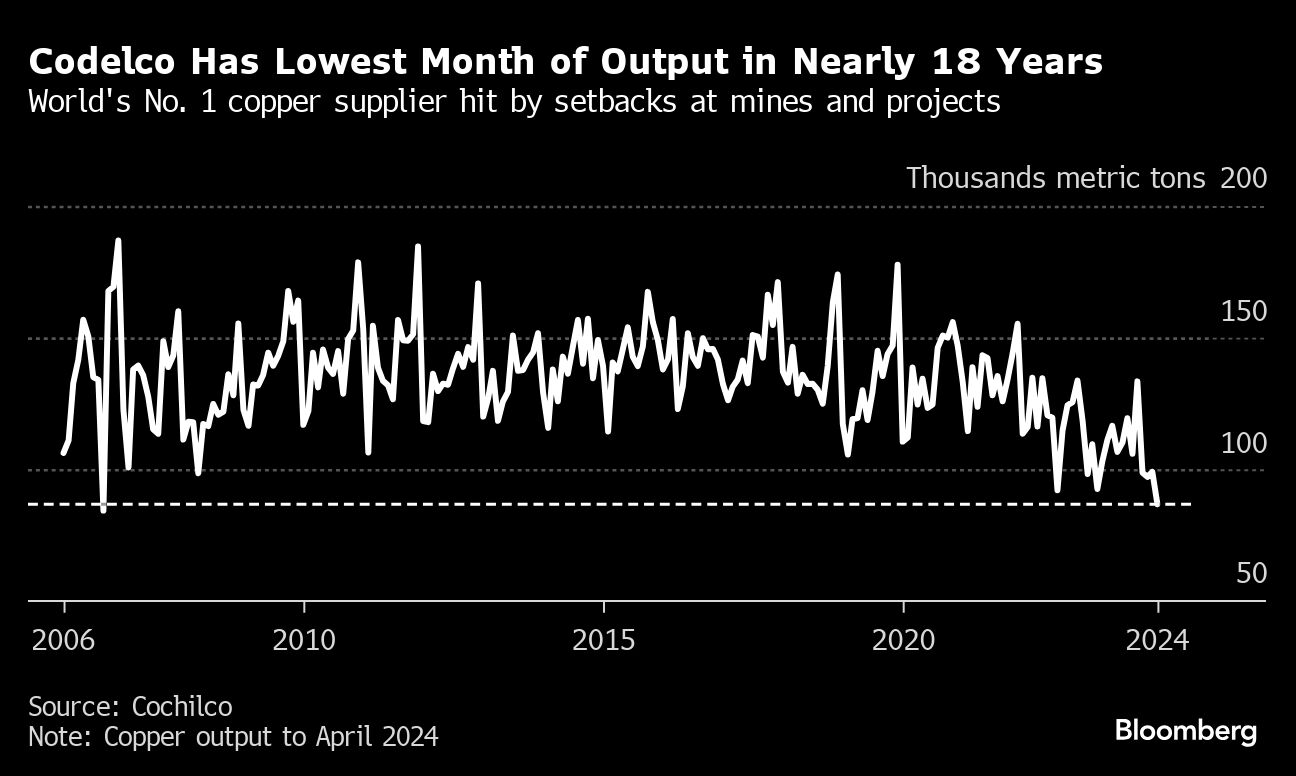

Copper shortages are here to stay. Codelco, one of the largest copper producers, is reaching record-low production figures.

Meanwhile, the need for copper seems insatiable. Green energy, artificial intelligence, and infrastructure renewal will drive the demand for copper in the foreseeable future.

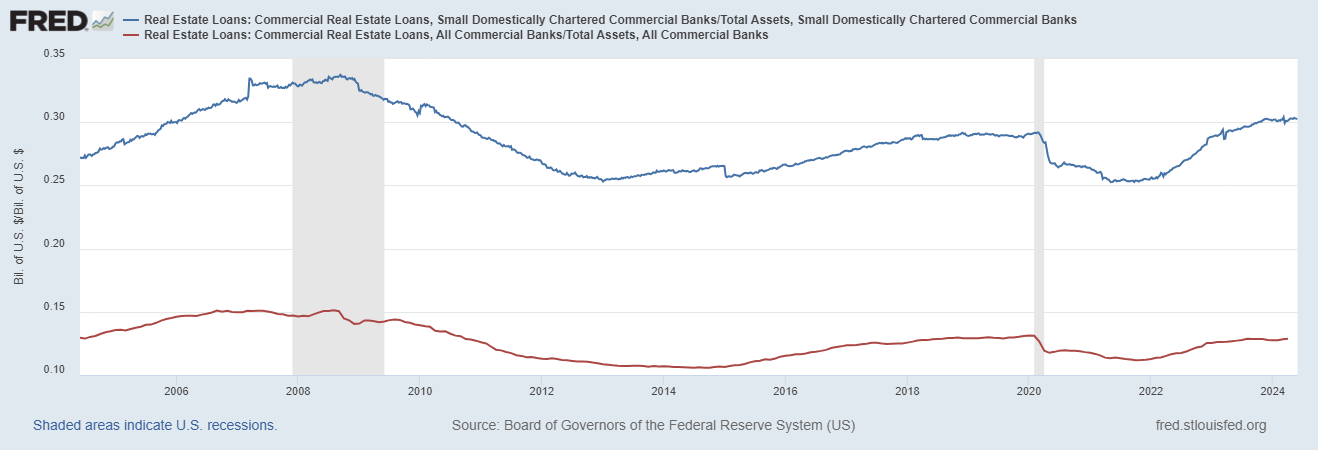

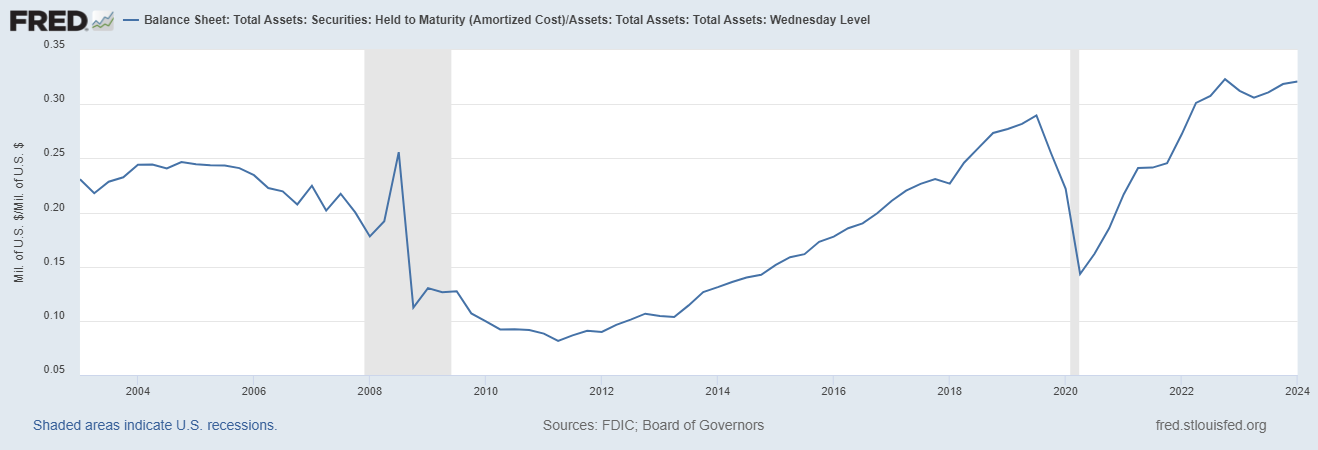

Let's see how the regional banks perform, particularly in two critical parameters: Treasuries held to maturity (HTM) and Commercial Real Estate Loans (CRE).

Both parameters are susceptible to interest rates. For HTM, the higher the interest rates, the lower the market price of the bonds, which means a lower value of the bank's assets.

CRE and high interest rates don't go well together, either. The loan is an asset to the bank and, as such, carries credit risk. The latter depends on the loan parameters and the reliability of the borrowers. A change in the former (particularly interest rates) can transform the latter's status from reliable to unreliable. Thus, the bank's credit risk rises sharply.

Let's see where the US regional banks currently stand.

HTM is way higher than in 2008 and 2019 as a percentage of total assets. Currently, they are about 32% of the banking system's total assets. It's a delicate situation. If interest rates suddenly rise in the next 24 months, there is a risk of another banking crisis.

In contrast to HTM, the CRE rate is lower than in 2008. A premature lowering of interest rates followed by a sharp rise would also negatively affect banks’ CRE exposure. At a certain point, some businesses cannot cover their obligations.

Thus, banks may end up with the collateral, i.e., the CRE. Tangible assets are not the bank's favorite. Unlike financial assets such as loans, they require maintenance, have low liquidity, and generate erratic cash flows.

The last two CPI reports show inflation deceleration. Two lower CPI prints do not cancel structural inflation. If the Fed were to cut rates decisively in 2024, it would feed the fire with fuel. In such a scenario, an emergency hike may repeat, as we saw in 2021/2022. Regional banks with higher CRE/HTM exposure carry the highest risk.

This is not to say that banks are a bad investment. Like any industry, nuances are important. Not all banks are equally attractive from an investor perspective.

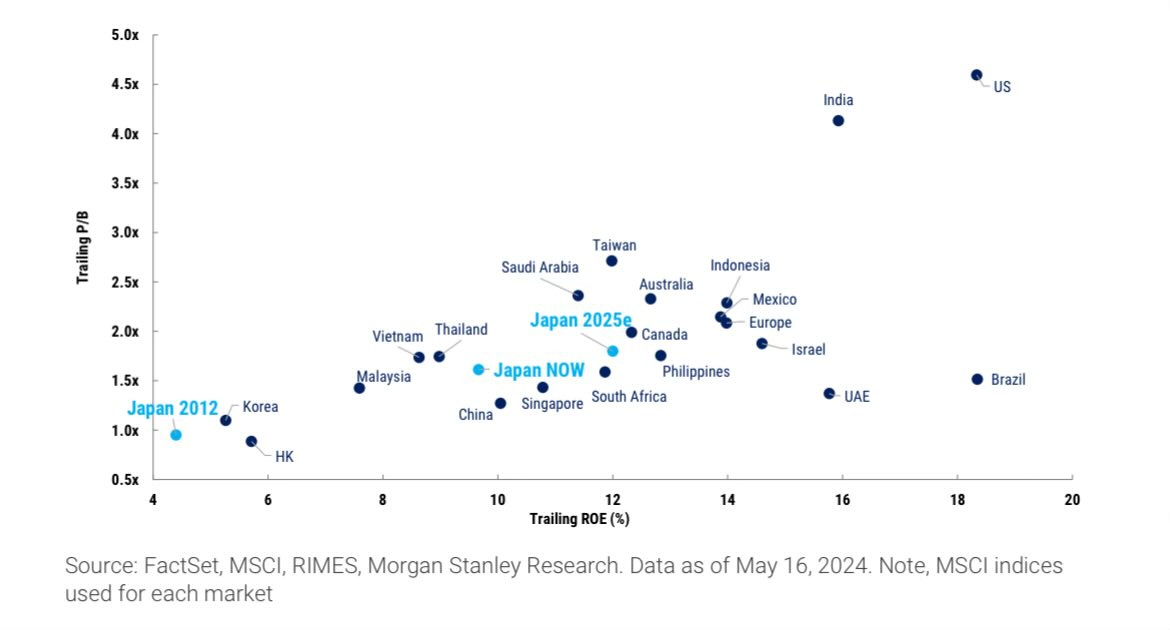

The following chart compares banks in developed countries and some major emerging markets by PB and ROE.

The further to the right and further down the country is, the more attractive its banks are. Brazil is an example. We pay 1.5 PB to get an 18% ROE. I would say it is an enticing offer.

Great one Mihail! I sent you a DM.