What do Switzerland, Norway, and Brazil share in common?

Investing in banking for adventurous investors

In my last article, I argue why I like the banking industry. Moreover, I share my framework for measuring risk and how I value a bank. The next step is to choose out hunting fields, i.e., where to find asymmetric stock picks in the banking industry.

In 2022 and 2023, I bet on Argentina, particularly Argentinean banks. To familiarize yourself with my analytical approach, read my takes on Grupo Galicia and Banco BBVA Argentina. The bet has paid off handsomely since Argentina’s political paradigm shift. Other enticing banking stocks are some Brazilian plays, like NU Bank, the largest neo-bank in the world. Besides Brazil, the two countries that grabbed my attention in 2024 are Colombia and Chile. Both trade at extremely cheap multiples.

Dark green and green countries offer the best risk-reward. Its PE ratio deviates at least one sigma from the 20-year average PE. Besides LATAM, my favorite region as an investor and explorer, enticing banking stocks can be found around the globe.

To find asymmetric stock ideas, I use a top-down approach. I start with the big picture (macroeconomics and geopolitics), work through regions and industries, and eventually reach individual companies.

In the context of banks, looking at areas with growth potential, I use the following criteria:

• Demography - population size and age structure. The more pyramidal the population pyramid, the better. Another hint is that a significant part of the population has passed the crucial threshold on the GDP S-curve. In other words, we have an emerging middle class. A great example was China 20 years ago. Nowadays, such countries are India, Nigeria, and Indonesia.

• The percentage of the population with access to banking services—the fewer, the better. A large percentage of the Global South population is underbanked, including Latin America, Central Asia, and the Far East (e.g., China, Japan, and South Korea).

• Regions and countries benefit from growing geopolitical entropy. Banks in the proper jurisdiction may serve as safe havens of capital. A prime example is Switzerland and its tradition in wealth management.

The criteria set seem contradictory at first glance. Nevertheless, banking is not a homogeneous industry; it includes a wide variety of banks. Accordingly, they prosper under distinct environments, depending on local demographics, economics, and geopolitical fragmentation. To put it another way, I would not look for wealth and asset management in Morocco or Islamic banking in Switzerland.

The list below presents the regions I consider attractive investments in the coming years. Each has its specificities, which are also reflected in the dominant banking sector. The exceptions are digital payment banks, which will become increasingly relevant in every region of the world.

Where and what banks do I look for:

• South America - traditional banks, digital payments

• Norway - commercial banks, digital payments

• Sub-Saharan Africa - Digital Payments and DeFi

• North Africa and the Middle East - Islamic banking and digital payments

• Switzerland - wealth and assets management, global advisory banks

In a few paragraphs, I elaborate on my thesis on a few prospective regions: Norway, Brazil, and Switzerland. The list is not exhaustive. I plan to write a separate article on Latin American banking stocks.

Norway

Norway is a positive example of an economy based mainly on extracting raw materials. Unlike many countries from the Global South suffering from the proverbial resource curse, Norway’s government has been a prudent capital allocator, playing the long game. Venezuela is a notorious example, with the largest oil reserves and a GDP as large as West Germany's in the 1970s.

Norway has several advantages that Venezuela lacks, such as a small and educated population. At the same time, it does not suffer from the migrant problems that are typical of Sweden. I am not saying Norway does not suffer from political issues. The leftist plague is spread in Scandinavian countries, rotting the fabric of society. Norway, however, seems less affected compared to Sweden and Finland.

In summary, Norway's advantages are as follows:

A small and well-educated population

Strong oil industry

Strong fishing industry

The most prominent sovereign wealth fund in the world

Norway, however, skillfully manages its oil and fishing revenues through its sovereign wealth fund. On average, Norwegians have $250,000 in fund assets.

The highly educated and affluent population will increasingly need efficient banking services, so the demand for digital banking services will grow. At the same time, traditional banks will have to adapt successfully to their customers' needs. Those who integrate innovations into their business processes will be the big winners.

The graphs below show a few Nordic banks with attractive valuations.

Brazil

Brazil is the tenth economy in the world and the first in South America.

Its strength and potential rests on the following:

A large population, of which 69% is of working age, i.e., 150 million of the total population;

Brazil, the world's fourth-largest country in terms of arable farmland, is in the top five in soybean production and first in coffee, orange juice and sugar production;

They have some of the largest reserves of Pre-salt gas and crude oil.

The election of Lula da Silva has stabilized Brazil politically - after the relative isolation of the Bolsonaro administration, the country is gradually returning to the big geopolitical game;

Brazil ranks among the top five in the world for bauxite and iron ore and among the top ten for gold and natural gas.

Brazil, unlike Norway and Switzerland, is a developing economy. However, this has its advantages, which lie in demography.

The potential of Brazilian banks is a function of Brazil's demographics and economic growth. GDP is set to grow at 2% per year over the next few years. The population in the 18-65 year old range is 150 million, or 69% of the country's population. This means that opportunities are yet to come.

Overall, Brazil's banking sector is very healthy and highly undervalued.

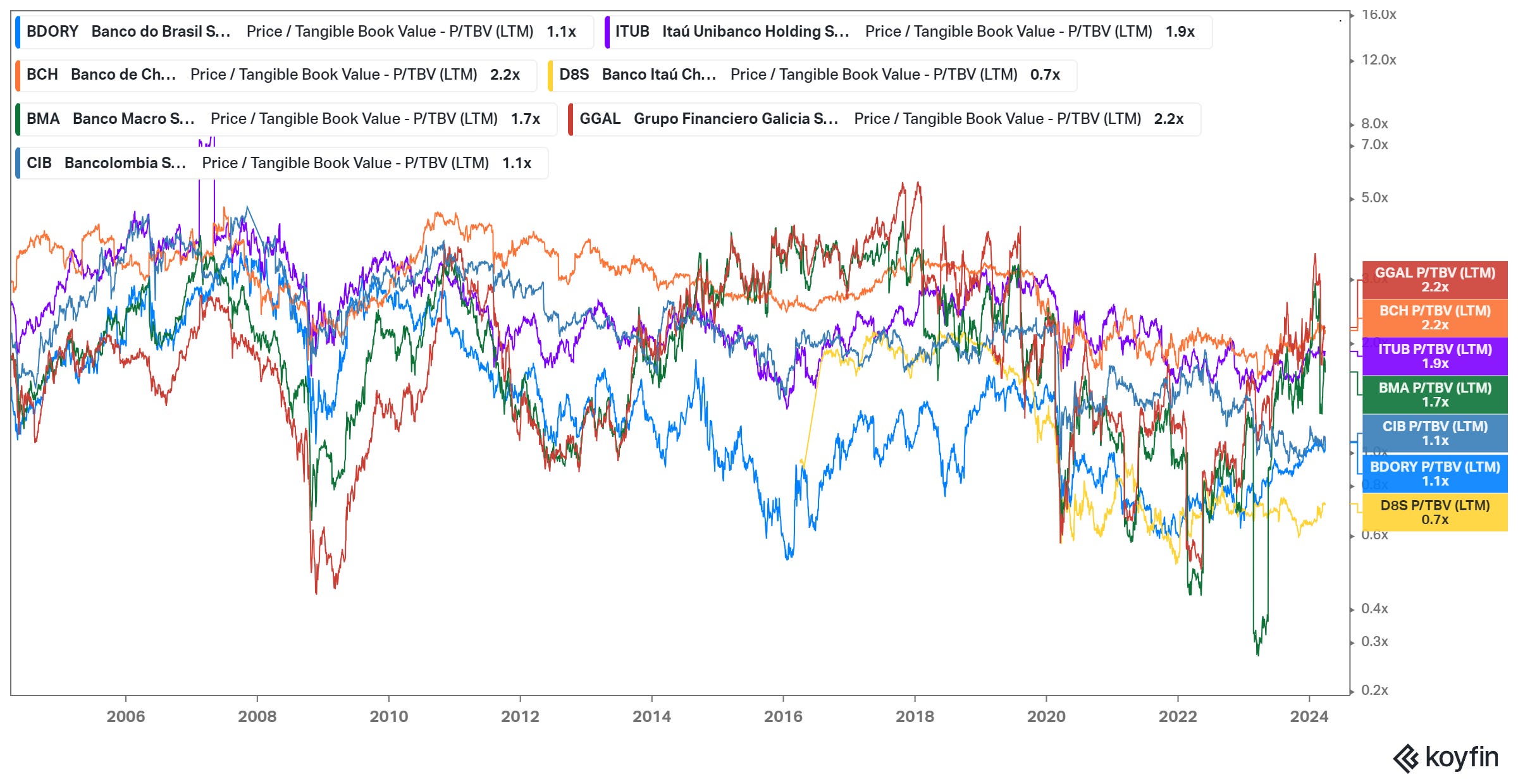

The chart above compares major Brazilian banks with Bank of America and JP Morgan. I use Price-to-Tangible Book Value to estimate the relative standing of the Brazilian banking industry. The American GSIBs trade at higher multiples compared to their Brazilian counterparts.

On the continental level, Brazilian banks are cheaper than Chilean and Argentine banks. Only the Colombian banks trade at lower multiples than the Brazilian banks.

Brazil is politically stable (by South American standards) and is going through a "normal" turbulent period globally. However, the market is pricing Brazilian equities as if Brazil were going through a deep internal or external crisis.

A growing population, not a tiny part of which is unbanked, and a strengthening economy will increase demand for banking services. In this case, the focus will be on traditional and digital payment banks.

Switzerland

The Swiss banking system is not limited to Credit Suisse. Asset and wealth management is the core of banking services in the land of purple cows and Patek Philippe.

Switzerland remains the number one destination for capital preservation. Here are some of the reasons that make Switzerland so attractive:

• Switzerland has a banking tradition of over 400 years. The first wealth management bank was Lombard Odier, established in 1796 and still exists. As its name suggests, it was founded by descendants of the Lombardi family, who came from the birthplace of modern banking, the Lombardy region of northern Italy.

• Highly educated population with a civic consciousness—Switzerland's economy is based on producing high-value-added goods and services requiring highly skilled personnel, so the population is necessarily highly educated. Another advantage is that civic consciousness is closely linked to education and governance through referendums following direct democracy principles.

• Switzerland is an entirely mountainous country, which makes an external invasion (almost) impossible. There are no plains in Switzerland, only mountains, making planning a military operation challenging and expensive. Therefore, the chance of such an invasion is meager.

• Firearms ownership is legal, and the population regularly undergoes military training - highly educated people with a civilian consciousness and the right to own guns is a nightmare for any internal or external enemy wishing to seize power.

• Permanently subscribed to the top three in GDP per capita globally, Switzerland manages the money of the rich while belonging to their club.

An affluent, responsible, and educated population ensures, to a large extent, the absence of internal unrest or invasion from outside. This means peace, the perfect environment for the capital to realize its purpose and multiply.

The above points can be summed up in three words - tradition, security, and responsibility. Popular destinations like Malta or Cyprus cannot boast these qualities. All this makes Switzerland the perfect destination for investment in private wealth and asset management banks.

Swiss banks trade at higher multiples than US and EM banks. The following chart shows two primary players in wealth management in Switzerland, Vontobel and Julius Bar, plus other major Swiss banks.

The old economy will become increasingly attractive to investors. The prime reasons are secular inflation and geopolitical fragmentation. It's an exciting time for market participants keen to delve into obscure and overlooked regions. The banking industry around the globe offers excellent opportunities for adventurous investors.