Adventures in REE universe, Part 3

Explorers and Developers

Critical minerals have made a comeback in the news. On Monday, China announced export restrictions on gallium, germanium, and antimony to the US.

CCP already took measures to curb antinomy exports in September. Antimony trioxide prices have reflected the measures. Rotterdam's price has increased by 230% since September to $39,000/ton. China is responsible for nearly 50% of the global antimony supply. On the other hand, it accounts for about 60% of refined germanium output and 98.8% of refined gallium production.

Export restrictions are part of one of the most asymmetrical themes for the next few years: trade wars between Great Powers. They include tariffs, export/import bans, and sanctions on various entities.

Here, I lay out my framework for playing the game. Below is a quote that summarizes it all:

Trade wars represent event-driven investing at a macro scale. Punitive measures have the potential to spark a sudden deficit in an already capital-starving industry. Critical minerals mining matches perfectly the description.

China is not the only country in that game. Russia has a lot to offer. Think about uranium, nickel, and palladium, just to name a few. Russian President Putin proposed restrictions on uranium exports a few weeks ago. Let’s not forget that sanctions work both ways.

Among the listed measures, my favorite is the critical minerals game. Russia has already taken decisive steps to curb uranium exports to the US. Kazatomprom kindly followed, diverting an ever-increasing part of its production to China.

PGMs have also been on my bingo card for export/import restrictions. Over the last 12 months, it has been discussed that the trade of Russian palladium could be restricted on the London Metals Exchange. Conversely, Russia can stop palladium exports to non-friendly states at any time.

Last but not least, rare earth elements (REE) serve as another geopolitical lever in China’s possessions. The probability of NOT applying REE export restrictions is lower than the opposite, which is restricting exports. In other words, I anticipate that REE will retake center stage in the next few quarters of the trade wars.

The best thing is that all discussed minerals fall in the “Simple” category. A few major players dominate supply and demand. The fewer participants there are, the better, especially for supply. Thus, creating credible scenarios is less challenging and less prone to mistakes.

I have extensively covered uranium and PGMs (links at the end of the article). I dedicated two articles to REE, and today, it's time for a third one. The first chapter discussed the REE market dynamics, while the second discussed the only existing producers outside China, MP Materials and Lynas Rare Earths.

In today’s write-up, I dive into the esoteric side of REE mining, the junior miners. Unlike gold, the REE universe is tiny, so the number of explorers and developers is limited to less than ten companies. To emphasize here, I mean REE pure plays.

Many aspiring mining companies list REE among their reserves. However, rare earths are a by-product of copper/gold/uranium/nickel mining. If I want to get exposure to REE, I prefer pure-play ideas, not polymetallic miners.

REE geography

To figure out where to look for fresh ideas, we must know the REE reserves' distribution. Everyone knows that China is the leading producer of rare earths. The same is true for the total reserve base. Interestingly, the second contender is located in LatAm.

Brazil holds 19% of global REE reserves, the only country with significant reserves in the Western Hemisphere. The US and Australia have negligible reserves compared to the top three players.

Going further to the Monroe Doctrine, LatAm falls in the US sphere of influence. The continent's role as a secure and reliable source of critical minerals for the US will grow proportionally to geopolitical entropy. South America offers the lowest geopolitical risk of all continents, so Brazil, Argentina, and Chile will have an increasingly important role in US supply chains.

The next step is to look at the most significant underdeveloped REE projects:

The first thing to notice is Greenland and Canada have a few projects on the list. Greenland holds massive REE reserves. However, mining there is far from easy. In 2021, Greenland banned uranium mining and halted several REE projects.

Canada, on the other hand, is among the countries with the longest time required to build a mine:

Of course, this varies widely between the provinces. In that case, Brazil is more competitive than the US and Canada.

In summary, Brazilian REE reserves will attract considerable attention in the coming years. This does not mean that other mining jurisdictions like Australia will lose their importance. Australia is the second REE-producing country outside China. That said, today’s contenders are Australian, Brazilian, and Angolan.

Choose your player

2024 was challenging for REE miners. The chart below shows the YTD performance of the most liquid names.

The developers (expect Arafura) delivered double-digit YTD gains, while producers struggled to stay even.

Our contenders are:

Pensana PLC

Arafura Rare Earths Limited

Brazilian Rare Earths Limited

Pensana PLC

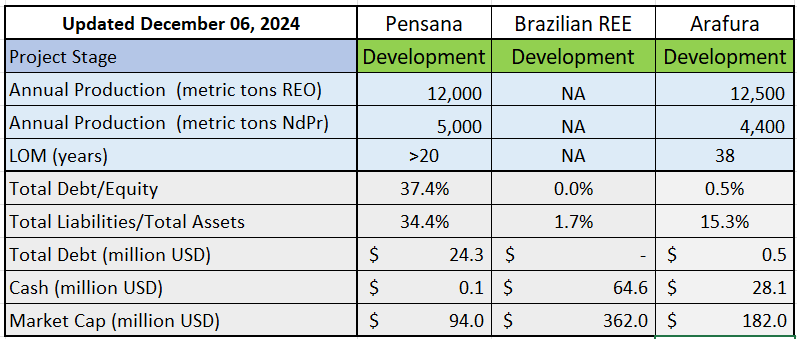

Pensana PLC is developing the Longonjo REE project in Angola. According to Pensana estimates, it is expected to become one of the world's largest REE mines, producing 5% of the world's NdPr supply. Annual production is projected to be 12,500 tons of separated REE, including 5,000 tons of NdPr oxides.

The Longonjo project is located in the Longonjo municipality of Huambo Province, Angola. It is near the Lobito Rail Corridor and has access to national roads and railways.

Longonjo is an open pit mine. Main construction started in 2024. In May, the company received approval for a 35-year mining title. Initial production is scheduled for late 2025; final commissioning is expected in 2Q26.

Pensana owns 84% of the project, Angola Sovereign Wealth Fund holds 10%, and the remaining 6% is distributed between institutional and retail investors.

Arafura

Arafura Rare Earths' flagship project is the Nolans project in Australia's Northern Territory. It is one of the world's largest undeveloped neodymium and praseodymium (NdPr) resources. Nolans is expected to deliver 5% of the global NdPr production. Annual output is projected to be 12,500 tons of separated rare earths, including 5,000 tons of NdPr oxides. The mine has 38 years of LOM.

The Australian Government invested US$550 million in Nolans in March 2024. Arafura has signed an agreement with Hyundai Motors to supply NdPr. Production is set to start in 2028. With government support and macro tailwinds, Arafura may complete the project on time.

Brazilian Rare Earths

Brazilian Rare Earths Limited's primary asset is the Rocha da Rocha Project, located in the State of Bahia, Northeast Brazil. The company recently discovered the Pelé project, located 60 kilometers southwest of its flagship deposit, Monte Alto.

Below are some details about the recent discoveries:

1. Monte Alto East:

· High-grade rare earth channel sampling across a 3-m-wide exposure

· Grades up to 10.7% Total Rare Earth Oxide (TREO)

· Exceptional heavy rare earth grades:

· 4,306 ppm dysprosium oxide (Dy₂O₃)

· 508 ppm terbium oxide (Tb₄O₇)

· 51,556 ppm yttrium oxide (Y₂O₃)

2. New Discovery 2.5 km from Monte Alto deposit:

· Outcropping rare earths mineralization

· Grades up to 14.5% TREO

· High-grade heavy rare earths:

· 5,691 ppm dysprosium oxide (Dy₂O₃)

· 737 ppm terbium oxide (Tb₄O₇)

· 74,543 ppm yttrium oxide (Y₂O₃)

The dysprosium and terbium grades are reported to be some of the highest-grade assays ever reported globally.

Monte Alto is still in its early stages of development. A Stage I Scoping Study is scheduled for 2Q25. Completing the scoping studies in 2025 will likely clarify the potential production timeline.

As can be seen, the companies are at different development stages. Pensana is the most advanced, followed by Arafura. BRE is still in the early stages of defining its reserves base.

Now let’s put it all together:

All contenders have a solid capital structure. Pensana, however, has nearly zero cash reserves. The company plans to start production in 2025, which means a lack of liquidity may postpone mine commissioning. I anticipate share issuance to fund the commissioning.

BRE holds sufficient cash reserves to finance the scoping studies in 2025. Hence, share dilution is not on the agenda. Moreover, BRE has no debt. Similar is the situation with Arafura, which has adequate cash reserves and nearly zero debt.

Final Thoughts

In a long term demand for NdPr is poised to grow:

In the mid-to-short term, however, demand is not the prime driver. Considering the cooling down of the EV craze, NdPr consumption may even decline.

The driving force here is the trade war. The anticipation of limited future supply will push the companies to frontload as many REEs as possible. Let’s not forget that expectations drive the markets in the short term.

The NdPr price is a perfect illustration. The peak in 2022 was driven by fear of supply issues due to the Ukraine-Russia war.

In Part 1, I reminded the collision between Japanese and Chinese vessels that led China to ban REE exports to Japan. NdPr price went parabolic. There is a vast difference between the state of the world then and now.

Fourteen years later, global bifurcation is in full force. The trade war is one of the symptoms. REE export restrictions are among the powerful weapons at the CCP’s disposal. This factor makes REE a lucrative event-driven idea.

Explorers and developers offer extreme RR. Treat such companies as a call option on REE reserves in the ground and future cash flows from mining. Among the contenders, I would go for BRE.

It is in its early stages of development, has zero debt, and holds cash. Early stages mean that more catalysts are on the horizon to drive its share price higher. Zero debt and cash imply low downside risk (for junior miners).

A kind reminder: explorers and developers, more often than not, are cash-burning and promise-underdelivering enterprises. So, play the game accordingly.

For further reading:

Adventures in REE universe, Part 1

Adventures in REE universe, Part 2

Part 1: Uranium Market Overview

Everything described in this report has been created for educational purposes only. It does not constitute advice, recommendation, or counsel for investing in securities.

The opinions expressed in such publications are those of the author and are subject to change without notice. You are advised to do your own research and discuss your investments with financial advisers to understand whether any investment suits your needs and goals.